The recent announcement of the Exion Group convertible bond issuance has sent ripples through the investment community. With a significant ₩10 billion deal on the table, stakeholders are closely watching what this strategic financial maneuver means for the company’s future. This represents a substantial capital injection, amounting to 14.66% of Exion Group’s market capitalization, and raises critical questions about its growth trajectory, financial health, and the potential impact on Exion Group stock.

This comprehensive analysis will break down the intricate details of the deal, explore the potential upsides and inherent risks, and provide a strategic outlook for current and prospective investors. Understanding the nuances of this Exion Group CB issuance is crucial for making informed decisions.

Unpacking the Terms: A Deep Dive into the ₩10 Billion Deal

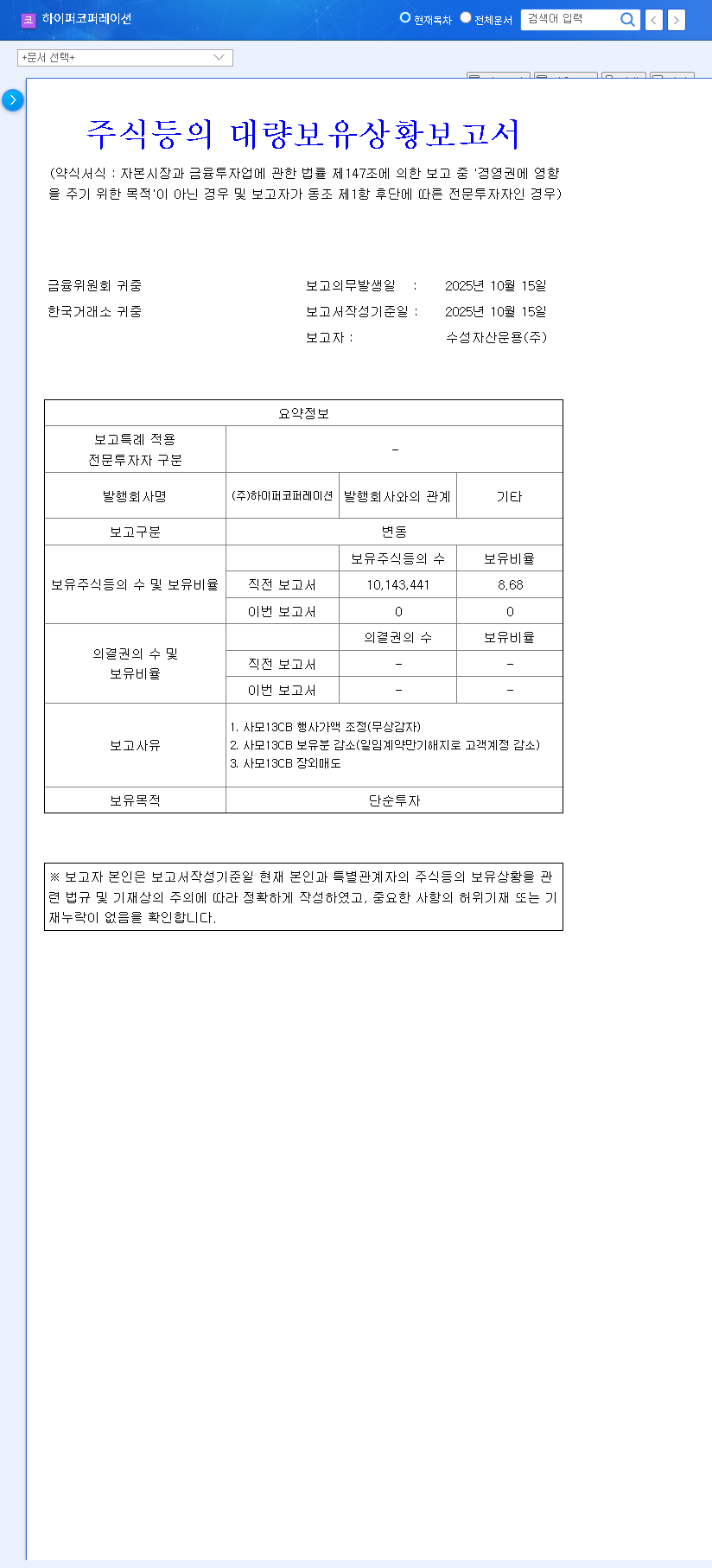

On October 22, 2025, Exion Group finalized its decision to issue the convertible bonds via a private placement, primarily to the ‘Cross No.1 Fund’. A convertible bond is a hybrid security that acts like a standard bond, paying interest, but can also be converted into a predetermined number of common stock shares. For a detailed primer, you can read more about how they work on authoritative financial sites. The official terms of this issuance provide a clear picture of the deal’s structure.

Key Financial Metrics Investors Must Watch

- •Issuance Amount: ₩10 billion

- •Conversion Price: ₩1,672 per share

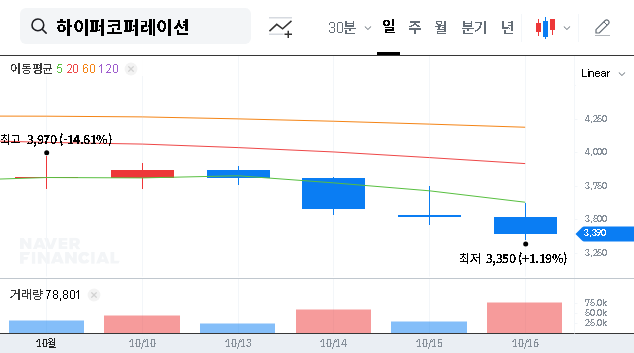

- •Current Share Price (at time of announcement): ₩1,369 per share

- •Minimum Adjustment Conversion Price: ₩1,170 per share

- •Coupon & Maturity Rates: 0.0% coupon rate with a 4.0% maturity yield.

- •Conversion Period: From November 13, 2026, to October 13, 2028.

The full details were published in a regulatory filing. Source: Official DART Disclosure

The Bull Case: Potential Upsides for Exion Group and Its Stock

From an optimistic perspective, this fundraising is a proactive step. The ₩10 billion capital injection can act as a powerful catalyst for growth, enabling the company to secure operational funds, invest in promising new business ventures, and bolster its R&D capabilities. This is precisely the kind of move that can drive long-term shareholder value if executed well, similar to what we noted in our analysis of Exion Group’s previous expansion efforts.

Furthermore, the fact that the conversion price (₩1,672) is set significantly higher than the current share price (₩1,369) can be interpreted as a vote of confidence. It suggests that both the company and the primary investor, Cross No.1 Fund, anticipate a substantial rise in the Exion Group stock price. If the stock surpasses this price, it creates a win-win scenario: the investor profits from conversion, and the company’s valuation is affirmed.

The Bear Case: Navigating the Risks of the Exion Group CB Issuance

However, investors must approach this development with caution. The most significant risk associated with any convertible bond analysis is the threat of share dilution. If and when these bonds are converted into stock, the total number of outstanding shares increases, which can dilute the ownership percentage and earnings per share for existing shareholders. This influx of new shares, especially if triggered by a stock price surge, could create overhead supply and put downward pressure on the stock price.

While the 0% coupon rate avoids immediate interest payments, the 4.0% maturity yield creates a future liability. If Exion Group’s business performance falters, this debt obligation could become a significant financial burden.

The ‘Minimum Adjustment Conversion Price’ of ₩1,170 is another critical detail. This clause protects the bondholder by allowing the conversion price to be lowered if the stock price falls, which would lead to even greater dilution for existing shareholders upon conversion. This makes the company’s future stock performance a key variable in determining the ultimate financial impact.

Strategic Analysis for Investors: What’s the Next Move?

The future trajectory of Exion Group stock hinges on several factors. The most crucial will be how effectively management deploys this new capital. Investors should demand clear communication regarding the specific business plans and monitor the company’s performance metrics closely over the coming quarters.

Short-Term vs. Long-Term Outlook

- •Short-Term: The key technical level to watch is the ₩1,672 conversion price. A sustained move above this price could attract momentum traders looking to capitalize on the positive sentiment.

- •Long-Term: The company’s fundamental performance is paramount. If the stock price languishes or declines, the ₩1,170 minimum adjustment price becomes a critical support level to monitor. A break below this could signal deeper issues.

In conclusion, the Exion Group convertible bond is a calculated risk aimed at fueling growth. While it presents a clear pathway to expansion, it also introduces potential dilution and financial obligations. Prudent investors will weigh both sides carefully, keeping a close eye on management’s execution and the stock’s price action relative to the key conversion levels outlined in this deal.

Disclaimer: This analysis is for informational purposes only and is based on publicly available information. It should not be construed as financial advice. All investment decisions should be made after conducting your own thorough research.