The latest JW LIFESCIENCE Q3 2025 earnings report, released on November 5, 2025, has sent ripples through the investment community. While the company’s foundational strength in the IV solutions market remains solid, the preliminary figures reveal a noticeable downturn in profitability. This analysis unpacks the numbers, explores the underlying causes, and provides a strategic outlook for current and potential investors navigating this complex financial landscape.

We will provide a comprehensive assessment of JW LIFESCIENCE’s performance, its correlation with the broader market, and what these results signal for the company’s future trajectory. For those seeking clarity on the JW LIFESCIENCE stock outlook, this detailed breakdown is essential reading.

Deconstructing the Q3 2025 Preliminary Earnings

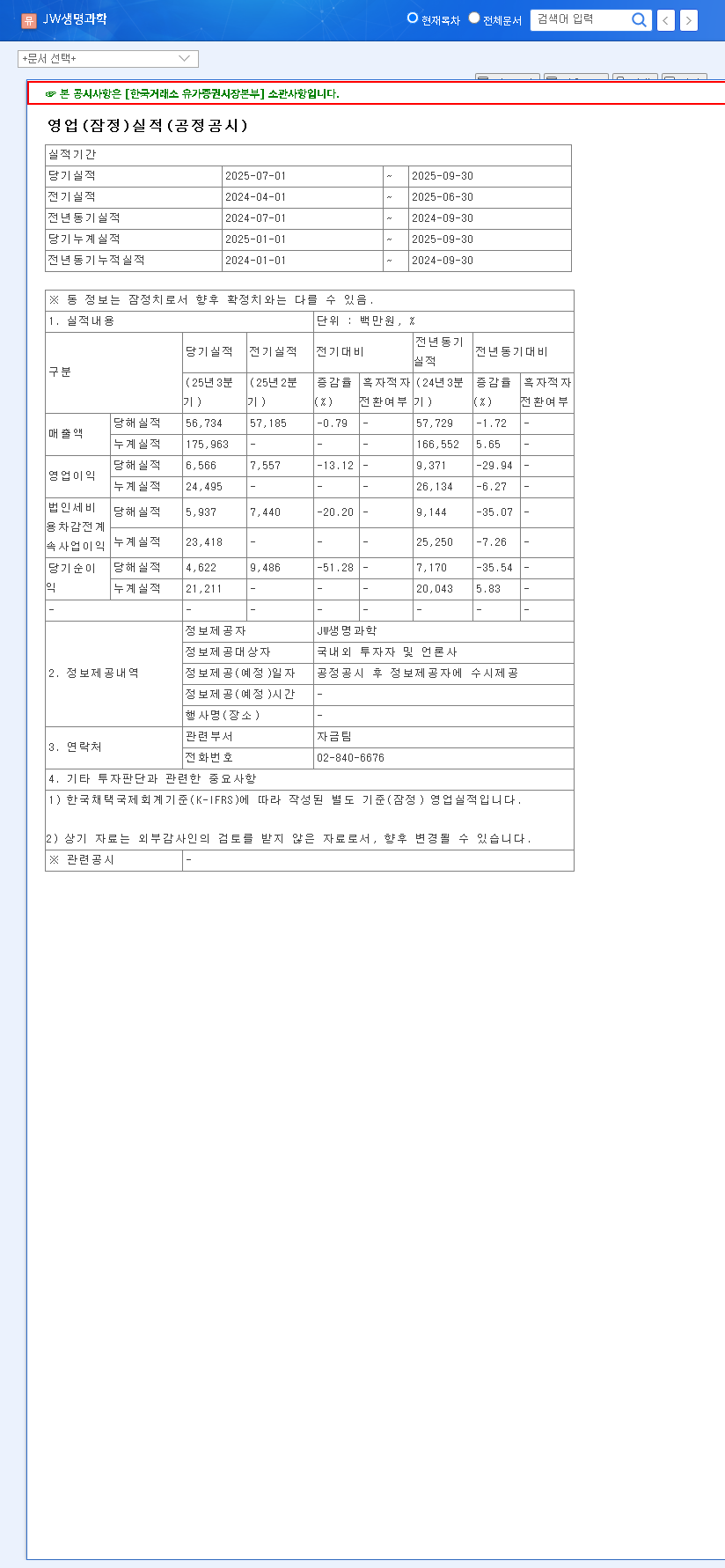

The initial figures from the JW LIFESCIENCE Q3 2025 earnings announcement paint a challenging short-term picture. Here are the key performance indicators disclosed:

- •Revenue: KRW 56.7 billion

- •Operating Profit: KRW 6.6 billion

- •Net Income: KRW 4.6 billion

These numbers represent a clear decline not only from the previous quarter (Q2 2025) but also when compared to the same period last year. This trend points directly to a compression of profit margins and raises critical questions about the operational pressures facing the company.

“While the short-term numbers present a challenge, the underlying strength of JW Lifescience’s core business and its strong financial health should not be overlooked by long-term investors.”

Fundamental Analysis: Why Did Profitability Falter?

Solid Fundamentals vs. Rising Cost Pressures

Despite the Q3 dip, JW LIFESCIENCE’s core business remains robust. The company holds a commanding competitive position in the IV solutions market and has made significant strides in global expansion, notably by securing its EU-GMP certification. Financially, the company’s foundation is sound, with healthy operating cash flow and a low debt-to-equity ratio of 48.9%. This financial prudence is a key asset.

The primary culprits for the Q3 profitability decline are clear: rising Cost of Goods Sold (COGS) and Selling, General & Administrative (SG&A) expenses. The fact that these costs grew at a faster rate than revenue indicates that margin erosion is the central issue. Effective cost management will be paramount for the company’s performance in the coming quarters. For a deeper dive into financial metrics, you can review our guide on how to analyze a biotech company’s statements.

Impact of Macroeconomic Headwinds

No company operates in a vacuum. Broader economic trends are influencing JW LIFESCIENCE’s financial performance. The recent strength of the KRW against the USD could increase the cost of imported raw materials, directly impacting COGS. Conversely, moderating international oil prices may offer some relief. As global financial analysis from sources like Reuters suggests, central bank policies, including the trend toward interest rate cuts, could reduce borrowing costs and stimulate investment.

The company’s stock price, which has seen a gradual decline since mid-2021, reflects these combined pressures. The market is now looking for a clear strategy to counteract these headwinds. For a granular look at the official figures, investors can consult the company’s filing. (Source: Official DART Disclosure)

Investor Action Plan & Strategic Outlook

Recommendation: Neutral (Hold)

Our analysis leads to a ‘Neutral (Hold)’ recommendation. The Q3 results are likely to exert short-term downward pressure on the stock price as the market digests the news of stalled revenue and decreased profits. However, abandoning a position based on one quarter would ignore the company’s strong market position and solid financial health. A ‘wait-and-see’ approach is prudent.

Key Factors to Monitor Moving Forward

- •Official Guidance: Pay close attention to the upcoming finalized Q3 report and the management’s conference call. Look for detailed explanations for the cost increases and a clear, actionable plan for improving profitability.

- •Cost Control Initiatives: Future success hinges on the company’s ability to manage COGS and SG&A expenses effectively. Any announcements regarding supply chain optimization or operational efficiency will be critical.

- •Pipeline and Global Expansion: Monitor for progress on new product development and further penetration into global markets, particularly in Europe, leveraging the EU-GMP certification.

Disclaimer: This analysis is based on publicly available preliminary data. All investment decisions carry risk, and the final responsibility rests with the individual investor. This article is for informational purposes and is not a direct recommendation to buy or sell securities.