A startling disclosure from Korean retail giant SHINSEGAE Inc. (004170) has sent shockwaves through the investment community. The announcement of the upcoming SHINSEGAE duty-free business suspension at a key Incheon Airport location has cast a shadow over the company’s future. For investors, this isn’t just a minor setback; it’s a critical event that demands a thorough re-evaluation of the company’s financial health and stock potential. This analysis will dissect the suspension’s details, explore its impact on SHINSEGAE’s already fragile fundamentals, and provide a clear action plan for your portfolio.

The Core Issue: A Multi-Billion Won Suspension at Incheon Airport

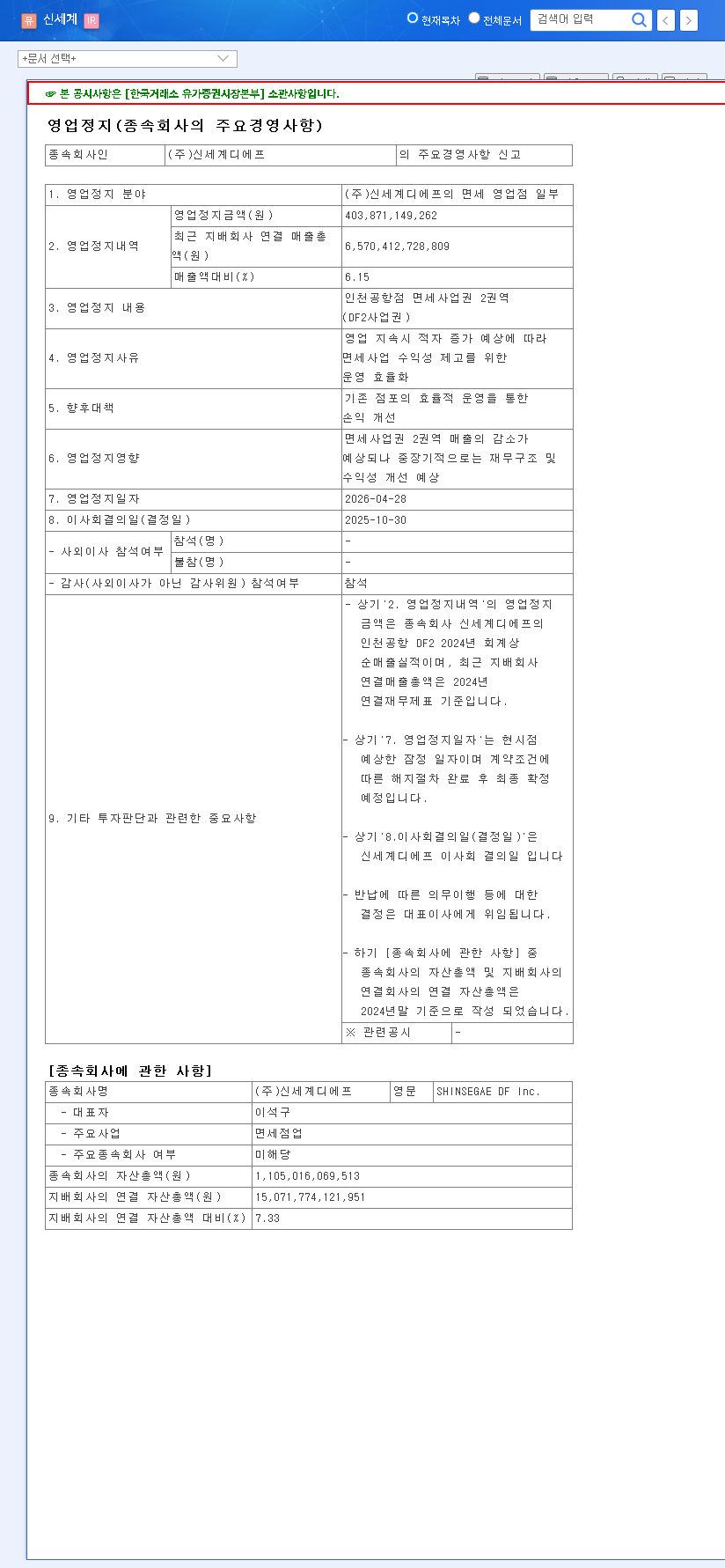

The central issue stems from SHINSEGAE’s subsidiary, SHINSEGAE DF. The company has officially confirmed the business suspension of its duty-free operation in the DF2 concession area of Incheon International Airport, with the suspension set to begin on April 28, 2026. This development was formally recorded in a public disclosure. (Official Disclosure: DART report).

The financial magnitude of this event is staggering. The suspended business accounts for an estimated 403.9 billion KRW, which represents a significant 6.15% of the company’s projected 2025 half-year revenue. This is not a simple operational adjustment but a substantial blow that will directly erode the company’s top and bottom lines, raising serious questions for anyone considering a SHINSEGAE Inc. investment.

Why This Hits So Hard: SHINSEGAE’s Unstable Fundamentals

The timing of this suspension could not be worse. SHINSEGAE was already navigating turbulent waters, with its 2025 half-year report revealing a company under considerable strain. The pre-existing vulnerabilities amplify the negative impact of this news.

Pre-existing Financial Cracks

- •Plummeting Revenue & Profit: Consolidated revenue in H1 2025 dropped by a stark 49% year-over-year, while operating profit fell by 26%. This was driven by severe underperformance in its core department store and duty-free segments.

- •Persistent Duty-Free Losses: The duty-free sector was already a weak link, posting an operating loss of 3.842 billion KRW in the first half of 2025, highlighting an inability to recover in the post-pandemic market.

- •Adverse Market Conditions: High interest rates, persistent inflation, and recessionary fears have suppressed consumer spending. A rising KRW/USD exchange rate adds cost pressure, while fierce online competition continues to challenge SHINSEGAE’s traditional retail models. For more on market volatility, sources like Reuters offer global economic insights.

Ripple Effects: The Full Impact on SHINSEGAE’s Future

The Incheon Airport duty-free business suspension is poised to create a cascade of negative consequences that will affect every aspect of SHINSEGAE’s operations and valuation.

- •Direct Financial Hit: The loss of over 400 billion KRW in revenue from a traditionally high-margin segment will severely compress the group’s overall operating profit.

- •Weakened Market Position: Losing a prime location at a major international hub like Incheon deals a significant blow to SHINSEGAE’s brand presence and competitiveness in the fierce duty-free market.

- •Growth Plans in Jeopardy: The financial strain may force the company to reconsider its planned 665.2 billion KRW investments for 2025, potentially stalling innovation and future growth engines. For a deeper look, see our complete analysis of the Korean retail sector.

- •Damaged Investor Confidence: This event serves as a major red flag, likely to drive down the stock price as investor sentiment sours. The long-term damage to brand trust could be substantial.

Given the compounding negative factors—worsening profitability, structural industry challenges, and weakened financial health—the current investment recommendation for SHINSEGAE Inc. (004170) is a ‘Sell’ or ‘Significant Portfolio Weight Reduction.’

Investor FAQ: Your Key Questions Answered

What is the SHINSEGAE duty-free business suspension?

SHINSEGAE Duty Free is suspending operations at its Incheon Airport DF2 concession area starting April 28, 2026. This move impacts 403.9 billion KRW in revenue, or 6.15% of its estimated annual total.

How bad was SHINSEGAE’s performance before this?

As of H1 2025, SHINSEGAE was already struggling. Consolidated revenue and operating profit had fallen by 49% and 26% year-over-year, respectively. The duty-free sector was already operating at a loss.

What should investors watch for going forward?

Monitor the company’s efforts to improve efficiency in its remaining stores, any government support for the industry, SHINSEGAE’s restructuring plans, and key macroeconomic indicators like exchange rates and consumer sentiment. For now, a cautious, risk-off approach is strongly advised for any SHINSEGAE stock outlook.

Leave a Reply