The recent news of the KPF CB redemption has captured significant market attention. KPF (케이피에프), a key player in industrial fasteners and automotive parts, announced its decision to redeem KRW 4.5 billion in convertible bonds (CBs). This move is far more than a simple balance sheet adjustment; it’s a powerful statement about the company’s confidence in its future and a direct commitment to enhancing KPF shareholder value. This detailed analysis will unpack the specifics of the redemption, its strategic implications, and provide a comprehensive KPF stock analysis for investors considering their next move.

The Details: KPF’s Convertible Bond Redemption Announcement

On November 14, 2025, KPF officially disclosed its decision to redeem its 8th series of unregistered, unsecured private convertible bonds. This strategic financial action involves a significant sum and has clear objectives tied to the company’s long-term shareholder return policy.

- •Event: Redemption of KRW 4.5 billion in treasury convertible bonds.

- •Primary Goal: A direct initiative to enhance shareholder value and prevent share dilution.

- •Key Impact: Eliminates the potential overhang of 1,096,224 shares (based on a KRW 4,105 conversion price) from entering the market.

- •Official Source: The details were confirmed in an Official Disclosure via DART, providing full transparency.

This action follows the shareholder return policy announced earlier in October, reinforcing management’s commitment to its stated goals and building trust with the investment community.

By proactively retiring these convertible bonds, KPF is sending an unequivocal message: the current share price does not reflect the company’s intrinsic value, and management is dedicated to protecting existing shareholders from future dilution.

Analyzing the Impact: What This Means for KPF and Investors

The decision to execute a KPF CB redemption is a multi-faceted event with significant positive implications, though it’s also important to consider the complete picture.

The Upside: A Clear Path to Higher Shareholder Value

- •Elimination of Stock Dilution: Convertible bonds represent potential future shares. By buying them back, KPF prevents the share count from increasing. This directly boosts Earnings Per Share (EPS), a key metric investors use to value a company, as profits are divided among fewer shares.

- •Improved Financial Structure: Removing KRW 4.5 billion in debt from the balance sheet strengthens the company’s financial health. This can lead to improved credit metrics and lower future borrowing costs, contributing to long-term stability.

- •Enhanced Investor Confidence: Actions speak louder than words. This redemption demonstrates that management is actively working to create value, which can attract long-term investors and foster a positive market sentiment around the stock.

A Balanced Perspective: Short-Term Considerations

While overwhelmingly positive, the redemption involves a KRW 4.5 billion cash outlay. However, given KPF’s recently improved operating cash flow and solid financial standing, this is viewed as a manageable expenditure that represents a strategic investment in its own equity rather than a financial strain.

Beyond the Redemption: KPF’s Core Business Fundamentals

A comprehensive KPF stock analysis must look beyond this single event. The company’s underlying business strength is crucial for sustained growth.

KPF boasts a diversified business portfolio across industrial fasteners, automotive parts, and shipbuilding cables. Its global strategy is a key strength, with subsidiaries in Vietnam, Japan, and China helping to secure cost competitiveness. Critically, the establishment of its U.S. subsidiary, TMC Texas Inc., positions KPF to capitalize on the ‘Buy America’ policy, a significant potential growth driver. This strategic move is explained in more detail in major financial publications like Bloomberg.

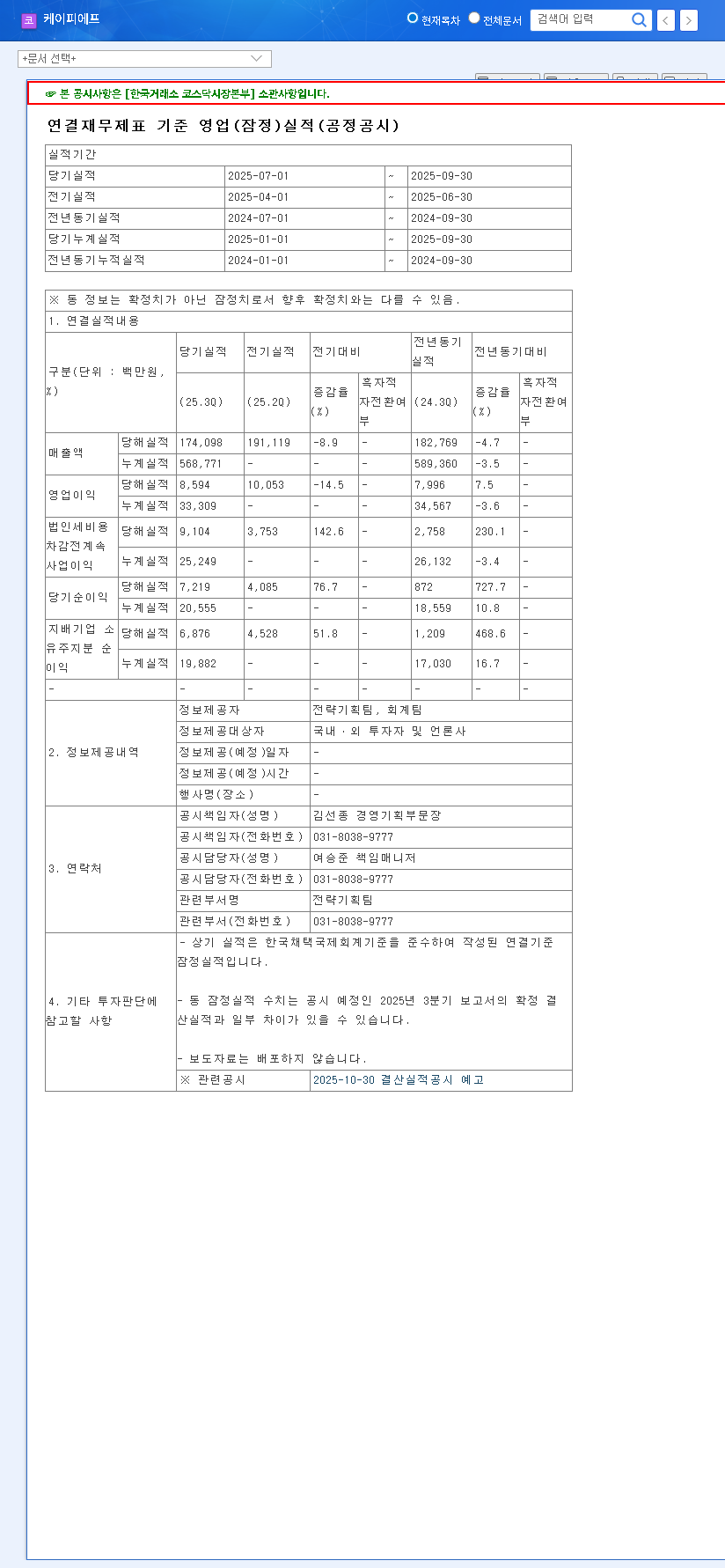

Despite a slight revenue dip in Q3 2025, the company maintained strong operating profitability, underscoring its operational efficiency. The noted recovery in the shipbuilding cable segment is another positive indicator. However, investors should remain aware of risks such as raw material price volatility, foreign exchange fluctuations, and the potential impact of regulations like the EU’s Carbon Border Adjustment Mechanism (CBAM).

Investment Thesis and Final Outlook

The KPF CB redemption is a decidedly positive catalyst for the company. It serves as a strong vote of confidence from management and directly addresses the issue of potential share dilution, paving the way for a higher valuation and improved KPF shareholder value.

Recommendations for Investors

- •Short-Term: The redemption news is likely to provide positive momentum for the stock. Investors should watch for increased trading volume and positive price action as the market digests this information.

- •Mid- to Long-Term: The focus should be on KPF’s execution of its growth strategy. Monitor the progress of its U.S. expansion, the performance of its core business segments, and the ongoing commitment to shareholder returns. For more details on their financials, see our Deep Dive into KPF’s Q3 Earnings.

In conclusion, KPF’s strategic bond redemption, coupled with its solid operational fundamentals and global expansion plans, presents a compelling case for a positive investment outlook.