Recent corporate disclosures from Aprogen, Inc. (007460) have sent ripples through the investment community, centering on a significant Aprogen convertible bond sale by a related party. For current and prospective investors, this event raises critical questions: Is this a sign of financial distress, a strategic maneuver, or something else entirely? This comprehensive Aprogen stock analysis will dissect the disclosure, evaluate the company’s underlying fundamentals, and provide a clear, forward-looking investment thesis to navigate the uncertainty surrounding Aprogen’s future.

Deconstructing the Aprogen Convertible Bond Sale

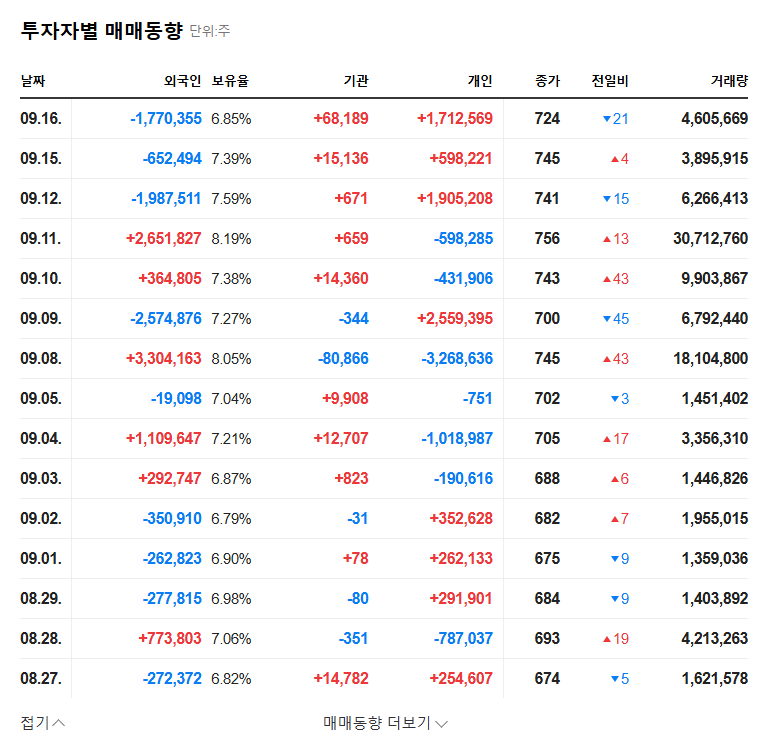

On October 24, 2025, a mandatory disclosure revealed that Aprogen’s majority shareholder, G-Base, saw its stake slightly reduced. This was triggered when a related entity, Apptochrome Co., Ltd., sold 2,597,402 shares of the company’s 27th series of convertible bonds (CBs) in an off-market transaction. A convertible bond is a type of debt security that the holder can convert into a predetermined number of the company’s shares. While the disclosure frames this as a change intended to influence management, the market often interprets such sales as a potential need for liquidity.

The transaction, which had a conversion price of KRW 770 per share, introduces a significant number of potential new shares into the market, a concept known as dilution. For a detailed breakdown, investors can review the Official Disclosure (DART).

Fundamental Analysis: A Company of Contrasts

To understand the implications of the Aprogen convertible bond sale, we must look at the company’s financial health and business structure. Aprogen is a company with two very different core operations, creating a complex risk profile.

Financial Red Flags: Profitability and Debt

Aprogen’s financial statements paint a concerning picture. Despite its pharmaceutical division comprising over half its sales, overall profitability is weak. The biopharmaceutical arm, intended to be the future growth engine, consistently posts significant operating losses. This leads to a troubling reliance on external financing.

- •High Debt Ratio: As of mid-2025, total liabilities surged to approximately KRW 309.5 billion against assets of KRW 808.4 billion. This spike is driven by borrowings and CB issuances, raising serious questions about the company’s financial stability.

- •Cash Flow Concerns: While operating cash flow recently turned positive, this was primarily due to financing activities, not core business profits. A continued dependence on fundraising to stay afloat is a major red flag for investors.

Dual Engines: Stable Metals vs. High-Risk Bio

Aprogen’s business is split between a steady, cash-generating metal division and a high-risk, high-reward biopharmaceutical division. The metal division, specializing in hardfacing with long-term clients like POSCO, provides a stable foundation. In contrast, the biopharma division holds the key to explosive growth through its pipeline of four biosimilars and treatments for brain diseases like Parkinson’s. However, this potential is fraught with peril.

The core challenge for any Aprogen investment thesis is balancing the stability of its legacy business against the immense R&D costs, clinical trial risks, and intense competition facing its biopharmaceutical ambitions.

Stock Impact: Analyzing the Fallout

The recent CB sale is likely to cast a long shadow over Aprogen’s stock price, with negative factors far outweighing any potential positives.

- •Stock Dilution & Overhang: The most direct impact is the threat of share dilution. The 2.5 million shares from the CB sale create a significant ‘overhang,’ meaning there is a large block of shares that could be sold into the market, suppressing the stock price and capping any potential rallies.

- •Negative Market Sentiment: The sale reinforces the market’s perception that the company may be struggling for liquidity to fund its costly R&D pipeline. This perception can deter new investment and encourage existing shareholders to sell. To better understand this financial instrument, you can learn more about convertible bonds from Investopedia.

- •Management Confidence: While the majority shareholder’s stake is still dominant, any sale by insiders or related parties can subtly erode investor confidence in management’s long-term conviction.

Investment Strategy for Aprogen (007460) Stock

Given the significant headwinds, a highly conservative and cautious approach is warranted. Our Aprogen stock analysis suggests segmenting the investment strategy into short-term and long-term outlooks.

Short-Term: Maintain a Defensive Stance

In the short term, the stock price is likely to remain under pressure. It is advisable to adopt a ‘wait-and-see’ approach until the company provides more clarity on its future funding plans and the rationale behind the CB sale. Technical indicators should be monitored closely for signs of further breakdown below recent lows.

Long-Term: Monitoring for Key Catalysts

A long-term investment in Aprogen is a speculative bet on its biopharma pipeline. For those with a high risk tolerance, there are several key catalysts to monitor before considering a position. This approach is similar to what’s outlined in our guide to analyzing biotech stocks.

- •Clinical Trial Progress: Tangible success and regulatory approval for key biosimilars, such as AP063 (a Herceptin biosimilar), would be a game-changer.

- •Financial Improvement: A clear, demonstrated path to improved profitability and a reduction in the company’s high debt ratio is non-negotiable.

- •Macro-Environment Shift: A more favorable interest rate environment could lower the cost of capital and provide some relief, but this should not be the primary investment thesis.

Conclusion: High Risk Overshadows Potential

In conclusion, while Aprogen, Inc. holds long-term potential in its biopharmaceutical ambitions, the company is currently plagued by significant financial weaknesses. The recent Aprogen convertible bond sale exacerbates existing concerns about liquidity, share dilution, and overall financial health. Until there is concrete evidence of a turnaround—marked by clinical success and improved financials—investors are strongly advised to exercise extreme caution. The risks, for now, appear to substantially outweigh the potential rewards.