The recent L&K BIOMED CB conversion has become a major talking point for investors. L&K BIOMED CO., LTD. announced the exercise of convertible bond (CB) conversion rights, a financial maneuver that, while common, often creates uncertainty. The impending listing of over 240,000 new shares understandably raises concerns about short-term stock dilution. However, it also serves as a strong signal of positive company valuation, as the current stock price is trading well above the bond’s conversion price. This comprehensive analysis will explore the nuances of this event, dissecting the company’s fundamentals and the macroeconomic factors at play to provide investors with a clear, actionable outlook.

While the L&K BIOMED CB conversion may introduce short-term volatility, the company’s long-term trajectory hinges on fundamental improvements in profitability and strategic execution in its high-growth markets.

Event Overview: Deconstructing the CB Conversion

What Exactly Happened?

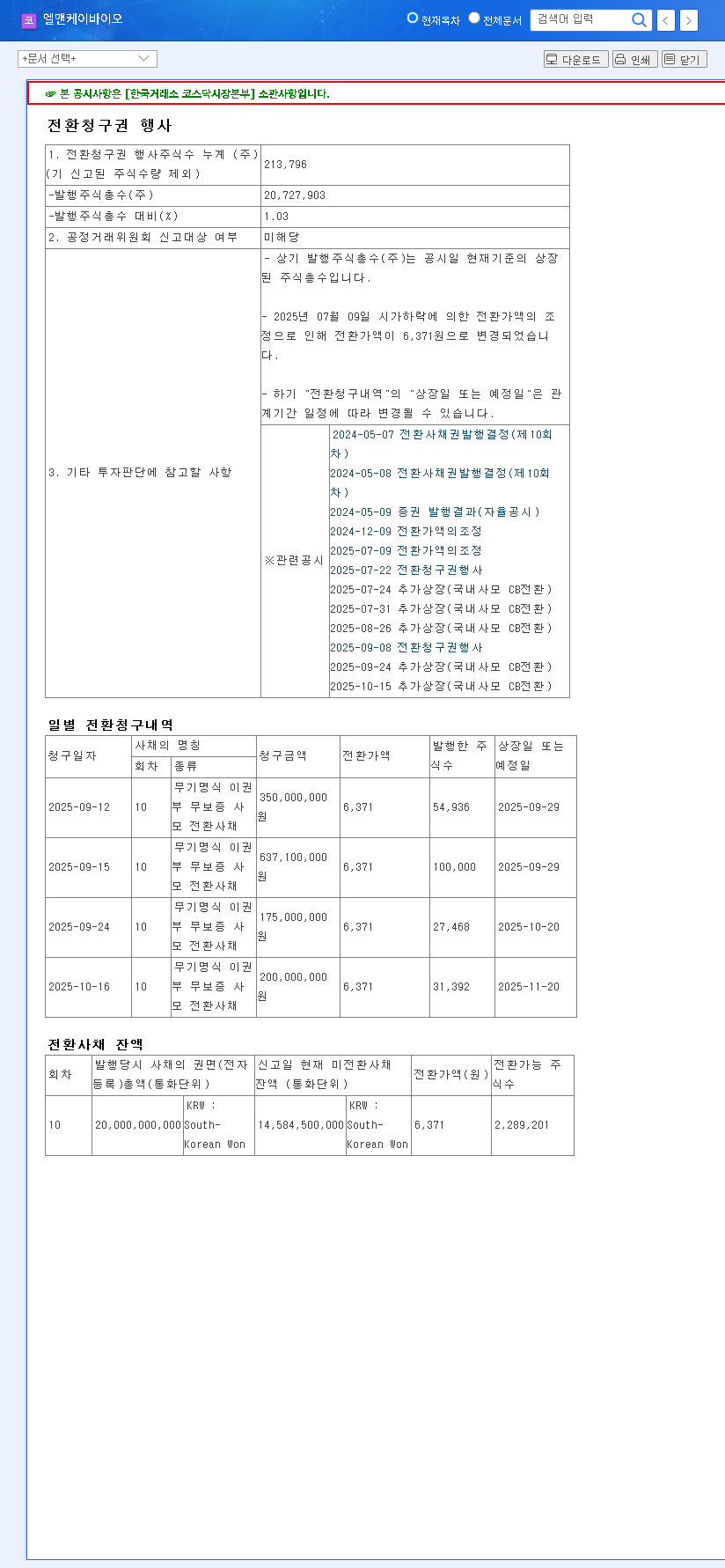

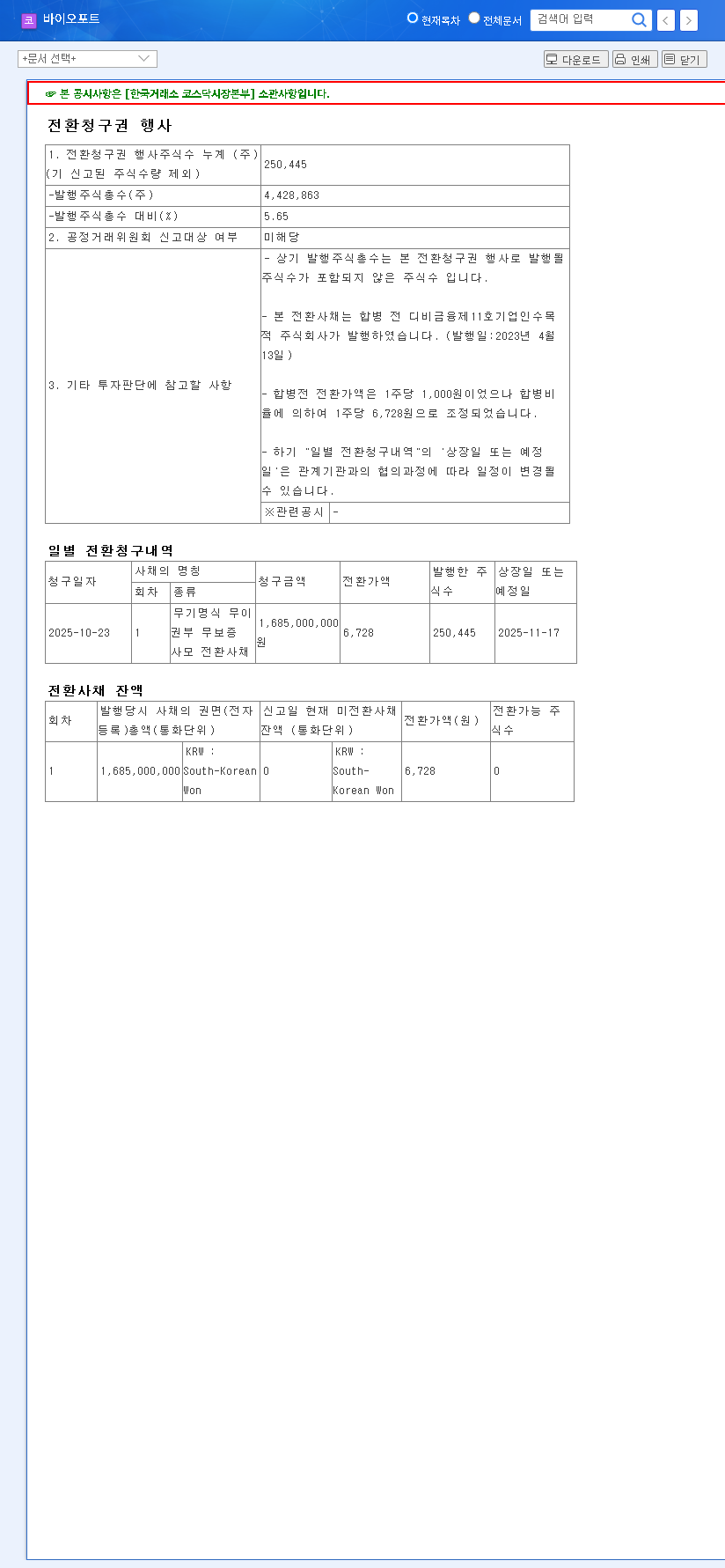

On October 27, 2025, L&K BIOMED (156100) confirmed that holders of its convertible bonds were exercising their right to convert that debt into equity. According to the Official Disclosure filed on DART, this action will result in the issuance of 245,313 new common shares. These shares, scheduled for listing on November 20, 2025, represent approximately 1.18% of the company’s market capitalization at the time of the announcement. The established conversion price is 6,371 KRW per share.

Why Is This Happening Now?

The primary catalyst for this conversion is a simple but powerful financial incentive. The market price of L&K BIOMED stock (9,680 KRW) is substantially higher—by over 50%—than the conversion price (6,371 KRW). This significant premium creates a compelling arbitrage opportunity for bondholders to convert their debt into more valuable stock and realize an immediate profit. From a broader perspective, this is a bullish indicator, suggesting that the market’s valuation of the company has grown considerably since the bonds were first issued. A convertible bond is a hybrid security that offers investors features of both debt and equity. For a deeper understanding, you can learn more about their mechanics from a high-authority source like Investopedia.

Analyzing the Impact on L&K BIOMED Stock

The convertible bond impact can be bifurcated into immediate, short-term effects and more crucial mid-to-long-term considerations tied to the company’s underlying health.

Short-Term: Navigating Dilution and Sentiment

The most immediate consequence is the potential for stock dilution. An increase in the number of outstanding shares means that the company’s earnings are spread thinner, which can negatively affect Earnings Per Share (EPS).

- •Price Pressure: The introduction of 1.18% new shares can create an overhang, potentially leading to downward pressure on the stock price as the market absorbs the new supply.

- •Investor Psychology: Existing shareholders may react cautiously, concerned about the dilution of their ownership stake. This can temporarily weaken investor sentiment.

- •Profit-Taking: The converting bondholders are likely to sell some of their newly acquired shares to lock in profits, adding to the selling pressure in the near term.

Mid-to-Long-Term: Fundamentals are Paramount

While the capital structure changes, the L&K BIOMED CB conversion has a limited direct effect on the company’s core business operations. The long-term stock performance will be dictated by its ability to generate profits and execute its growth strategy. A critical point of concern is the reported net loss of 30.14 billion KRW in the first half of 2025. This was attributed to rising SG&A expenses and other costs. Future stock appreciation depends heavily on management’s ability to control these costs and improve profitability. On the other hand, L&K BIOMED has several powerful growth drivers:

- •Strong Overseas Growth: Sales from the Americas have been robust, showcasing strong international demand.

- •Market Potential: The global spinal implant market is a growing sector, providing a favorable tailwind.

- •Innovation Pipeline: With FDA-approved products and expansion into new areas like thoracic implants, the company demonstrates strong R&D capabilities. For more detail, you can read our complete overview of L&K BIOMED’s product pipeline.

Investor Action Plan & Strategic Outlook

Given the circumstances, a measured and informed approach is essential. Investors should consider the following strategic points:

- •Monitor Profitability Metrics: Pay close attention to upcoming quarterly earnings reports. Look for signs of improving margins, effective cost controls, and tangible revenue from new business segments.

- •Assess Further Dilution Risk: Keep an eye on the company’s balance sheet and financial statements for any indication of future convertible bond issuances or other dilutive financing activities.

- •Track Macroeconomic Factors: As a global company, L&K BIOMED is exposed to currency fluctuations. Monitor the USD/KRW exchange rate and global interest rate trends, as they can impact both revenue and investor sentiment.

In conclusion, the L&K BIOMED CB conversion is a classic case of short-term pain for potential long-term gain. While the immediate stock dilution is a valid concern, the event itself underscores the market’s growing confidence in the company’s value. Prudent investors should look past the near-term noise and focus on the fundamental execution that will truly drive the value of their L&K BIOMED stock over time.