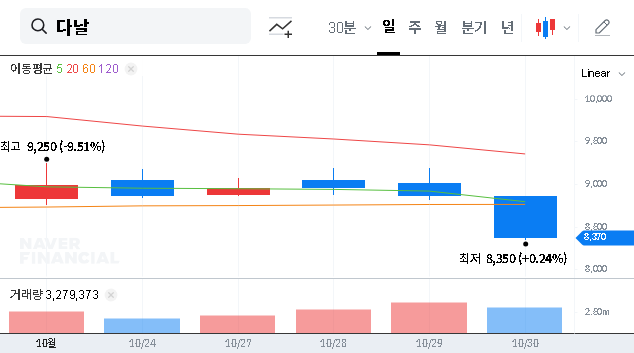

The outlook for RN2 Technologies stock (KRX: 148250) has entered a new phase of speculation and analysis following a significant financial maneuver. RHC Investment Partners has acquired a substantial stake via convertible bonds (CBs), prompting investors to question the future trajectory of the company’s share price and fundamental value. This deep-dive report unpacks the event, analyzes its potential impact, and provides a clear investment strategy to navigate the opportunities and risks ahead.

We’ll explore everything from the specifics of the deal to the core business of RN2 Technologies, ensuring you have the comprehensive insight needed for informed decision-making.

The Catalyst: RHC’s Convertible Bond Acquisition

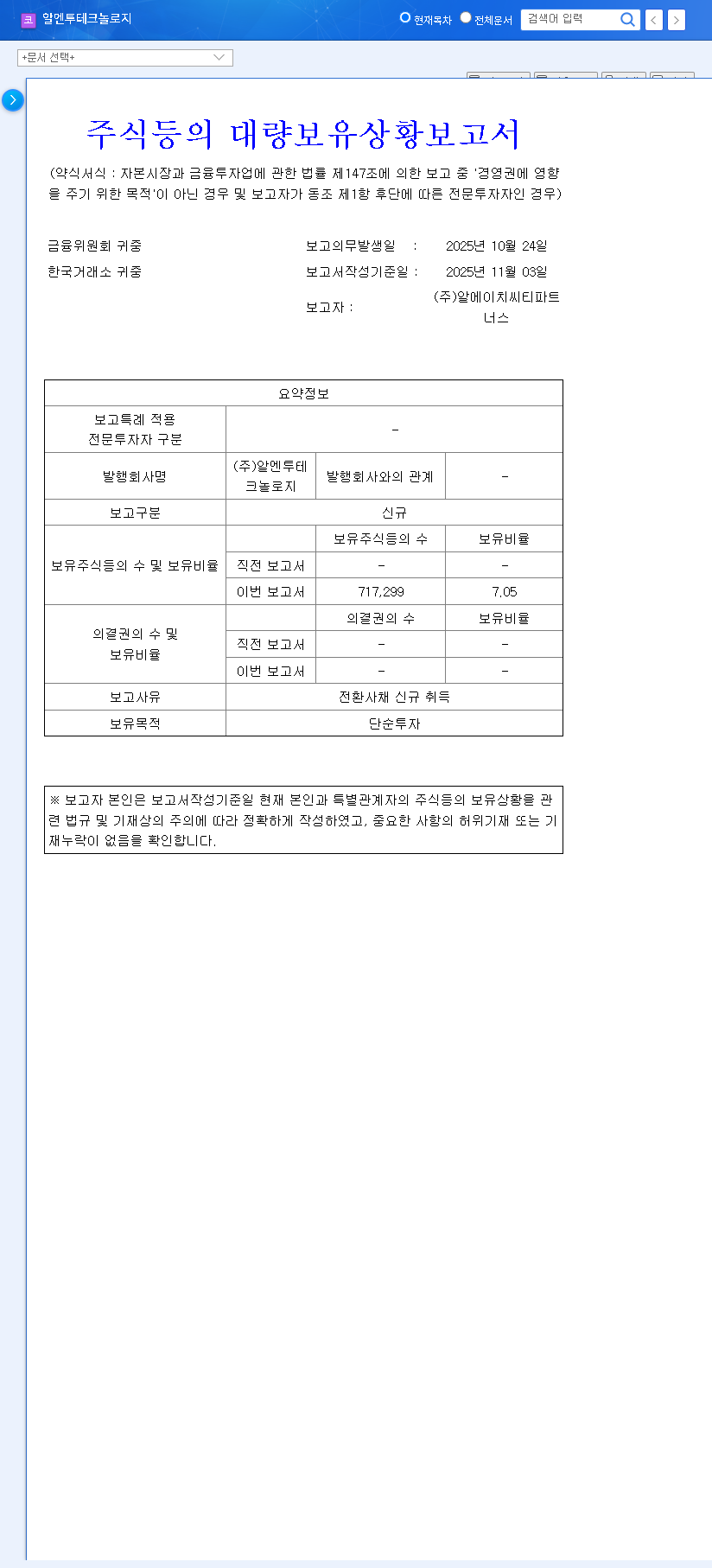

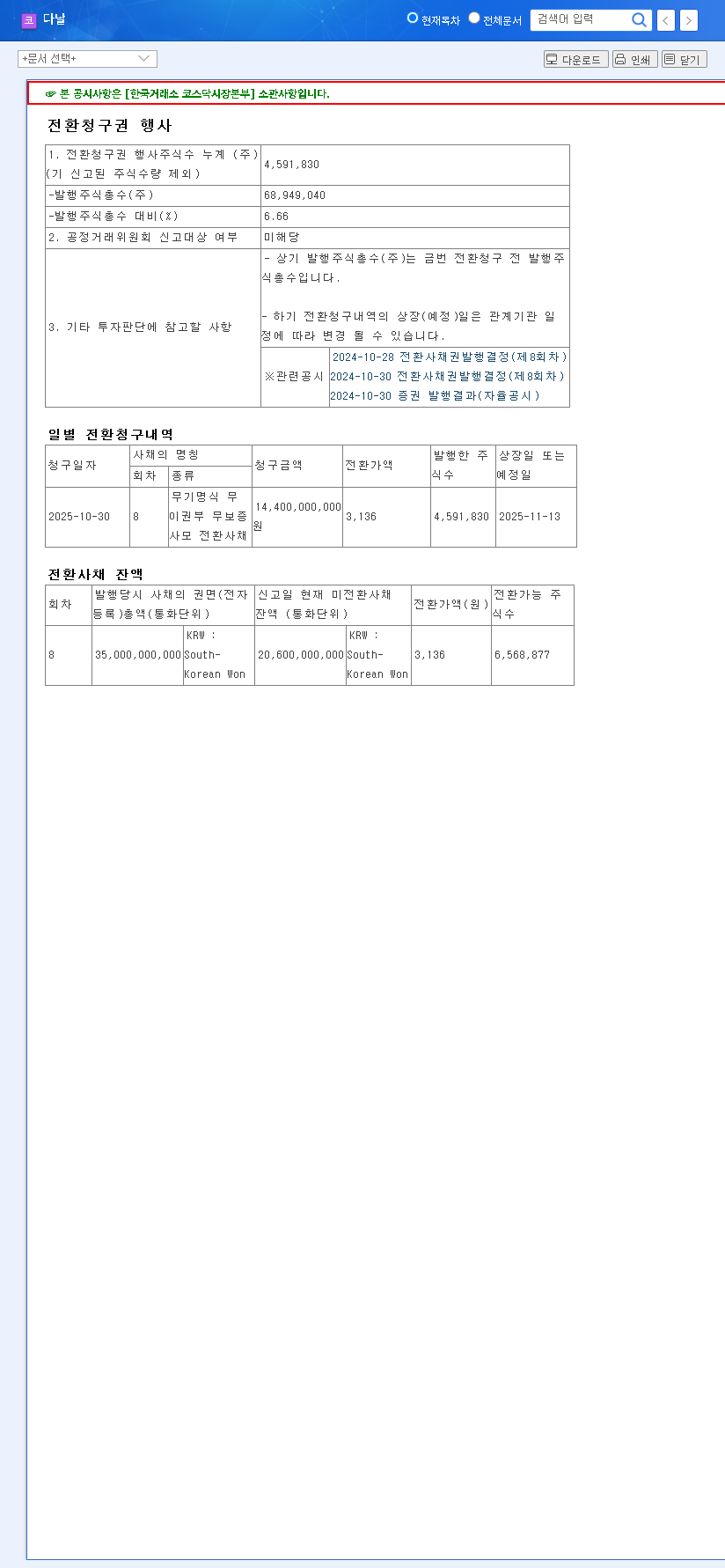

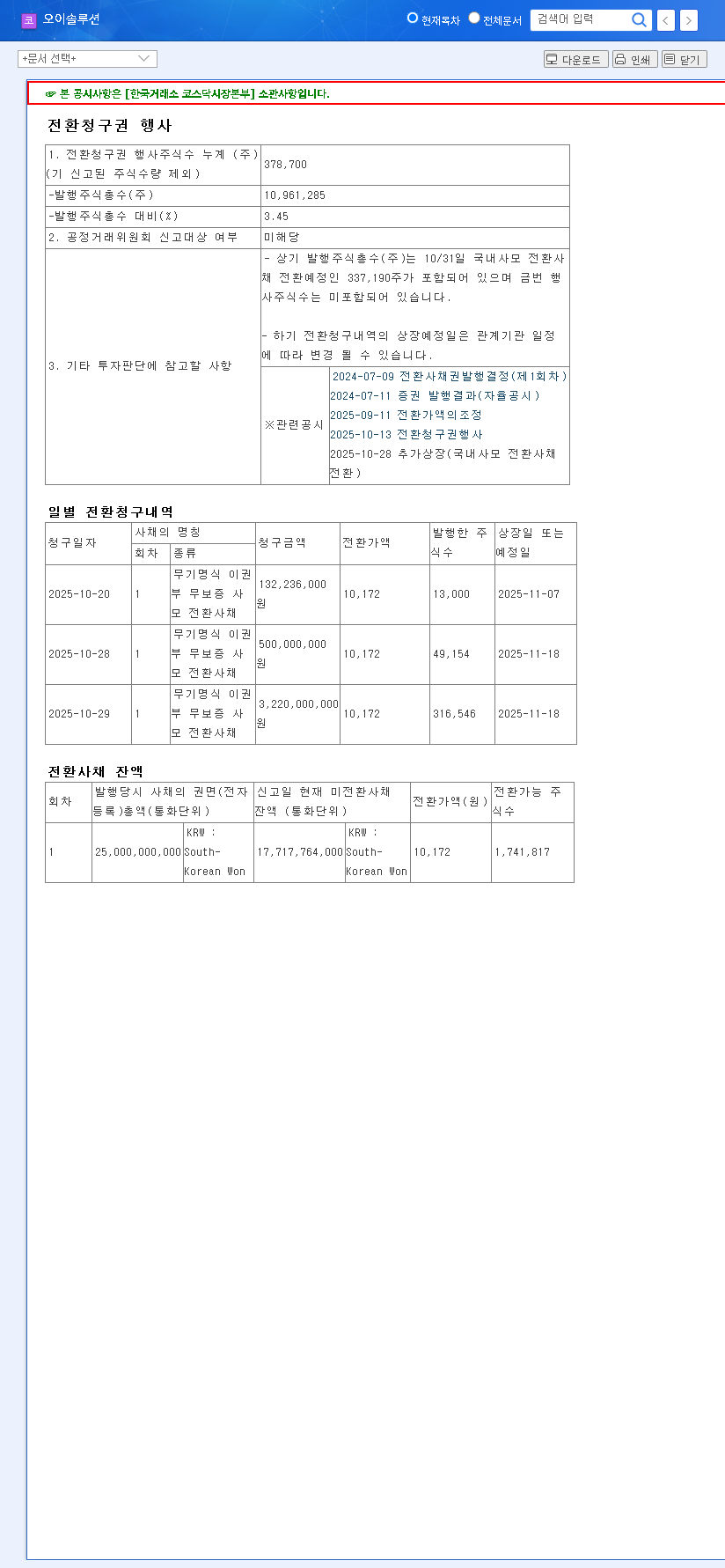

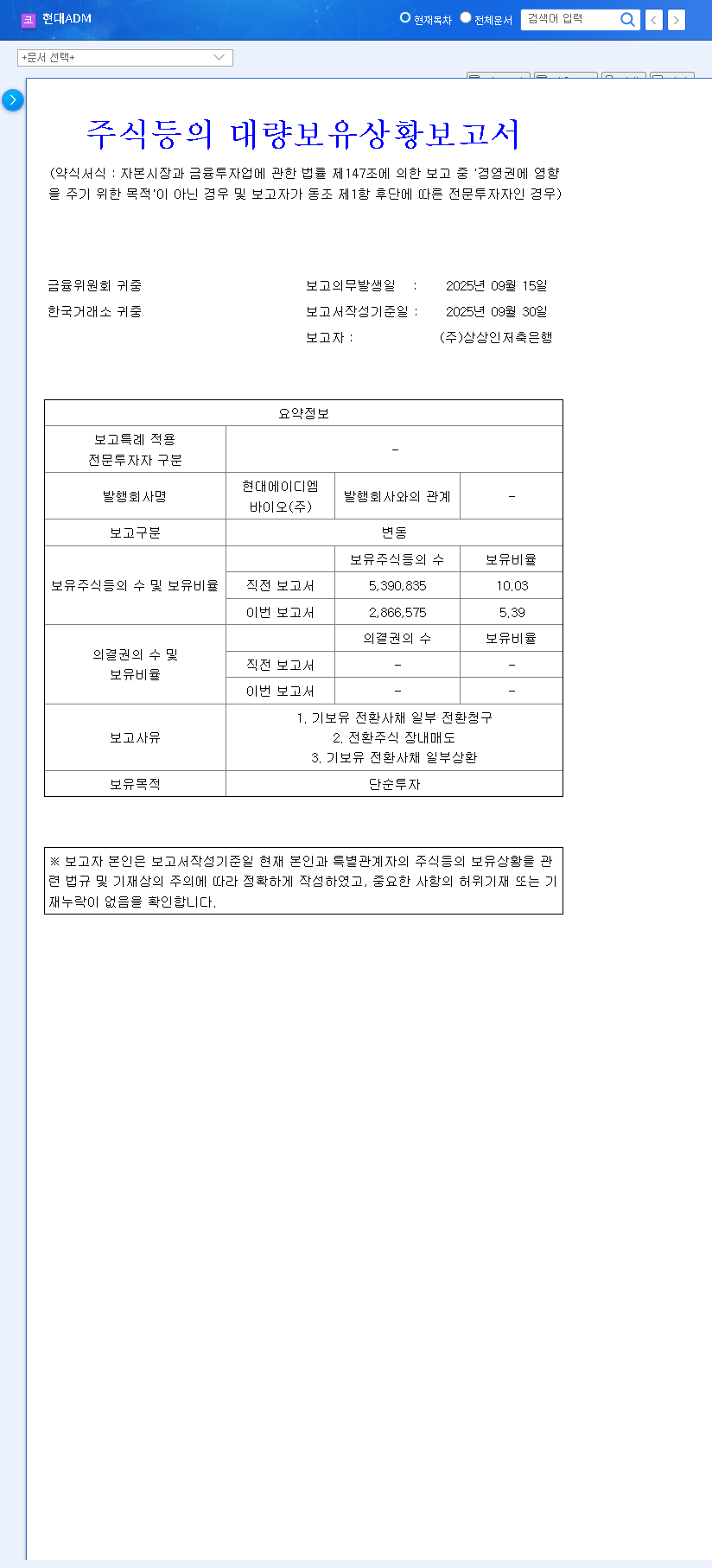

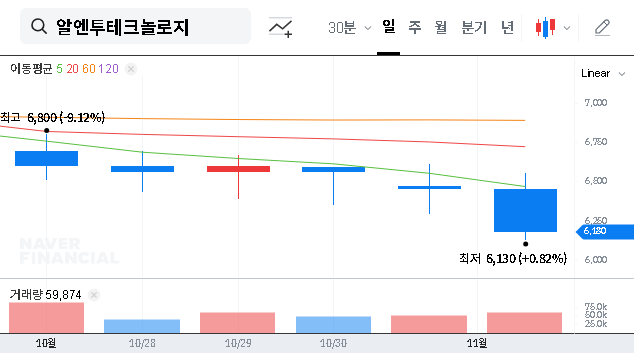

On November 3, 2025, the market took notice when RHC Investment Partners filed a large-scale holding report concerning RN2 Technologies Co., Ltd. According to the Official Disclosure, the core of this event is the acquisition of new convertible bonds that, if converted, would represent a 7.05% stake in the company. While the stated purpose is ‘simple investment,’ such a move always warrants closer inspection.

- •Reporting Entity: RHC Investment Partners

- •Target Company: RN2 Technologies Co., Ltd. (148250)

- •Key Detail: New acquisition of convertible bonds (CBs) for a 7.05% potential stake.

- •Stated Purpose: Simple investment.

Who is RN2 Technologies? A Look at the Core Business

To understand the investment, one must first understand the company. RN2 Technologies is a specialized manufacturer of radio frequency (RF) components. These are not everyday consumer items but are critical building blocks for advanced technology, primarily in the telecommunications and defense industries. Their products, such as couplers, attenuators, and terminators, are essential for managing signal power in 5G base stations and sophisticated military radar systems. While the company has demonstrated consistent revenue growth, driven by the global 5G rollout, its profitability has been a persistent challenge, making this new capital infusion a pivotal event.

Understanding Convertible Bonds: A Double-Edged Sword

A convertible bond is a hybrid security—it starts as a loan (a bond) that pays interest, but it gives the holder the option to convert it into a predetermined number of common shares. This unique structure presents both opportunities and risks. You can learn more about the technicals from high-authority sources like Investopedia.

The Upside: A Vote of Confidence and Flexible Capital

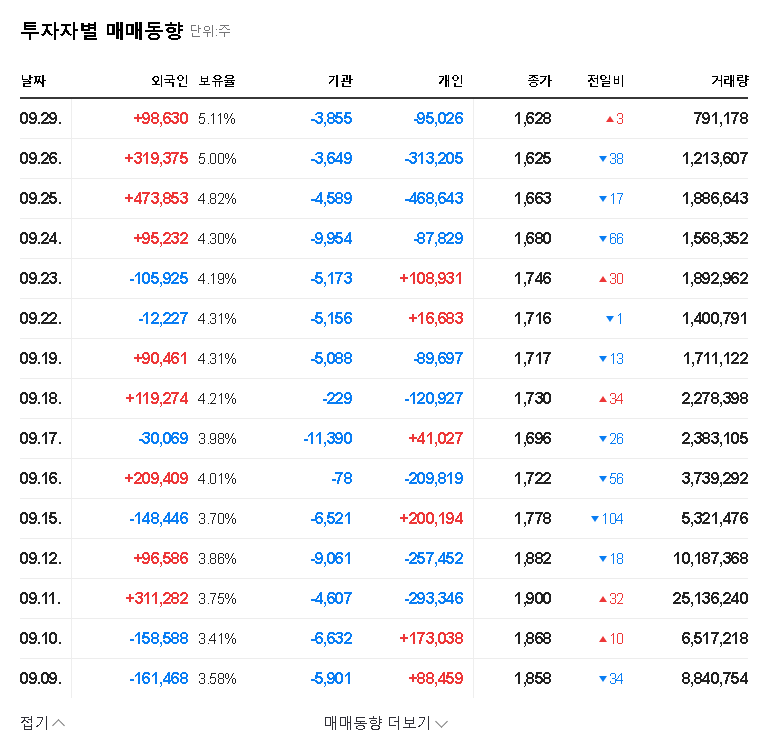

RHC’s investment signals a positive assessment of RN2 Technologies’ future. They are betting on the company’s growth potential. For RN2, this provides crucial capital that can be used for R&D, expanding production, or improving its financial structure without the immediate dilution that a direct stock offering would cause.

The Downside: The Threat of Future Share Dilution

The primary risk for existing shareholders is dilution. If and when RHC converts these bonds into stock, the total number of outstanding shares will increase. This can decrease the ownership percentage and earnings per share for existing investors, potentially putting downward pressure on the stock price.

While the entry of a new, significant investor is a vote of confidence, the path for RN2 Technologies stock is now influenced by the dual forces of growth potential and the overhang of potential dilution.

Analyzing the Impact on RN2 Technologies Stock

The immediate impact on the RN2 Technologies stock price is likely neutral to slightly positive, driven by market sentiment. However, the long-term direction will depend entirely on how events unfold.

Short-Term Market Reaction

In the short term, the news may attract traders and generate positive buzz. However, savvy investors will remain cautious, aware of the potential for dilution. This creates a balance between buying interest and watchful waiting, likely leading to increased volatility but no major breakout without further news.

Medium to Long-Term Fundamental Drivers

The long-term performance hinges on two factors: RHC’s strategy and RN2’s execution. Will RHC remain a passive investor, or will they seek to influence management? More importantly, can RN2 Technologies use this opportunity to finally solve its profitability challenges and capitalize on its strong position in the 5G market? The ultimate driver of the stock price will be tangible improvements in the company’s intrinsic value.

A Prudent Investment Strategy

Given the mix of potential and risk, a cautious and well-researched approach is essential. Investors should consider the following steps:

- •Monitor CB Conversion Terms: Keep a close eye on the conversion price and maturity date of the bonds. Any moves by RHC to convert will be a significant market signal.

- •Track Fundamental Performance: Focus on quarterly earnings reports. Look for margin improvements and updates on new contracts or technological advancements. This is more important than the daily stock price fluctuations.

- •Analyze the Broader Sector: The performance of the RN2 Technologies stock is tied to the 5G and defense sectors. Read our latest analysis of 5G component manufacturers for broader context.

- •Adopt a Long-Term Perspective: This event is not a short-term catalyst for a massive price surge. Real value creation will take time. Only invest if you believe in the company’s long-term ability to improve its fundamentals.

Frequently Asked Questions (FAQ)

Q1: What is the single most important event for RN2 Technologies right now?

A1: The acquisition of convertible bonds representing a potential 7.05% stake by RHC Investment Partners. It introduces a significant new investor and potential for both capital infusion and share dilution.

Q2: Is this CB acquisition good or bad for RN2 Technologies stock?

A2: It’s neutral with both positive and negative potential. It’s positive because it shows confidence from an institutional investor. It’s negative due to the risk of future share dilution, which could harm existing shareholders’ value.

Q3: How does this affect existing shareholders?

A3: If the bonds are converted to stock, the total number of shares increases, which can dilute the value and ownership percentage of existing shareholders. The stock price may become more volatile as the market anticipates the conversion.

Q4: What should I watch for as an investor?

A4: Focus on the company’s fundamental improvements—specifically, whether they can improve profitability. Also, monitor any news regarding RHC’s investment strategy and the timing of a potential bond-to-stock conversion.