All eyes are on Doosan Robotics Inc., a prominent leader in the global collaborative robot market, as it approaches its pivotal Q3 2025 Investor Relations (IR) event. This briefing is more than a routine update; it represents a critical juncture for the company. Will this IR serve as the catalyst to overcome recent financial headwinds and solidify its future as an AI-driven powerhouse? Or will it magnify existing concerns about profitability and competition?

This comprehensive analysis offers a deep dive into the upcoming event, dissecting company fundamentals, macroeconomic factors, and the potential impact on Doosan Robotics stock. We will explore how the Q3 earnings and management’s strategic vision will shape investor sentiment and guide you toward more informed robotics investment decisions.

The Stakes of the Q3 2025 IR Event

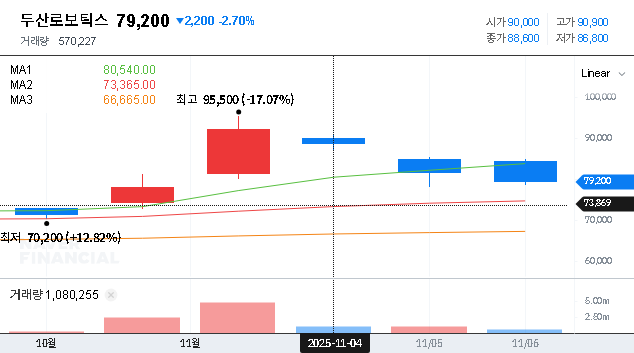

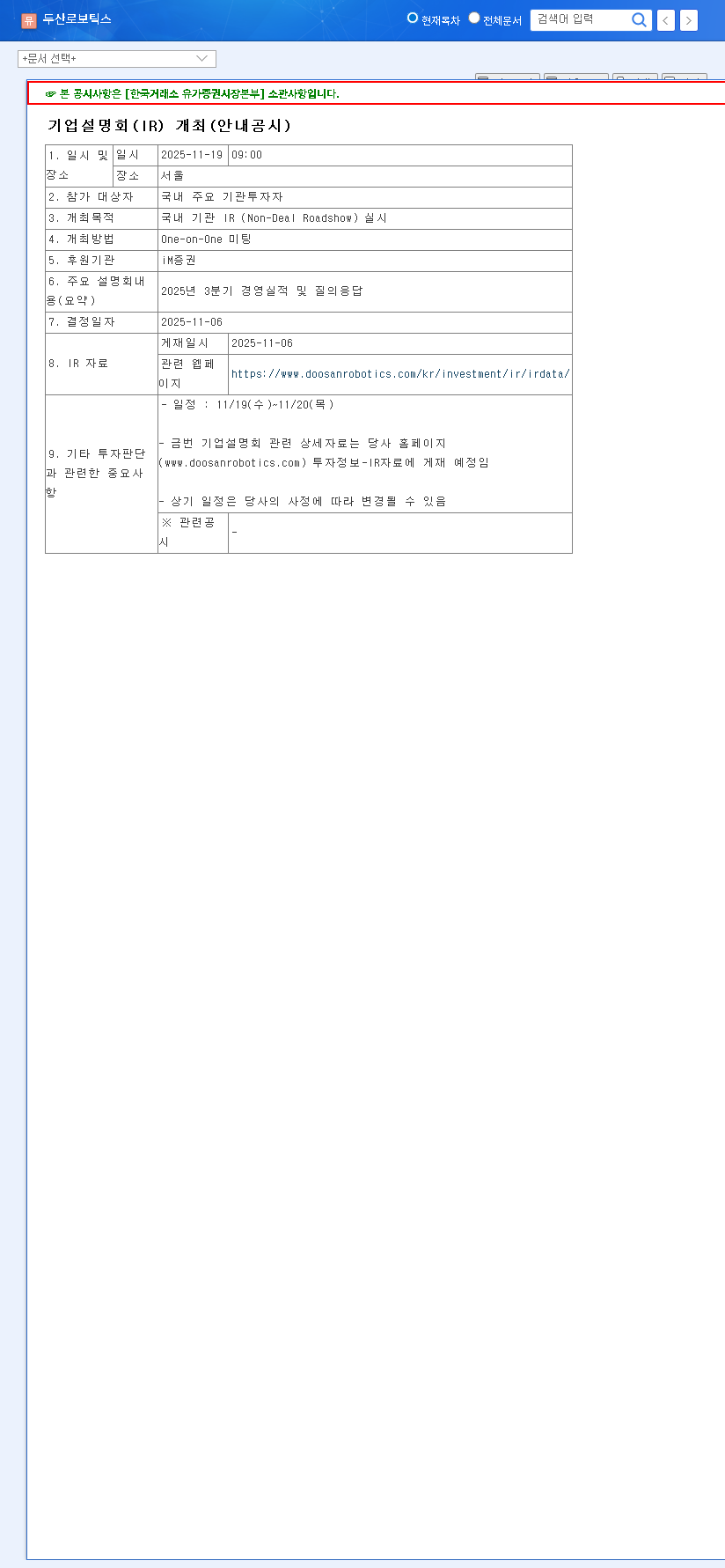

Doosan Robotics Inc. has scheduled its IR briefing for domestic institutional investors on November 19, 2025. This Non-Deal Roadshow will feature the announcement of its Q3 2025 performance results, followed by an essential Q&A session. The primary goal is to transparently communicate the company’s current business health and strategic outlook, as detailed in its Official Disclosure. For investors, this is a key opportunity to gauge the leadership’s confidence and clarity of vision.

Financial Health: A Fundamental Diagnosis

While Doosan Robotics Inc. is strategically positioned in the high-growth collaborative robot market, its recent financial performance presents a mixed picture, highlighting a significant challenge in achieving profitability.

Deteriorating Revenue and Profitability Metrics

The first half of 2025 revealed some concerning trends that investors will be watching closely in the Q3 report:

- •Significant Revenue Decrease: H1 2025 revenue stood at 9.812 billion KRW, a sharp 61.2% decline year-over-year, largely attributed to the global economic slowdown and key customer inventory adjustments.

- •Expanding Operating Losses: The operating loss widened to 27.757 billion KRW in H1 2025. This was driven by the combination of decreased revenue and rising Selling, General, and Administrative (SG&A) expenses.

- •Negative Earnings Per Share: The loss per share of -401 KRW in H1 2025 underscores the profitability challenges the company faces.

A Silver Lining: Financial Soundness

Despite the operational losses, the company’s balance sheet shows a key strength. With a debt-to-equity ratio maintained at an exceptionally low 5.02%, Doosan Robotics Inc. demonstrates robust financial health. This stability is a crucial asset that can support the company through volatile periods and provides a solid foundation for its long-term growth strategy.

The core challenge for Doosan Robotics is clear: it must prove to investors that its exciting AI-driven vision can be translated into a sustainable and profitable business model.

The Future Growth Driver: AI Robotics Strategy

The company’s long-term value proposition hinges on its ambitious AI robotics strategy. Management is steering the company from a hardware-centric model to becoming an AI-based, End-to-End intelligent robot solution provider. This strategic shift is vital for differentiation in a competitive market. However, the absolute decrease in R&D expenditure, a consequence of falling sales, is a point of concern that management will need to address. Strategic investments, like the stake in ONExia, Inc., signal a commitment to this vision, but investors will be looking for a clearer roadmap to monetization.

Market Landscape and Potential Scenarios

The global collaborative robot market is expanding at a remarkable rate, providing a fertile ground for growth. However, competition from established players like Universal Robots and FANUC is intense. Doosan’s price competitiveness and high safety ratings are key advantages, but the market demands continuous innovation.

Positive Scenario (The Bull Case)

- •Q3 earnings beat expectations, signaling a revenue recovery.

- •Management presents a concrete, data-backed roadmap for the AI strategy.

- •A clear plan for controlling SG&A expenses and improving margins is unveiled.

Negative Scenario (The Bear Case)

- •Q3 results show continued revenue decline and widening losses.

- •The AI strategy remains vague without clear milestones or commercialization plans.

- •Concerns about the absolute decline in R&D spending are not adequately addressed.

Actionable Insights for Investors

Investors should look beyond the headline numbers of the Q3 report. The real insights will come from management’s narrative during the Q&A session. Pay close attention to their commentary on profitability improvements, progress in the AI and solution integration, and global market expansion strategies. Understanding the broader trends is also crucial. For context, you can read our detailed analysis of the global robotics industry and compare financial metrics with reports from authoritative sources like the Financial Times.

Ultimately, this IR event will be a defining moment for Doosan Robotics stock. A convincing performance could restore investor confidence and set the stage for a rebound, while a disappointing one could prolong the uncertainty. Diligent analysis of the information presented will be key to making a sound investment decision.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be based on your own research and judgment.