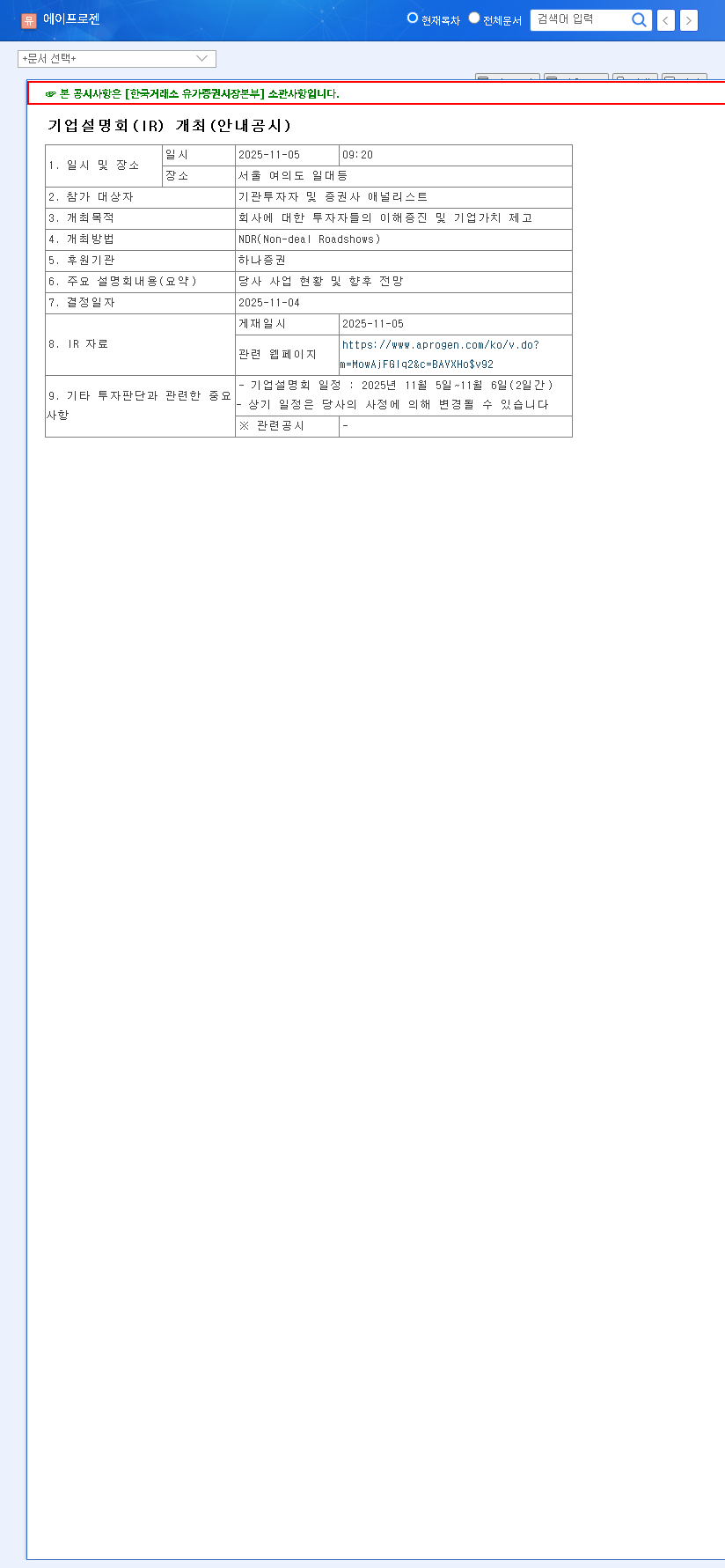

For any potential Aprogen, Inc. investment, November 5, 2025, represents a critical crossroads. The company is poised to host a pivotal Investor Relations (IR) conference, an event that will lay bare its current financial health and ambitious future vision. Investors are watching closely, asking a crucial question: can the revolutionary potential of its biopharmaceutical business finally overshadow the persistent financial risks that have plagued its balance sheet? This comprehensive analysis dissects Aprogen’s complex business landscape, providing the insights necessary for informed decision-making.

We will explore the core tension facing the company—the promise of its high-value biosimilar pipeline versus the reality of its debt burden and underperforming legacy divisions. This deep dive will prepare you for the short-term volatility and long-term implications of the upcoming Aprogen IR.

Aprogen’s Business Segments: A Tale of Two Companies

Understanding an Aprogen, Inc. investment requires a clear-eyed look at its disparate business units. The company operates almost as two separate entities: a collection of legacy industrial businesses and a forward-looking, high-risk, high-reward biopharma division.

Legacy Divisions: Stability Meets Stagnation

- •Metal Business: While holding a near-monopolistic position in its domestic market provides a stable revenue floor, this division has been hampered by a continuous decline in sales.

- •Pharmaceutical Business: The generics segment faces headwinds from government drug price reductions and fierce competition. While the market is growing, Aprogen struggles to compete with top-tier players.

- •Insulation Business: A long 2-3 year revenue cycle makes this division an unreliable contributor to offsetting the sluggish performance of other legacy units in the short term.

The Crown Jewel: The Aprogen Biopharmaceutical Division

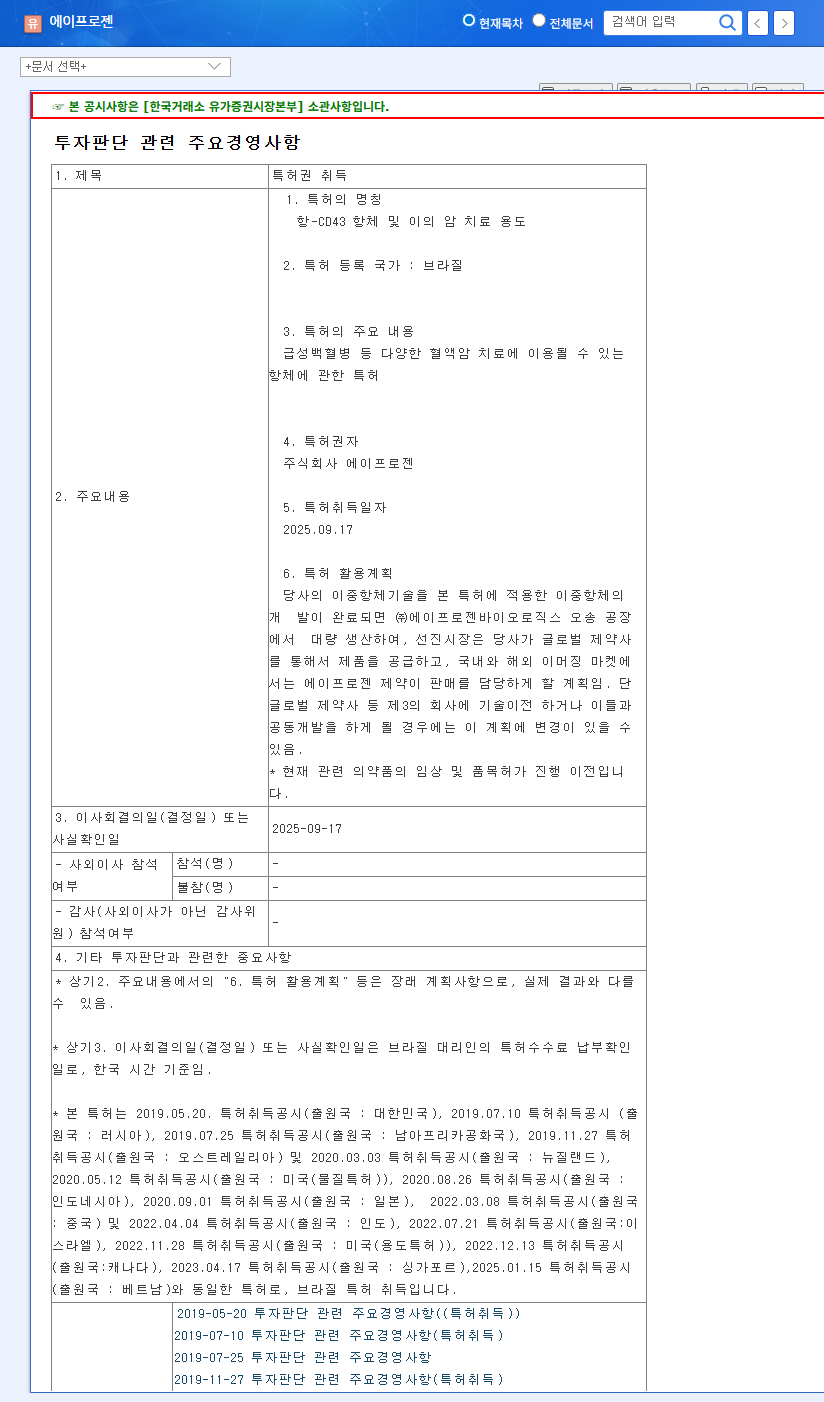

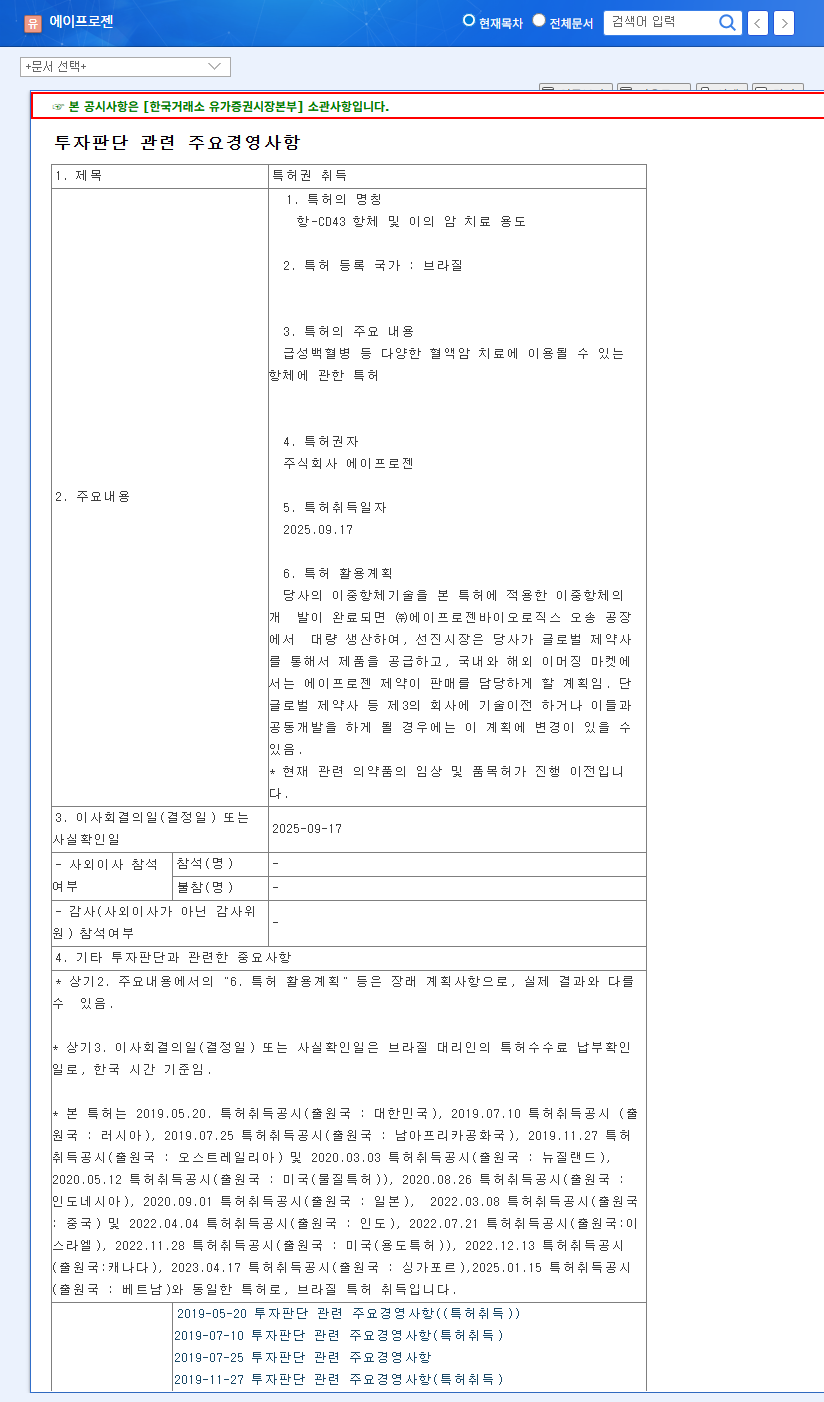

The entire bull case for Aprogen rests on this division. Its pipeline contains potential blockbusters that could redefine the company’s future. The key assets are biosimilars—highly similar, lower-cost versions of approved biologic drugs.

The global biosimilar market is projected to grow exponentially, offering a massive opportunity for companies with approved products. For more on this trend, you can review market analysis from sources like Grand View Research.

Aprogen’s leading candidates, AP063 (Herceptin biosimilar) and AP096 (Humira biosimilar), target multi-billion dollar markets. The company’s Phase 3 waiver strategy for AP063 is particularly noteworthy, as it could significantly accelerate development timelines and reduce costs. However, risks remain, including high R&D expenditures, potential clinical trial failures, and delays in cGMP certification.

Unpacking the Numbers: A Sobering Aprogen Financial Analysis

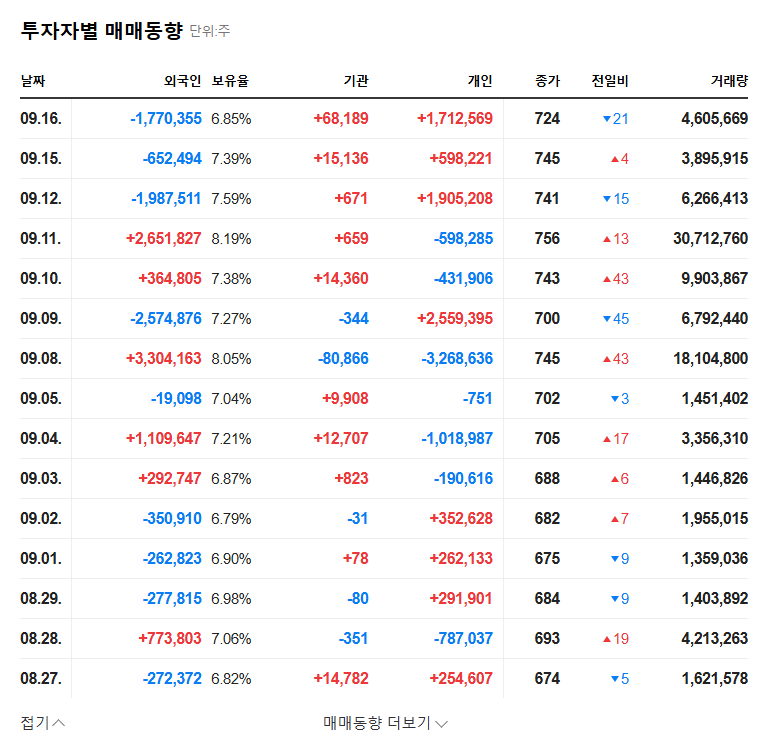

A comprehensive Aprogen financial analysis reveals significant concerns. A deepening retained earnings deficit, coupled with substantial debt from convertible bonds, has created a heavy debt burden. While operating cash flow has recently turned positive, this is undermined by significant cash outflows for investing and financing activities, painting a picture of an unstable cash position. For a detailed breakdown of the company’s financial instruments, investors should consult the Official Disclosure (DART). These financial constraints could impede the company’s ability to fund its promising biopharma pipeline through to commercialization.

IR Scenarios & Stock Impact

The upcoming Aprogen IR could send the Aprogen stock price in dramatically different directions based on the information presented.

Positive Scenario (Short-Term Catalyst)

If management presents concrete, positive updates—such as successful clinical trial data, a confirmed timeline for market entry, or a credible plan to reduce debt—investor sentiment could be significantly boosted, leading to a potential stock price rally. This is the outcome bulls are hoping for.

Negative Scenario (Increased Volatility)

Conversely, if the IR reveals development delays, worsening financial metrics, or a lack of clear strategy, it could trigger a sell-off. Vague answers to tough investor questions could amplify uncertainty and negatively impact the stock price both in the short and long term.

Investor Action Plan: What to Watch For

To make a sound Aprogen, Inc. investment decision, focus on these key areas during the IR event. For further reading on due diligence, consider our guide on how to analyze a biotech company.

- •Biopharma Roadmap: Demand specifics. What are the exact timelines for clinical trials and regulatory submissions? What is the competitive edge of their biosimilars?

- •Financial Health Plan: Look for an actionable, credible plan to manage debt and improve profitability. Vague promises are not enough.

- •Management’s Vision: Does leadership present a clear, confident, and realistic roadmap to navigate the high risks of the bio business and overcome past performance issues?

Ultimately, this IR is a moment of truth for Aprogen, Inc. It will serve as a crucial turning point, hopefully one that enhances transparency and sets the stage for long-term corporate value creation. Investors should be prepared for either outcome.