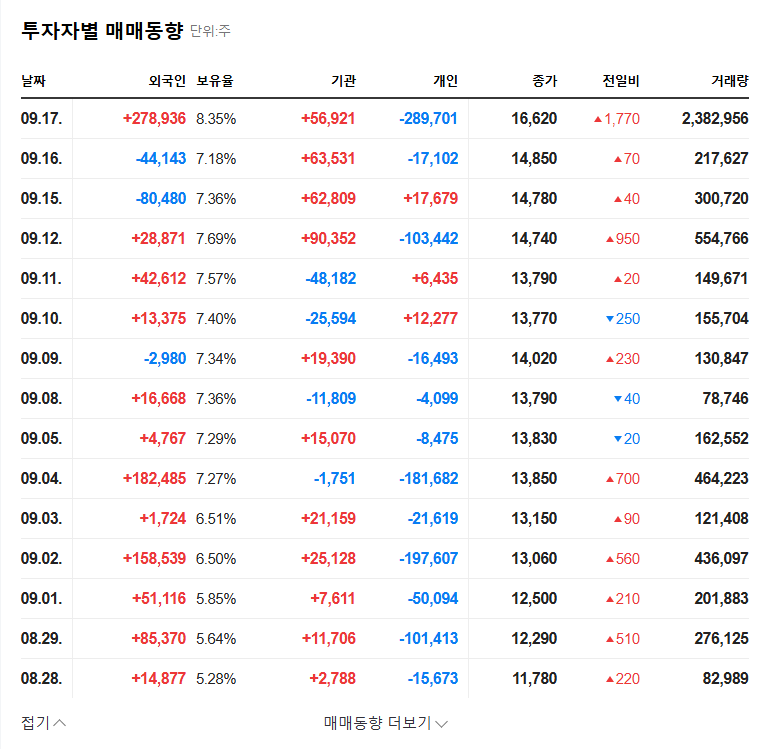

The recent VM Inc. stock option exercise has captured significant attention within the investment community. As a leading semiconductor equipment manufacturer, any corporate action from VM Inc. (브이엠) warrants a closer look, especially when it involves the issuance of new shares. This event, representing 1.23% of its total outstanding shares, comes at a critical time for the company, which is navigating sluggish performance and management uncertainty. This comprehensive guide will dissect the implications of this move, offering a detailed semiconductor stock analysis and outlining crucial strategies for current and potential investors.

For anyone holding or considering an investment in VM Inc. stock (ticker: 089970), understanding the nuances of this development is paramount to making an informed decision.

Breaking Down the VM Inc. Stock Option Exercise

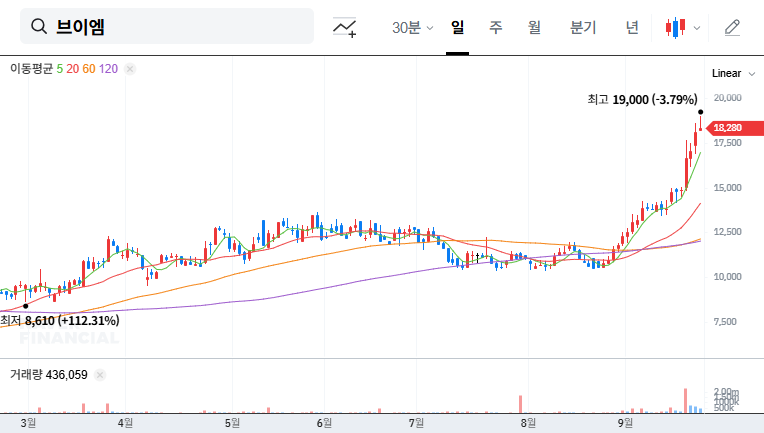

On December 3, 2025, VM Inc. announced the exercise of 320,000 stock options. The details of this corporate action were made public in the company’s Official Disclosure. In essence, a stock option exercise allows employees to purchase company shares at a predetermined, often favorable, price. This common practice serves as a powerful compensation tool, designed to motivate employees by aligning their financial interests with the company’s long-term success. While the number of shares—1.23% of the total—is not massive, its timing and context are what truly matter for investors.

VM Inc. at a Glance: A Company of Contrasts

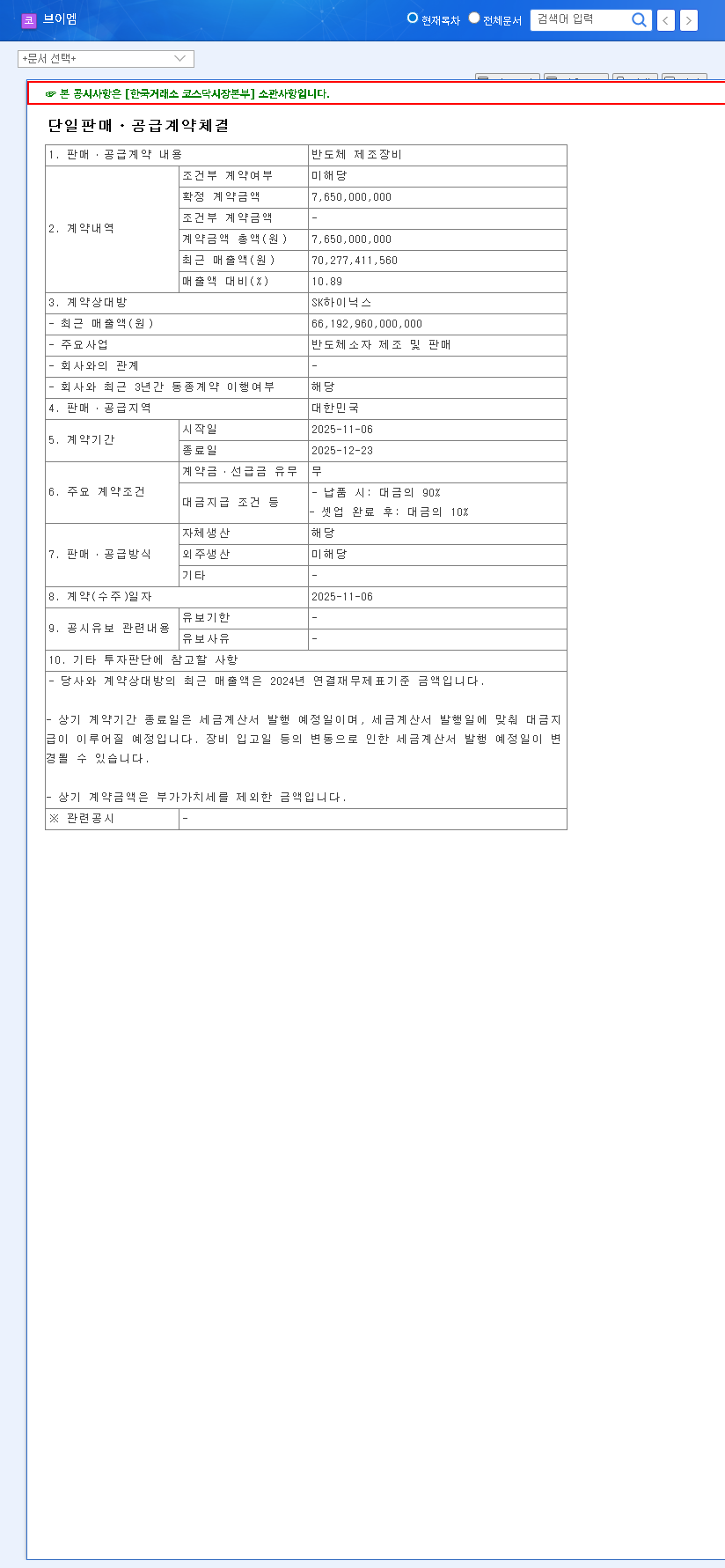

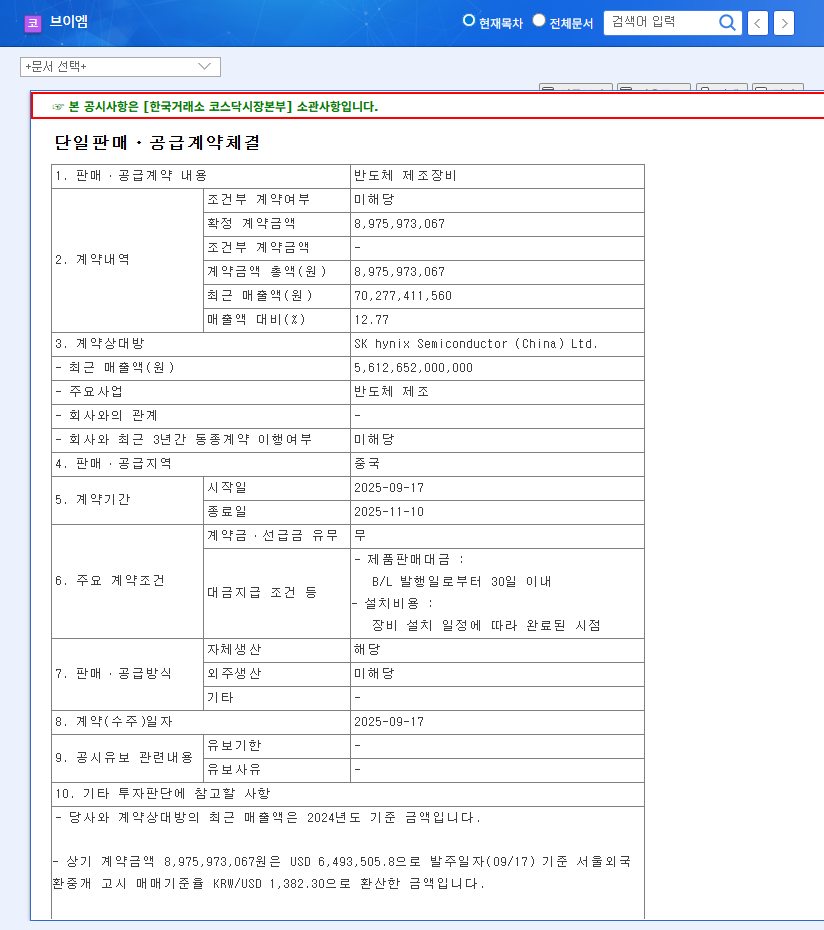

To understand the impact of the stock option event, we must first analyze the company’s current operational and financial landscape. VM Inc. is a key player in the semiconductor ecosystem, specializing in advanced etching process equipment for 300mm wafers, with SK Hynix as a major client.

Financial Fortitude vs. Performance Slump

The company’s recent performance has been challenging. VM Inc. recorded operating losses for two consecutive years (2023, 2024), a direct result of the global semiconductor market downturn and subsequent reduction in capital expenditures by clients. In 2024, it posted an operating loss of KRW 8.6 billion on revenues of KRW 70.3 billion. However, despite these operational headwinds, the company’s financial health remains remarkably stable:

- •A low debt-to-equity ratio of 33.31% signals minimal leverage risk.

- •A strong equity ratio of 75.01% demonstrates a solid balance sheet.

- •Substantial cash reserves of KRW 91.9 billion ensure excellent liquidity to weather the downturn and fund future growth.

This financial stability is crucial, as it allows VM Inc. to continue its significant investment in R&D for next-generation equipment, positioning itself for the inevitable market recovery.

Navigating Macroeconomic Headwinds

The broader economic environment presents further challenges. While emerging technologies like AI and autonomous driving promise long-term demand for semiconductors, the industry remains highly sensitive to macroeconomic shifts. As noted by market analysts at reputable financial news sources, factors like currency volatility (KRW/USD, KRW/EUR) and rising interest rates can significantly impact VM Inc.’s costs and profitability, creating a complex risk profile for investors.

Investor Impact: Reading Between the Lines

The VM Inc. stock option exercise carries both positive and potentially negative signals for the market.

The Bull Case: A Signal of Confidence?

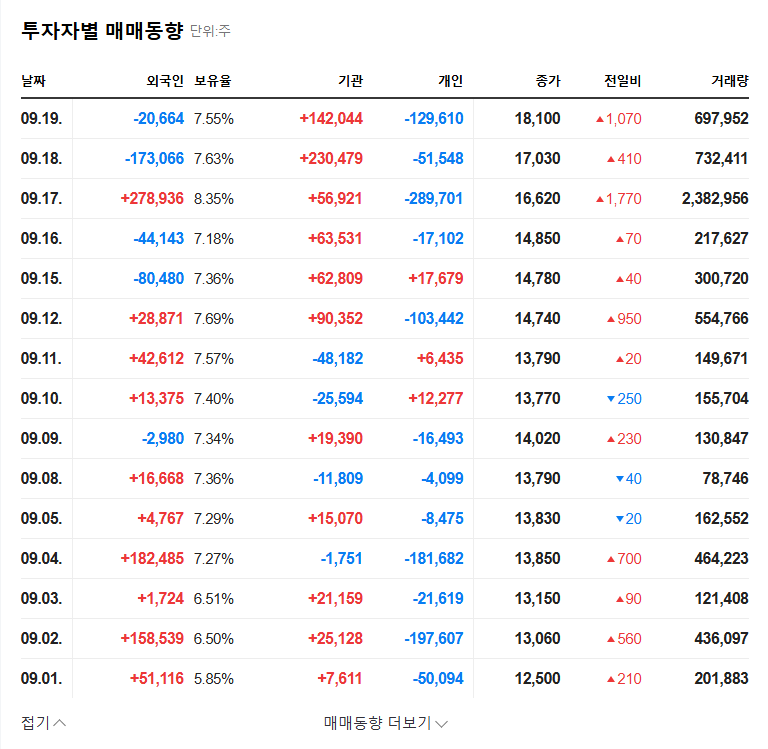

On the positive side, the exercise boosts employee morale and incentivizes performance, which can lead to innovation and operational excellence. It aligns the team’s goals with shareholder value. For the market, it can create short-term positive momentum as it signals a degree of internal confidence and precedes a potential new share issuance.

The Bear Case: A Distraction from Core Issues

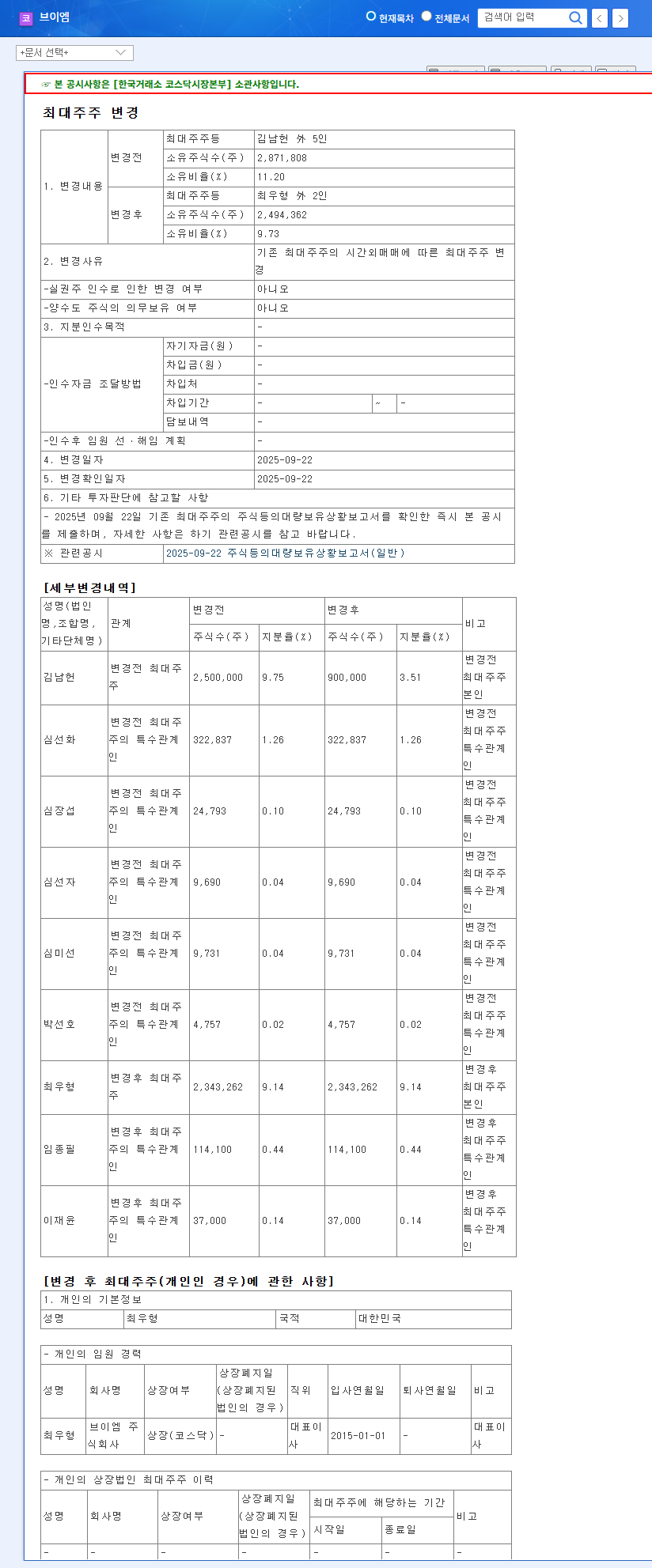

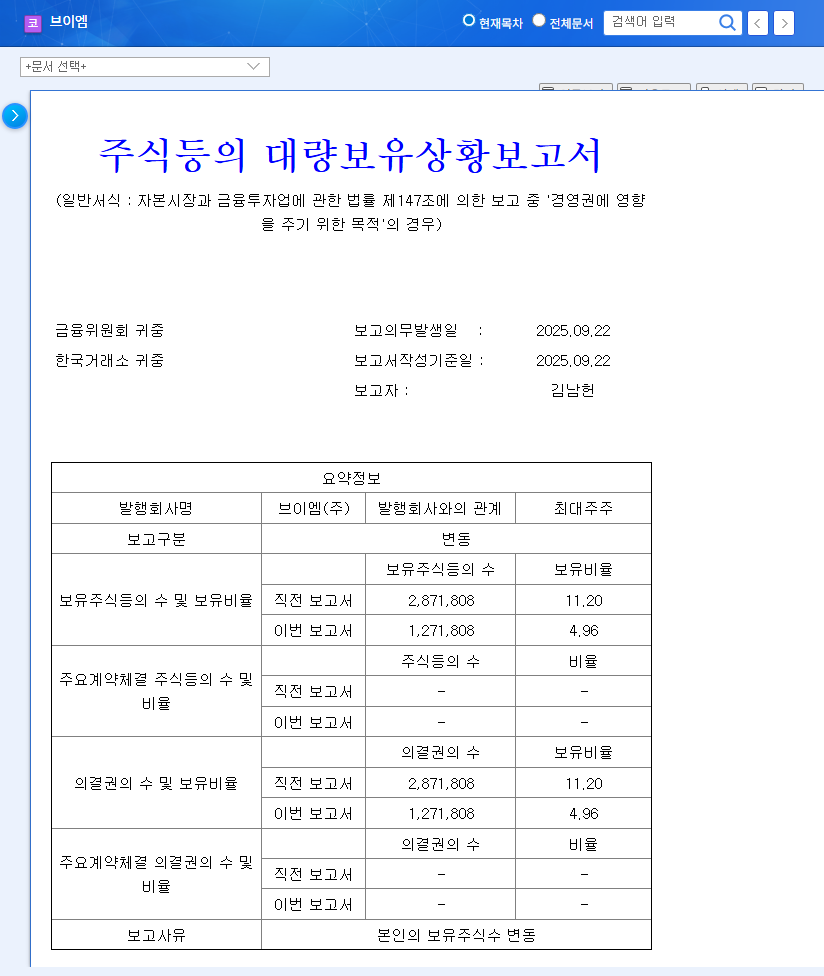

Conversely, the timing is critical. Executing options during a performance slump suggests the primary driver is employee compensation rather than a signal of an imminent turnaround. While the risk of share price dilution from the 1.23% stake is minimal, the event does nothing to solve the company’s fundamental challenges: lackluster profitability and an ongoing management dispute with its largest shareholder. These core issues remain the primary drag on VM Inc. stock.

While the stock option exercise is a notable event, its overall impact is likely limited given the company’s current financial struggles and management uncertainties. Therefore, our investment opinion remains ‘Neutral‘.

Investment Thesis and Action Plan for VM Inc. Stock

This investor guide concludes that a wait-and-see approach is most prudent. The company’s strong technological base and solid financials are compelling, but they are currently overshadowed by significant risks.

Key Catalysts to Monitor:

- •Performance Turnaround: The single most important factor is a return to profitability, driven by the mass production of next-generation equipment. Watch for contract wins and earnings reports.

- •Management Stability: Any resolution or escalation of the dispute with the largest shareholder will have a significant impact on corporate strategy and stock valuation.

- •Semiconductor Market Recovery: Monitor industry-wide capital expenditure trends. For more on this, see our full semiconductor industry outlook.

Ultimately, the VM Inc. stock option exercise is a minor event in the larger narrative. Investors should focus on the fundamental drivers that will determine the company’s long-term value.