The latest CJ CGV Q3 2025 earnings report presents a complex picture for investors. While certain divisions show promise, the headline figures reveal significant challenges, with operating profits missing targets and net income slipping into a deficit. This comprehensive CJ CGV financial analysis will dissect the provisional Q3 results, explore the underlying causes of the underperformance, identify potential silver linings, and offer a strategic outlook for those monitoring CJ CGV stock.

Understanding the nuances of this report is critical for making informed decisions. We will examine how the company’s core business is faring against macroeconomic headwinds and what its future trajectory might look like. For context, you can also review our previous analysis of CJ CGV’s Q2 2025 performance.

CJ CGV Q3 2025 Earnings: The Official Numbers

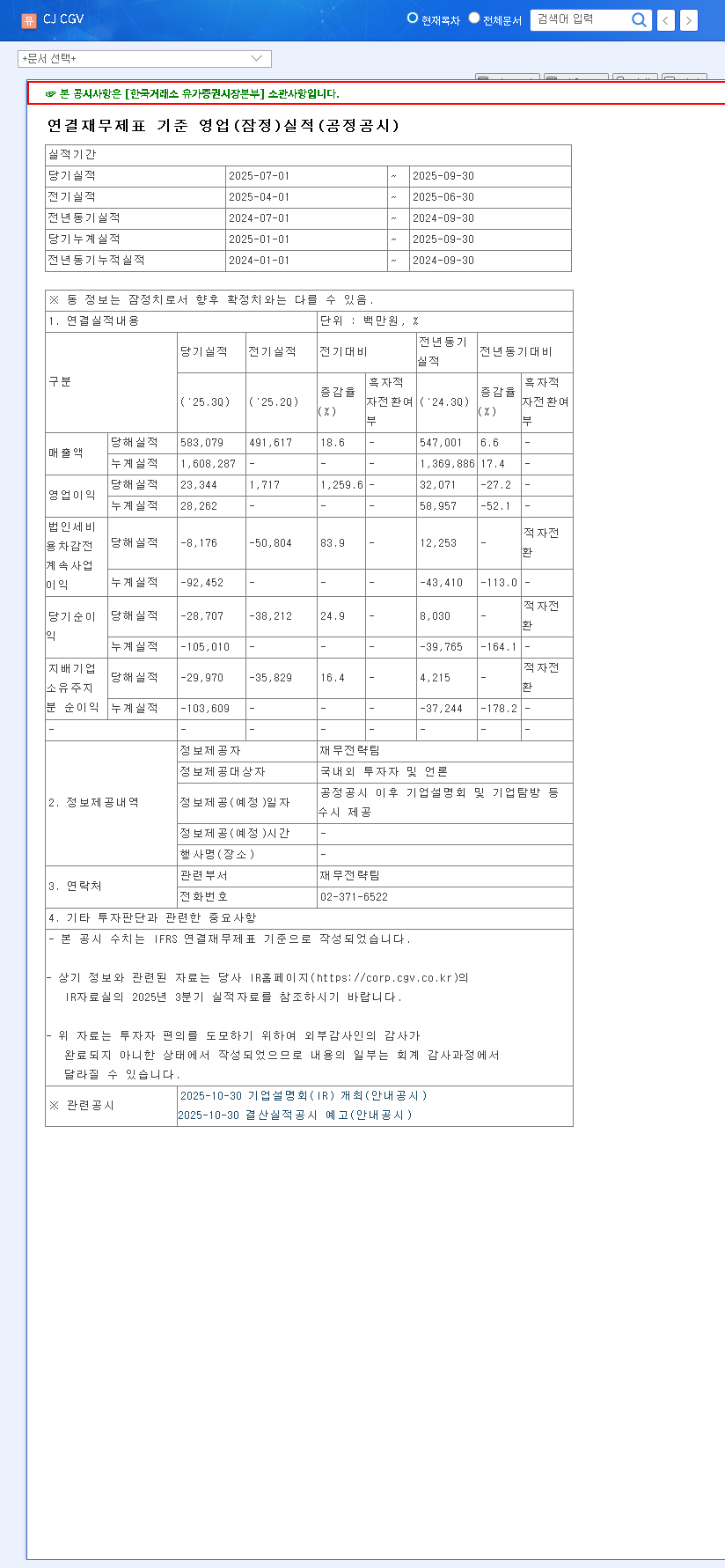

CJ CGV CO.,LTD. released its provisional earnings for the third quarter of 2025, revealing a mixed bag of results that warrant careful examination. This analysis is based on data from the company’s public filing. Source: Official Disclosure. Here are the key financial highlights:

- •Revenue: KRW 583.1 billion. This figure slightly surpassed market consensus, driven by positive growth in the IT service division and a partial recovery in key overseas markets.

- •Operating Profit: KRW 23.3 billion. A significant miss compared to market expectations and a decrease year-over-year, primarily due to the deteriorating profitability of the core multiplex cinema operations.

- •Net Income: KRW -30.0 billion. The company shifted to a net deficit, a concerning development caused by the combination of lower operating profit, rising financial costs, and losses related to foreign exchange fluctuations.

Despite bright spots in technology and content, the sluggish performance of the core cinema business has dragged down overall results, while high debt levels are amplifying financial risks in the current economic climate.

Why the Underperformance? Analyzing the Core Challenges

The disappointing CJ CGV Q3 2025 earnings are not the result of a single issue, but a convergence of internal and external pressures.

Weakening Core Business Profitability

The primary drag on performance is the multiplex division. Persistently weak box office results, both domestically and internationally, have led to lower attendance figures. This is compounded by rising operational costs, including everything from energy and rent to personnel and marketing, which have squeezed profit margins thin.

Deepening Financial Health Concerns

The company’s financial structure is under strain. The shift to a net deficit makes it harder to pursue financial improvements through capital increases. Furthermore, a high debt ratio in a period of sustained high interest rates, as noted by leading financial experts, dramatically increases interest payment burdens, directly eroding any profits generated from operations. Volatility in foreign exchange markets also poses a significant risk for a company with a large international footprint like CJ CGV.

Silver Linings & Future Growth Drivers

While the headline numbers are concerning, the report wasn’t entirely negative. A closer look at the CJ CGV performance reveals strategic areas that are showing strength and could become future growth engines.

- •IT & Technology Services: This division reported notable growth, indicating that the company’s investments in technology and digital solutions are paying off.

- •Special Theaters (4DX, ScreenX): Technology-focused premium formats continue to perform well, attracting audiences willing to pay for a differentiated, high-value experience that cannot be replicated at home.

- •Content Business: The company’s content arm also showed positive results, highlighting the strategic importance of controlling a pipeline of exclusive and engaging content for its screens.

These successes demonstrate that CJ CGV’s diversification strategy is bearing fruit. The key challenge will be leveraging these strengths to support and ultimately revitalize the core cinema business.

Investor Guide: A Cautious but Watchful Approach

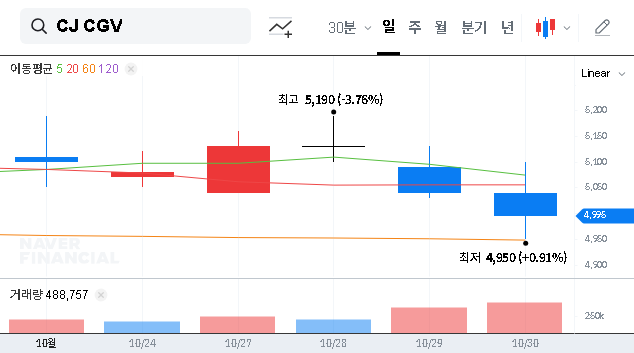

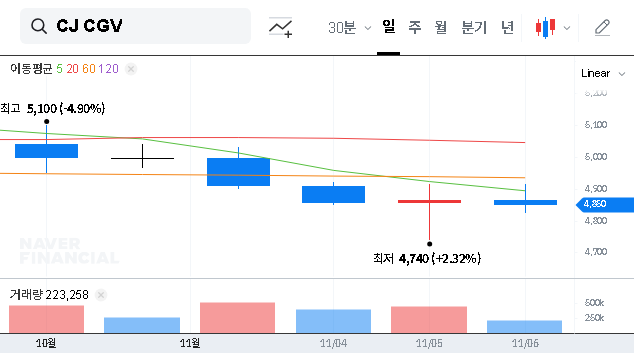

Given the current uncertainties, a cautious approach to CJ CGV stock is warranted. Investors should adopt a long-term perspective and closely monitor several key areas.

Monitor Financial Restructuring Efforts

Keep a close eye on the company’s plans to improve its financial health. This includes any announcements regarding asset sales, capital increases, or debt refinancing. Tangible progress in reducing the debt ratio is a critical milestone for recovery.

Track Core Business Turnaround Strategy

The path to sustained profitability runs through the multiplex division. Watch for strategies aimed at securing blockbuster content, enhancing the competitiveness of premium screens, and improving the overall customer experience to drive foot traffic.

Assess the Macroeconomic Landscape

External factors will continue to play a huge role. Pay attention to interest rate trends, foreign exchange movements, and shifts in consumer spending habits, as these will all impact CJ CGV’s bottom line.

In conclusion, the CJ CGV Q3 2025 earnings report highlights a company at a crossroads. While significant financial and operational hurdles remain, its strategic investments in technology and content provide a potential pathway to future growth. A patient, long-term view focused on fundamental improvements is the most prudent course of action for investors.