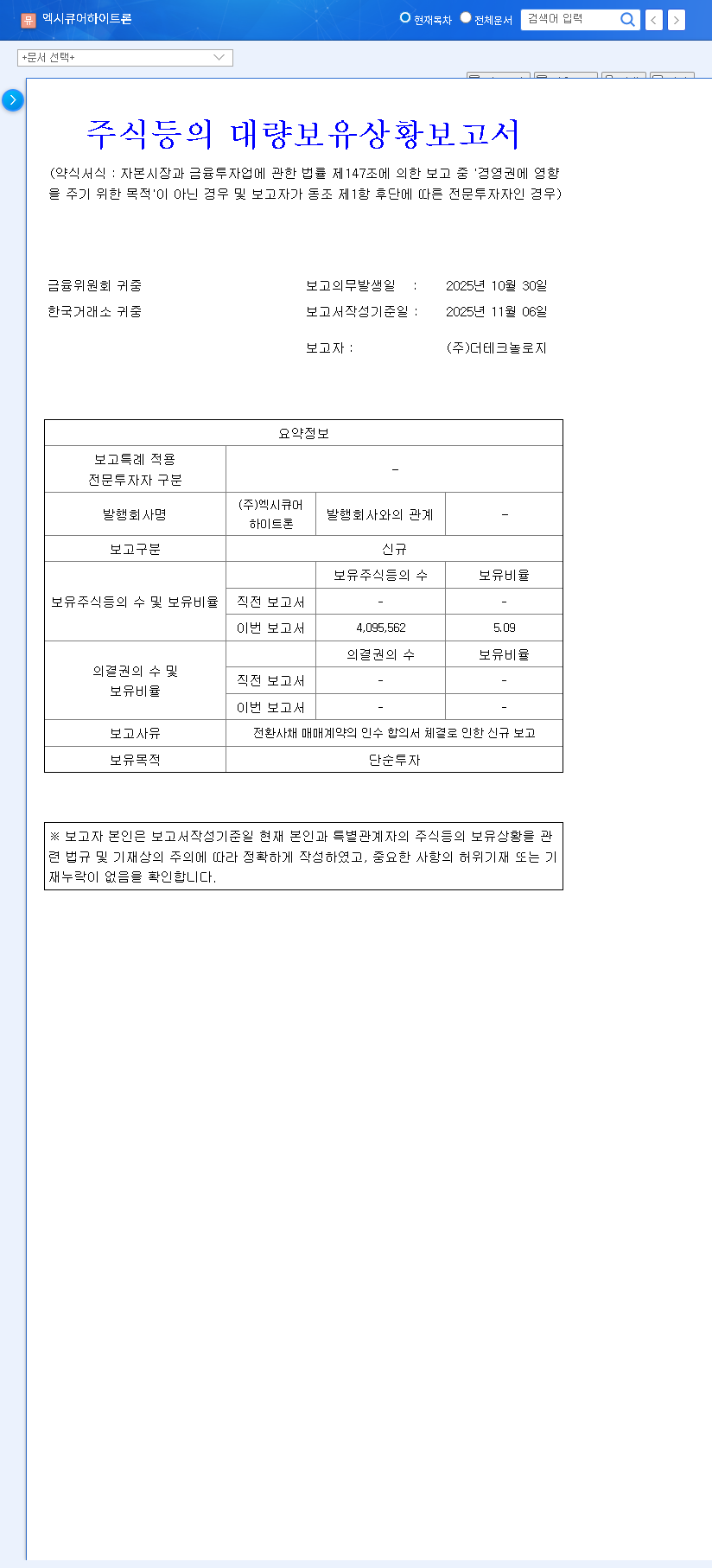

In the intricate dance of the stock market, the moves of major shareholders are often the most telling. For investors in HanWool Materials Science, Inc. (091440), a recent disclosure has raised critical questions. The company’s largest shareholder, Harrison Investment Union No.1, has reduced its stake, sending a ripple of uncertainty through the market. Is this a red flag signaling trouble ahead, or simply a strategic readjustment?

This comprehensive analysis will dissect the recent shareholding changes at HanWool Materials Science, evaluate its underlying financial health, and provide a strategic roadmap for investors navigating this pivotal moment. We will explore both the risks and potential opportunities presented by this development.

The Core Event: Deconstructing the Shareholder Stake Change

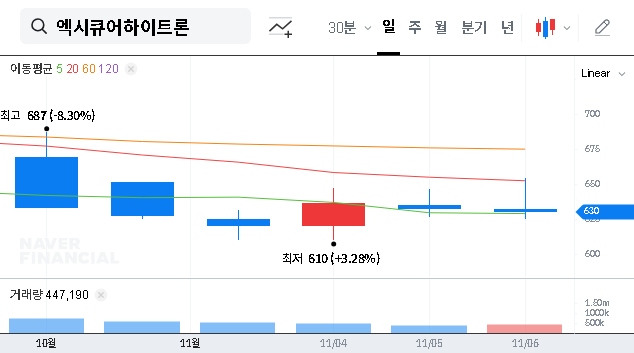

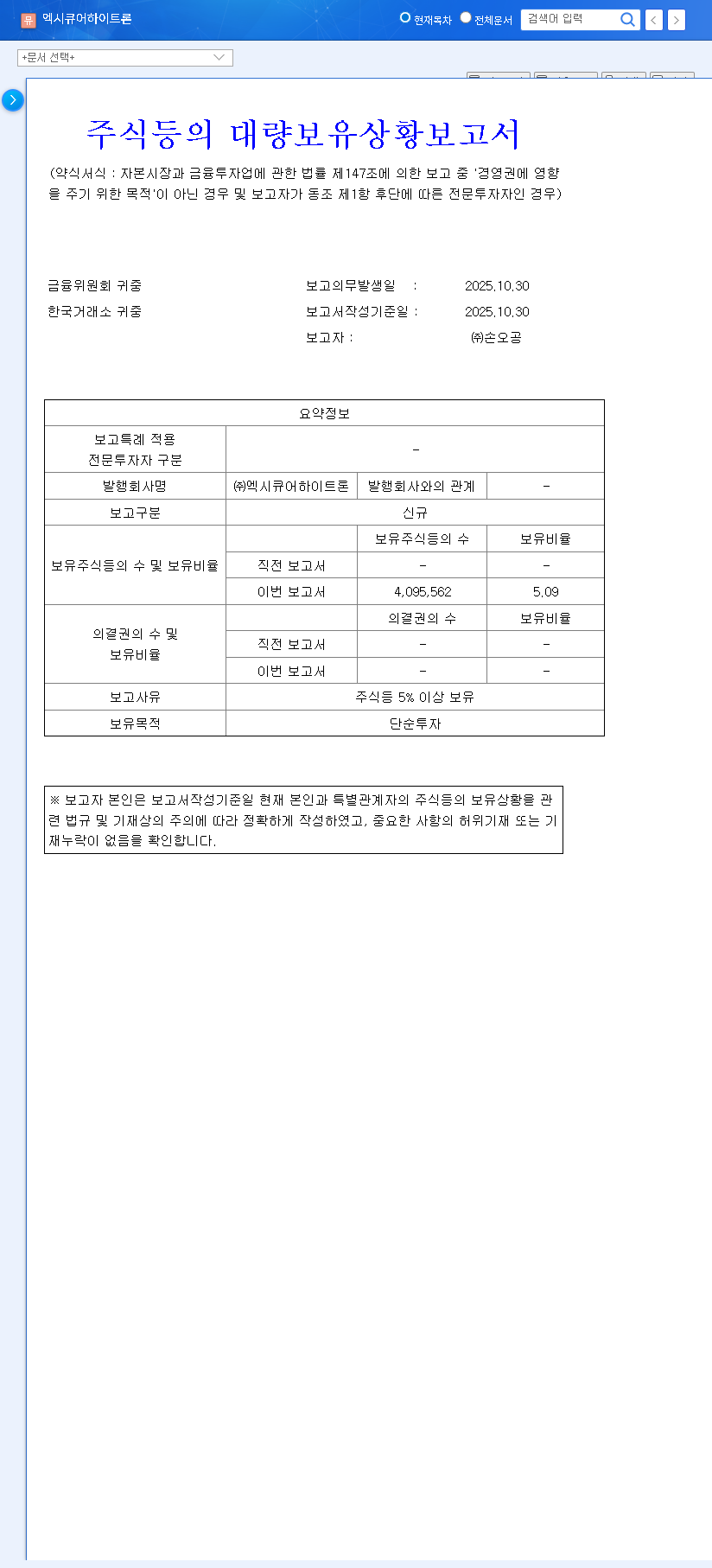

On November 10, 2025, Harrison Investment Union No.1, a pivotal shareholder in HanWool Materials Science, officially reported a change in its ownership. The stake decreased from 25.24% to 22.86%. While not a complete exit, this 2.38% reduction is significant. According to the Official Disclosure on DART, this was not a simple market sale but a complex transaction involving:

- •Partial Partner Withdrawal: Some members of the investment union decided to exit, leading to their shares being distributed.

- •In-kind Distribution: Instead of selling shares and distributing cash, the shares themselves were given to the withdrawing partners. This could lead to future selling pressure on the open market.

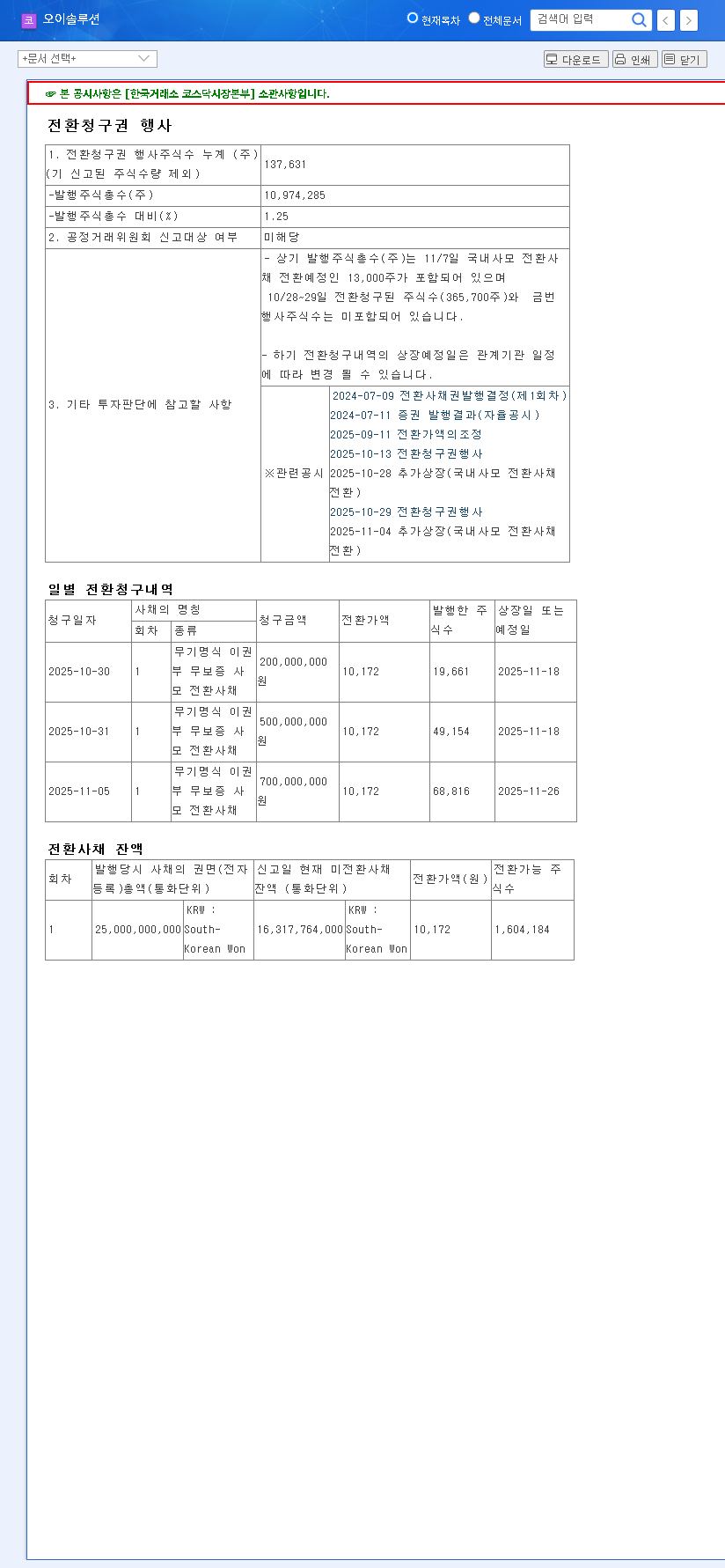

- •Exercise of Convertible Bonds: Concurrently, some convertible bonds (CBs) were exercised, converting debt into new company shares. This slightly offsets the reduction but also dilutes the value for existing shareholders.

A Two-Sided Coin: Analyzing HanWool Materials Science’s Fundamentals

To truly understand the implications of this stake change, we must look beyond the transaction and analyze the current health of the business. The latest semi-annual report for HanWool Materials Science stock paints a picture of a company at a crossroads, with promising ventures balanced by significant financial challenges.

The Bull Case: Potential Growth Catalysts

- •Strategic New Ventures: The company is expanding into high-growth sectors, including semiconductor materials (photoresist) and advanced GFRP rebar distribution, tapping into future-proof industries.

- •Technological Advancement: With the successful development of 5G/6G POTN equipment and participation in national R&D projects, HanWool is positioning itself at the forefront of telecommunications infrastructure.

- •Stable Revenue Streams: Key contracts with public institutions and major telecom operators provide a reliable, foundational revenue base.

The Bear Case: Significant Financial Headwinds

- •Persistent Losses: The company continues to post significant net losses on a consolidated basis, raising questions about its path to profitability.

- •Heavy Debt Burden: The issuance of KRW 42 billion in convertible bonds (CB) and KRW 37.5 billion in bonds with warrants (BW) creates a massive financial overhang. This poses a dual threat of stock dilution and future interest payments.

- •Sub-Investment Grade Credit: A BB- credit rating from NICE평가정보 signals concerns about financial soundness and could make future financing more expensive and difficult.

- •Negative Cash Flow: A significant deterioration in operating cash flow is a major red flag, indicating the core business is not generating enough cash to sustain its operations.

The key challenge for HanWool Materials Science is to translate its promising technological ventures into tangible profits before its financial burdens become insurmountable. This shareholder change adds another layer of complexity to that race against time.

A Strategic Action Plan for Investors

Given the mixed signals, a wait-and-see approach is insufficient. Proactive monitoring and a clear strategy are essential. For those invested in HanWool Materials Science, here is a recommended action plan:

- •Monitor Selling Pressure: Keep a close watch on trading volumes in the coming weeks. A spike in volume without a corresponding positive news catalyst could indicate that the partners who received shares via in-kind distribution are selling them on the market.

- •Scrutinize Quarterly Reports: The next earnings report is critical. Look for any improvement in operating cash flow and a reduction in net losses. Vague promises are not enough; concrete numbers are needed. For context, you can learn more by reading expert analyses on financial news sites like Bloomberg.

- •Track New Business Progress: Pay attention to press releases and industry news regarding the semiconductor materials and GFRP rebar businesses. Any news of new contracts or milestone achievements could serve as a powerful positive catalyst.

- •Understand Dilution Risk: Keep track of the outstanding convertible bonds and warrants. Understanding the potential for future dilution is key to valuing your investment. For a broader understanding of this topic, read our guide on how convertible debt impacts stock prices.

Frequently Asked Questions (FAQ)

Q1: What exactly happened with HanWool Materials Science’s major shareholder?

Harrison Investment Union No.1, the largest shareholder, reduced its stake from 25.24% to 22.86%. This was caused by some partners leaving the investment union, leading to a distribution of shares, and was partially offset by the conversion of some company debt into new shares.

Q2: Is a major shareholder reducing their stake always a bad sign?

Not necessarily, but it warrants caution. In this case, because the reduction is due to the structure of the investment union rather than an outright sale on the market, the immediate signal is mixed. The primary short-term risk is the potential for the exiting partners to sell their newly acquired shares.

Q3: What is the biggest risk for HanWool Materials Science right now?

The biggest risk is its financial health. The combination of ongoing losses, deteriorating cash flow, and a heavy debt load from convertible bonds creates significant pressure. The company must demonstrate a clear and rapid path to profitability to regain investor confidence.