This comprehensive BGF retail investment analysis provides a deep dive into the company’s fundamentals and strategic outlook ahead of a pivotal event. On November 17, 2025, BGF retail CO., LTD. will host its Investor Relations (IR) conference to present its Q3 2025 financial results. This event is more than just a numbers release; it’s a critical window into the company’s future vision, market strategy, and overall health, drawing significant attention from investors looking to understand the potential of BGF retail stock.

We will explore the core strengths of BGF retail, its ambitious global expansion, and the potential impact of this IR event. Our goal is to equip you with the insights needed to make informed decisions and identify whether this represents a promising opportunity in the competitive convenience store investment landscape.

BGF Retail Q3 2025 IR: A Critical Overview

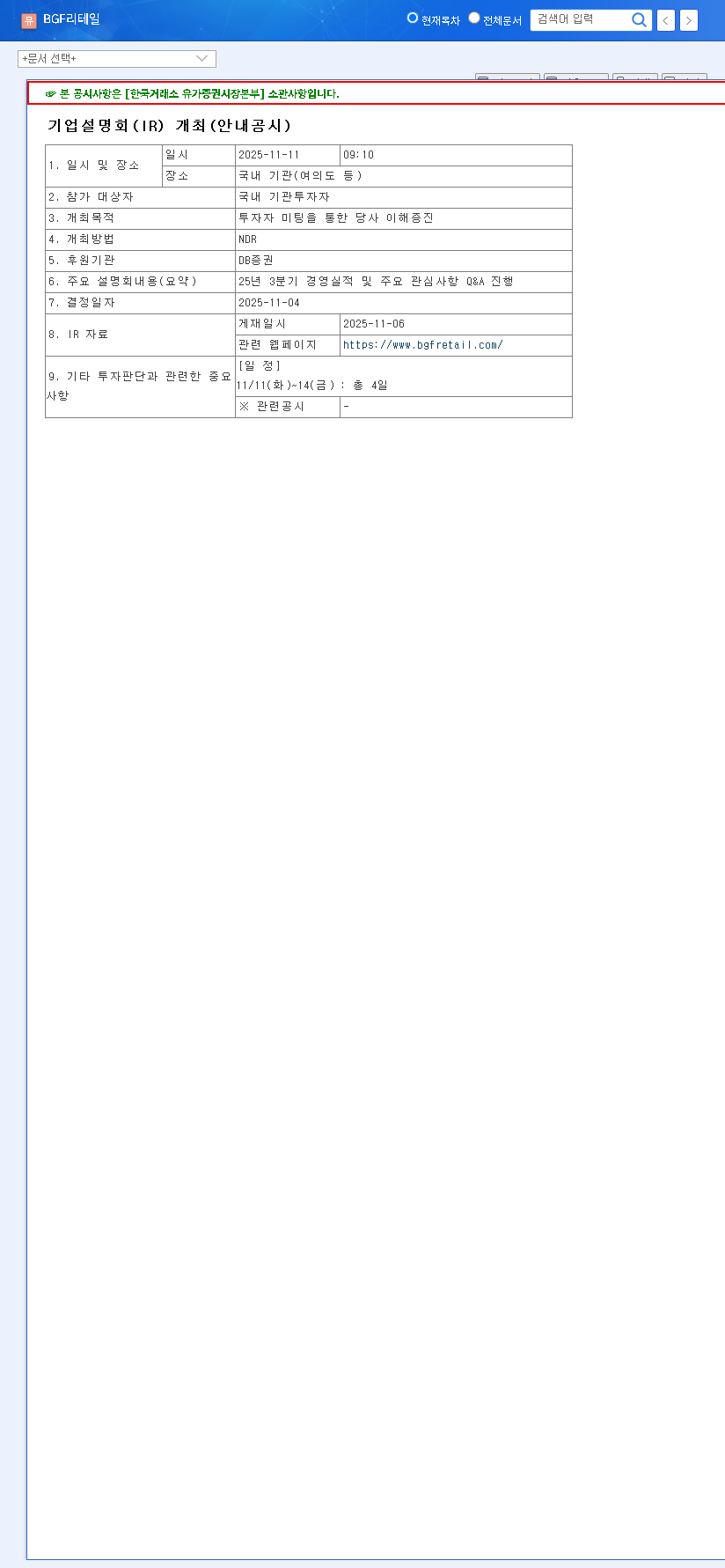

Scheduled for 10:00 AM on November 17, 2025, the IR conference is a key event for the investment community. The agenda is twofold: to present the Q3 2025 earnings and to hold an interactive Q&A session. This allows analysts and investors to probe into management’s strategy, operational performance, and outlook, providing transparency that can significantly influence market sentiment. For the latest official filings, you can view the company’s Official Disclosure on DART.

Core Fundamentals: A BGF Retail Investment Analysis

A thorough BGF retail investment analysis begins with its solid fundamentals. The first half of 2025 has already shown a trajectory of robust operations and strategic growth, particularly in overseas markets.

Dominance in the Convenience Store Sector

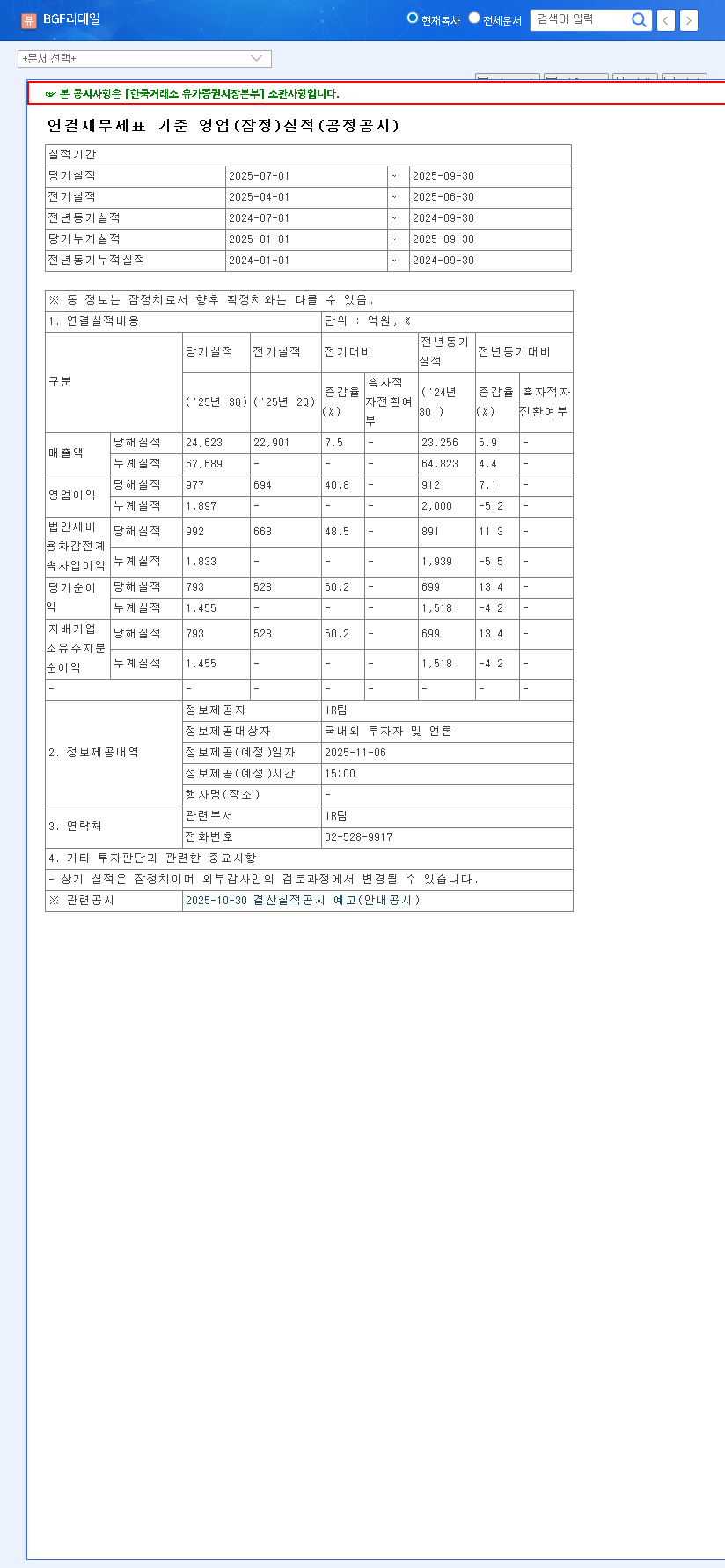

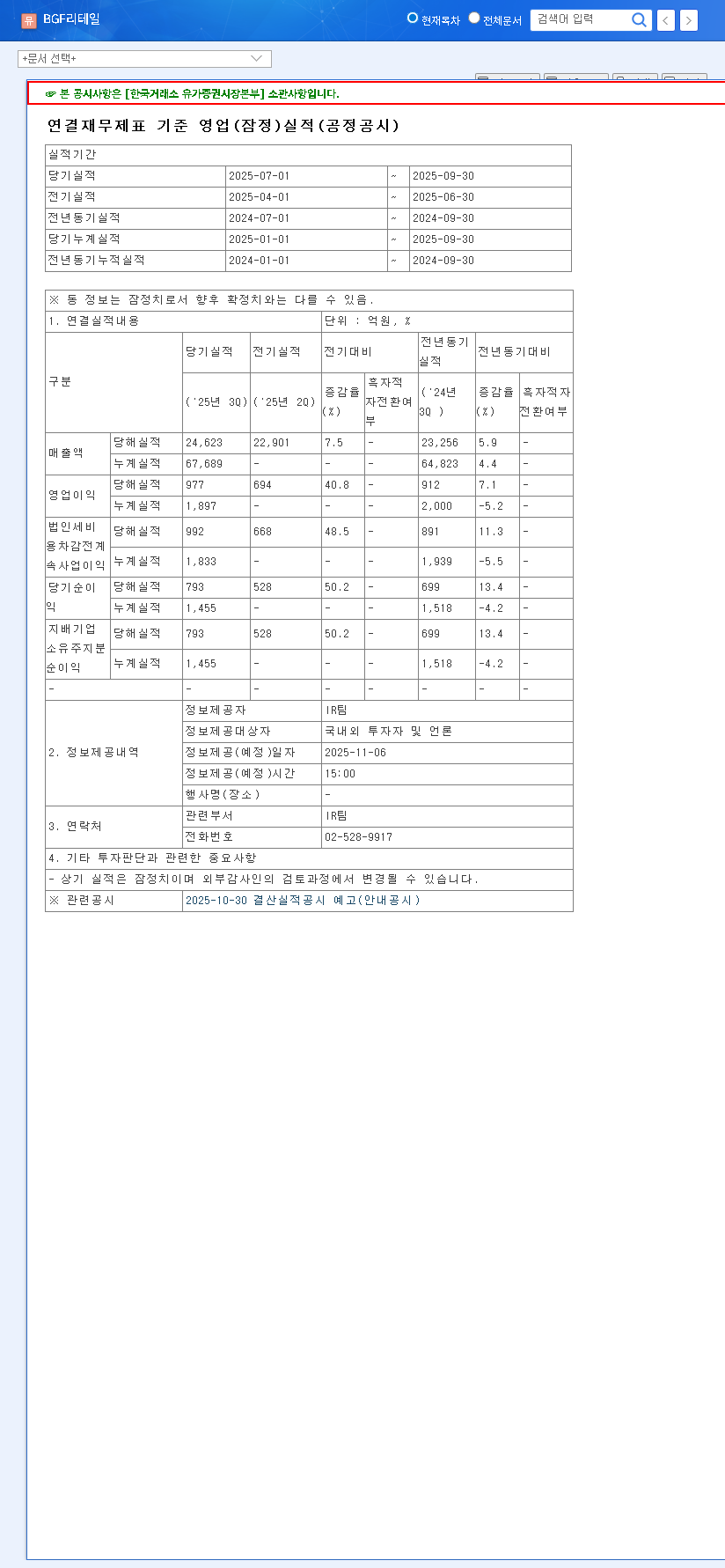

The core business continues to thrive, capitalizing on societal shifts like the rise of single and two-person households. This demographic trend boosts demand for convenient, accessible retail solutions. In H1 2025, BGF Retail reported impressive figures with revenue of KRW 4.2136 trillion and an operating profit of KRW 83.4 billion, underscoring its strong market position and profitability.

Synergistic Subsidiaries & Global Expansion

Beyond its primary retail operations, BGF’s subsidiaries in logistics, food manufacturing, and e-commerce provide a stable, diversified income stream. These segments are not just profitable but also create powerful synergies that enhance the efficiency of the entire ecosystem. The company’s most exciting growth story, however, is its international expansion. Key strategic moves include:

- •Establishing a strong brand presence in emerging markets like Mongolia, Malaysia, and Kazakhstan.

- •Entering the U.S. market with new locations in Hawaii, securing new revenue streams and boosting global brand recognition.

- •Investing KRW 189.5 billion in a new Busan logistics center to enhance operational efficiency, with completion expected by late 2026.

Financial Health and Market Position

While a consolidated debt-to-equity ratio of 188% might seem high, it’s essential to look deeper. When accounting for franchise deposits and right-of-use assets, the company demonstrates a stable operating cash flow of KRW 310.9 billion, sufficient to service its debt comfortably. BGF Retail maintains a competitive edge through innovative private-label products and differentiated services, a crucial factor in a highly competitive market. For more on sector trends, see this analysis of the global retail market.

The key takeaway for investors is that BGF Retail’s strategy is not just about domestic saturation but aggressive and calculated international growth, which could unlock significant long-term value for the BGF retail stock.

Scenarios: Analyzing the IR Event’s Impact

The IR event’s outcome can steer investor sentiment in several directions. Here are the most likely scenarios:

- •Bull Case (High Probability): If the Q3 2025 earnings beat expectations and management provides a confident, clear vision for future growth—especially in overseas markets—the stock could see a significant positive reaction. A transparent Q&A that builds investor trust is crucial.

- •Neutral Case (Medium Probability): Should the earnings meet market consensus without any major surprises, the stock may see limited short-term movement. The focus would then shift to macroeconomic factors, which you can track on platforms like Bloomberg.

- •Bear Case (Low Probability): An earnings miss, a lowered future outlook, or evasive answers during the Q&A could erode investor confidence and negatively impact the stock price.

Investment Thesis and Key Monitoring Points

Our current investment opinion on BGF retail CO., LTD. is ‘Neutral’ with a positive bias, pending the results of the upcoming IR. The company’s strong market position and growth potential are compelling, but the execution of its strategies post-IR will be the deciding factor.

Investors should closely monitor the following points to make timely decisions:

- •Detailed Q3 2025 financial metrics (revenue, profit, segment performance).

- •Management’s commentary on overseas expansion progress and profitability.

- •Updates on the efficiency gains from new logistics investments.

- •Competitor movements and changes in domestic market share.

- •Short and long-term stock price reaction following the IR event.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. Investment decisions should be made based on individual research and judgment. Market conditions can change rapidly.