The latest financial release from APR Co., Ltd. (278470) has sent a clear message to the market: the growth story is far from over. The definitive APR Q3 2025 earnings surprise not only crushed analyst consensus but also effectively erased the concerns about slowing growth that emerged from the first half of the year. This report confirms the company’s robust fundamentals and dominant position in the competitive beauty and cosmetics landscape.

For investors tracking APR Co Ltd earnings, this quarter marks a significant turning point. In this comprehensive analysis, we will break down the key figures, explore the underlying drivers of this stellar performance, and provide a strategic outlook for those considering investing in APR.

Deconstructing the APR Q3 2025 Earnings Surprise

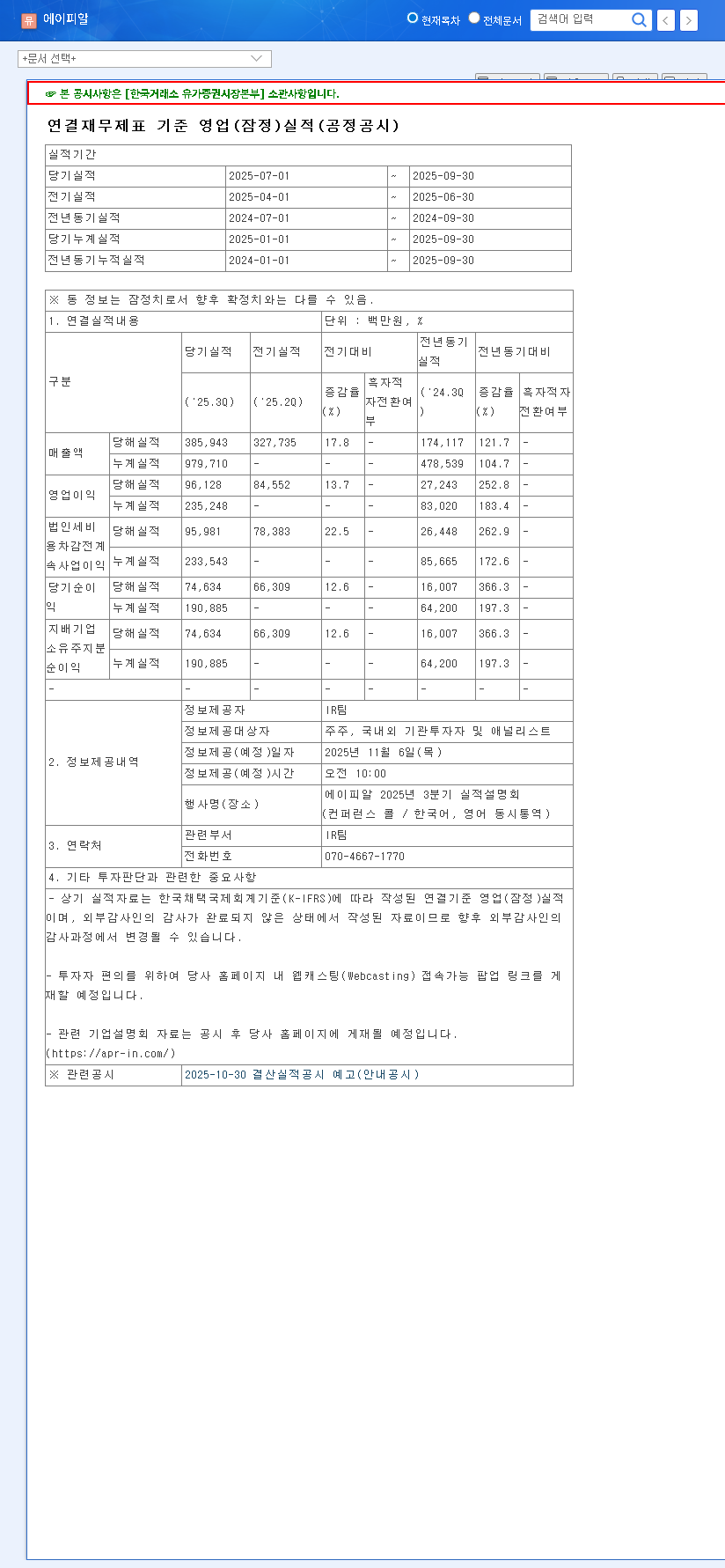

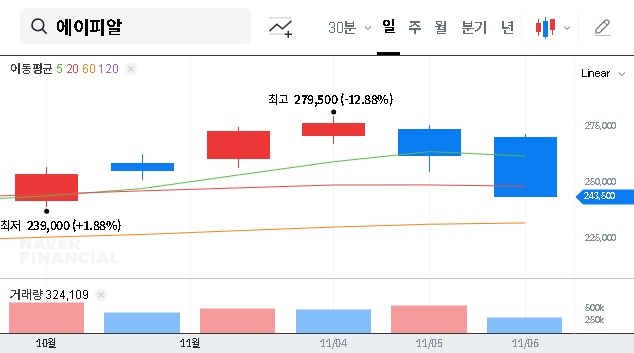

On November 6, 2025, APR Co., Ltd. released its preliminary consolidated financial results, which significantly outperformed market expectations. The positive deviation was not marginal; it was a decisive beat across all key metrics, signaling strong operational execution and market demand. For a complete breakdown, investors can view the Official Disclosure filed with DART.

APR’s Q3 performance demonstrates a powerful rebound, with revenue growing 17.8% quarter-over-quarter and operating profit surpassing forecasts by over 12%. This is a clear indicator of regained momentum.

Key Financial Highlights vs. Forecasts

- •Revenue: KRW 385.9 billion, a +4.5% beat over the KRW 369.3 billion consensus.

- •Operating Profit: KRW 96.1 billion, an impressive +12.1% surprise above the KRW 85.7 billion forecast.

- •Net Income: KRW 74.6 billion, outperforming expectations by +12.4% (vs. KRW 66.4 billion).

This dramatic reversal from the trends seen in our H1 2025 performance review has restored investor confidence. The substantial increase in profitability, with both operating and net profit margins improving, directly counters previous concerns about margin compression.

Core Strengths: The Engine Behind the Growth

This outstanding performance is not a one-time event but the result of APR’s deeply ingrained strategic advantages. The detailed APR financial results showcase the power of its core business segments.

Dominance in Beauty Devices & Cosmetics

The dual engines of APR’s growth—cosmetics and home beauty devices—fired on all cylinders. The beauty device segment, in particular, solidified its market leadership through continuous innovation from its in-house R&D and integrated production facilities. This vertical integration is a critical moat, enabling faster product launches and superior quality control. Simultaneously, the cosmetics division saw remarkable expansion in overseas markets, particularly in North America and Southeast Asia, validating its global appeal and effective marketing strategies.

Financial Fortitude and Shareholder Value

A strong balance sheet underpins this growth. In Q3, APR increased its total equity and generated robust operating cash flow, highlighting efficient capital management. This financial health allows the company to reinvest in growth while also rewarding shareholders. The ongoing share buyback program and interim dividend payments are a testament to management’s commitment to enhancing shareholder value, a crucial part of any long-term 278470 stock analysis.

Investor Outlook & Strategic Action Plan

The APR Q3 2025 earnings surprise is a pivotal event that reshapes both the short-term and long-term investment thesis for the company. Exceeding expectations so decisively is likely to fuel positive stock price momentum as buying sentiment strengthens.

Key Factors to Monitor Moving Forward

While the results are overwhelmingly positive, prudent investors should keep several factors on their radar:

- •Q4 Momentum: Can APR sustain this high level of performance into the final quarter to cap off a strong year?

- •Global Economic Conditions: The impact of macroeconomic factors, such as inflation and consumer spending habits, remains a key variable. High-authority sources like The Wall Street Journal provide essential context on this front.

- •Competitive Landscape: The beauty market is notoriously competitive. Monitoring new entrants and the strategic moves of existing rivals is crucial.

- •Innovation Pipeline: Continued investment in R&D for new beauty devices and cosmetic lines will be the lifeblood of future growth.

In conclusion, APR Co., Ltd. has delivered a powerful statement with its Q3 2025 results. The company has proven its ability to navigate challenges, execute its growth strategy effectively, and generate substantial profits. For investors, this quarter provides a compelling reason to be optimistic about the company’s trajectory and its potential for long-term value creation.