The recent announcement regarding the YOUNGPOONG Seokpo Smelter has sent ripples through the investment community. For anyone holding or considering shares in YOUNGPOONG CORPORATION (영풍), the 10-day suspension of operations is a critical development. This is not merely a logistical pause; it’s a significant event with a projected revenue disruption of nearly 1 trillion Korean Won, striking at the heart of the company’s financial stability. This comprehensive analysis will dissect the situation, evaluate the impact on YOUNGPOONG’s stock and fundamentals, and provide a clear action plan for investors navigating this uncertainty.

We will move beyond the headlines to offer a deep, data-driven perspective on what this operations halt means for both the short-term stock price and the long-term viability of one of Korea’s major industrial players.

The Core Issue: A Staggering Production Halt

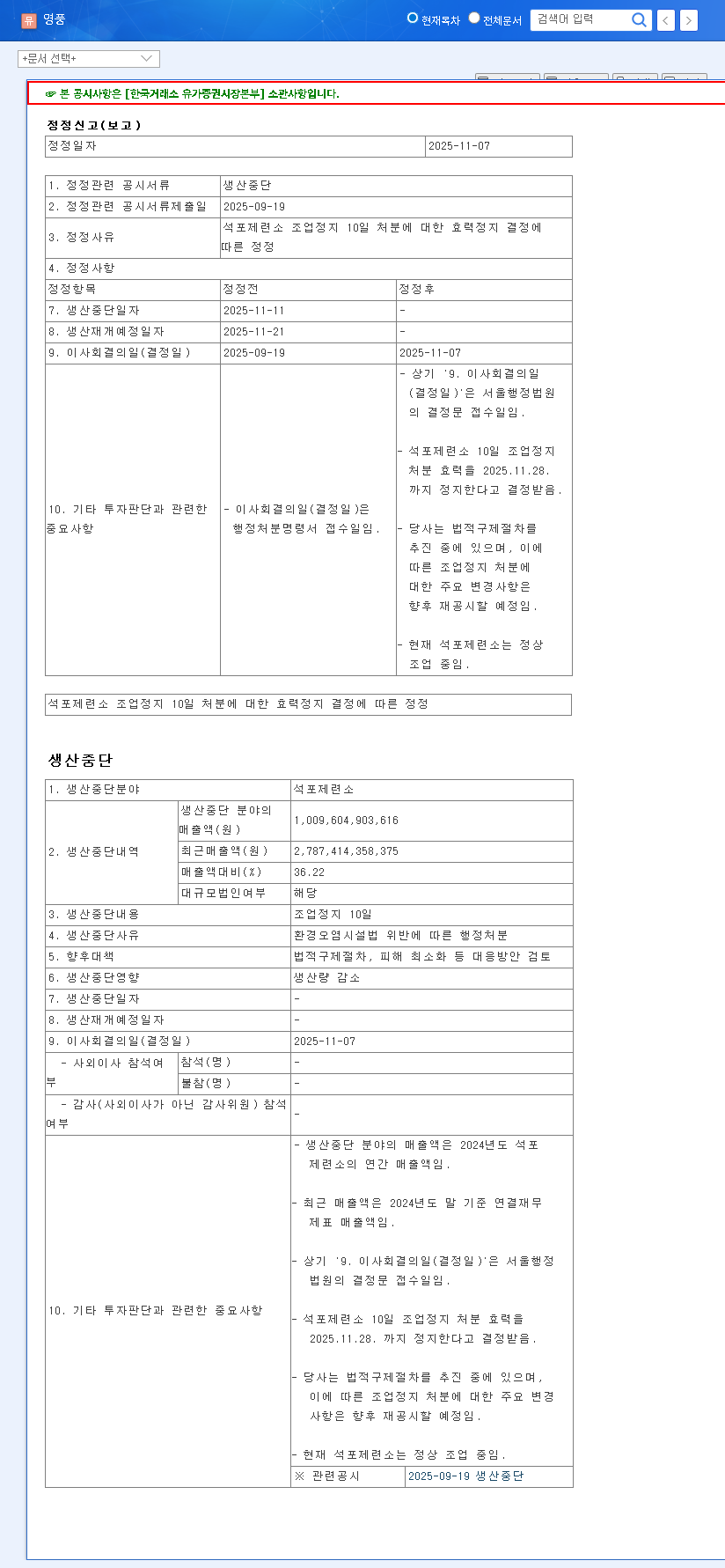

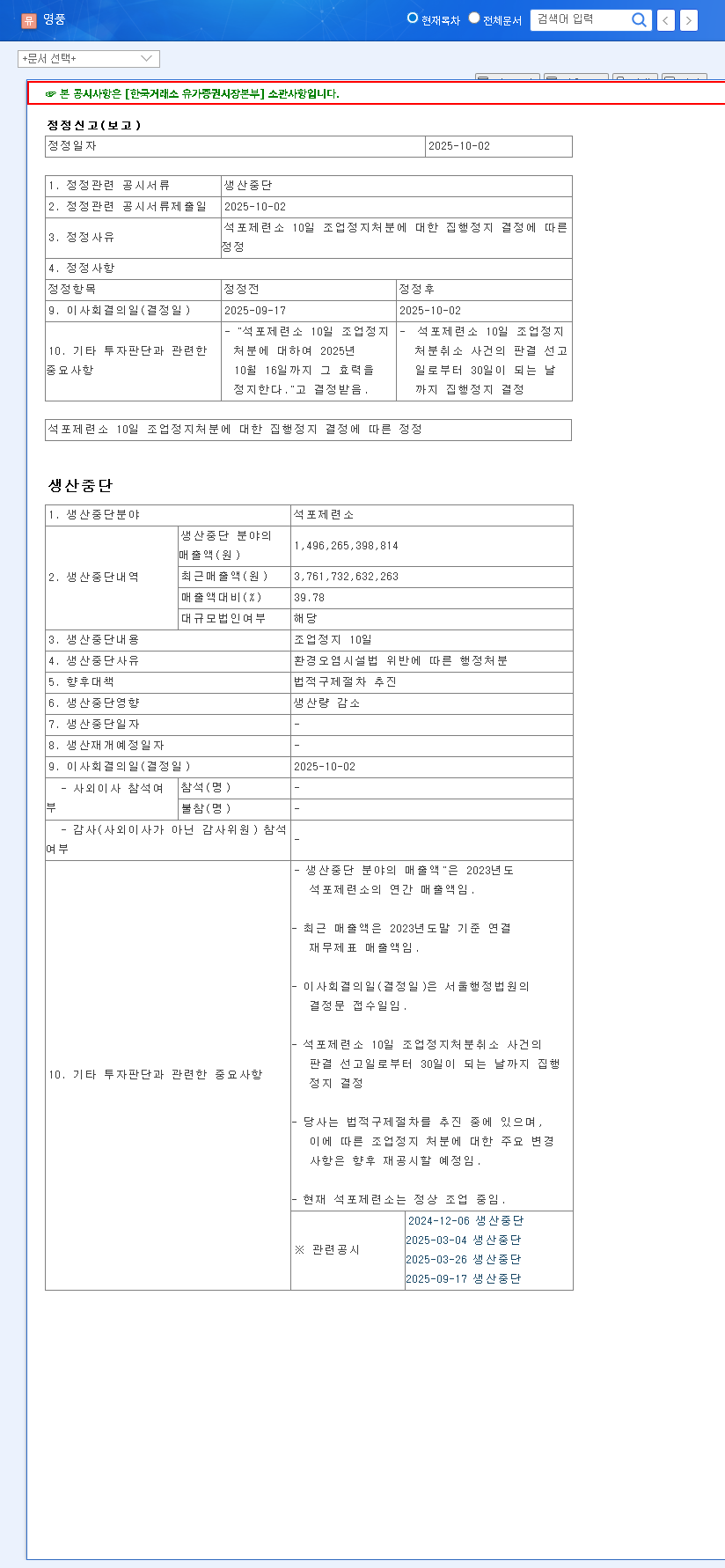

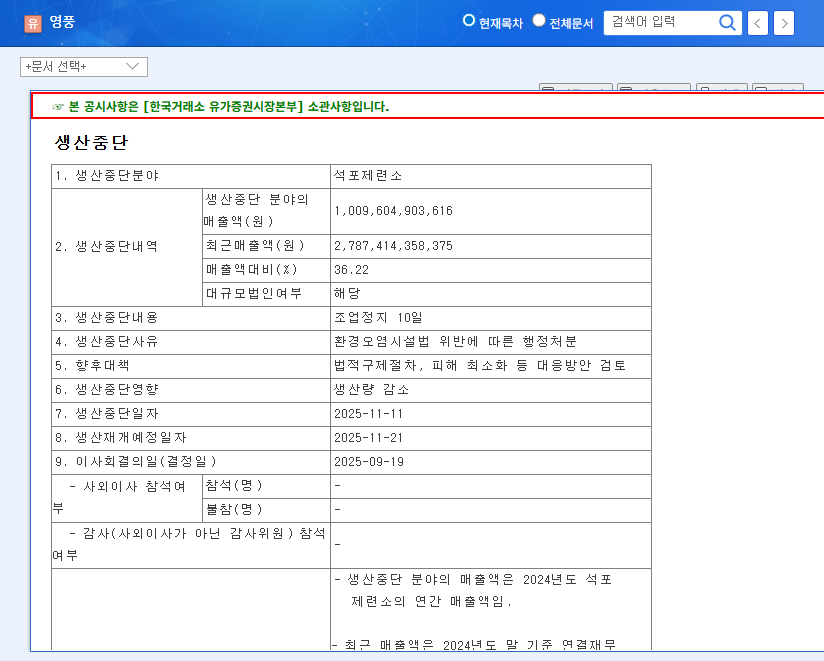

On November 7, 2025, YOUNGPOONG CORPORATION formally announced a 10-day suspension of all production at its core Seokpo Smelter facility. According to the company’s public filing, this halt is projected to slash revenues by an estimated ₩1,009.6 billion. To put this in perspective, this figure represents a massive 36.22% of the company’s total revenue from the previous reporting period. The direct and severe impact on the company’s top line cannot be overstated. Investors can view the Official Disclosure (DART) for primary source information.

This is a pivotal moment for YOUNGPOONG. While the company has other thriving divisions, the sheer scale of the Seokpo Smelter’s revenue contribution makes this operational halt a significant threat to its immediate financial performance and investor confidence.

Dissecting YOUNGPOONG’s Financial Health (Pre-Incident Analysis)

To understand the true impact of this shutdown, we must first have a clear picture of YOUNGPOONG’s fundamentals based on its 2025 H1 report. The company presents a mixed but intriguing financial landscape.

Key Financial Metrics

- •Revenue Decline: Consolidated revenue stood at ₩1.17 trillion, a notable decrease year-on-year, primarily dragged down by poor performance in the smelting division.

- •Operating Loss: An operating loss of ₩150.48 billion was recorded, a slight improvement but still indicative of significant operational challenges and rising environmental compliance costs.

- •Net Profit Turnaround: Surprisingly, the company posted a net profit of ₩264.27 billion, driven by returns from financial instruments and equity investments, not core operations.

- •Strong Financial Health: The debt-to-equity ratio improved to a very healthy 31.38%, suggesting a solid balance sheet that can weather short-term storms.

Performance by Business Division

YOUNGPOONG is not a monolith. Its diversified business model is a key factor in this analysis.

- •Smelting Division: This division has been the primary concern. Even with a 4% rise in international zinc prices, the production utilization rate was a dismal 34.94% due to ongoing operational issues. The current halt will drive this figure even lower.

- •Electronic Components: The star performer, this division recorded revenue of ₩871.2 billion, showcasing robust growth and technological leadership with exports making up over 64% of its sales.

- •Semiconductor Division: Led by its subsidiary Signetics, this segment is a growing force, with revenues of ₩51.59 billion and strong potential.

The Financial Impact of the YOUNGPOONG Seokpo Smelter Shutdown

The 10-day operations halt will have immediate and severe negative consequences on YOUNGPOONG’s fundamentals. The loss of over a third of its revenue in a short period will directly translate into a sharp decline in Q4 performance, likely wiping out any gains and deepening the operating loss. This creates a cascade of potential issues:

- •Profitability Crisis: The smelting division’s woes will be significantly amplified, making it nearly impossible for the profitable electronics and semiconductor divisions to offset the losses.

- •Cash Flow Strain: While the company’s strong balance sheet provides a cushion, a sudden revenue stop of this magnitude will strain short-term cash flow and could impact planned capital expenditures.

- •Reputational and Regulatory Risk: This halt, likely linked to the company’s history of environmental issues and pending lawsuits, damages corporate credibility. It signals deeper operational problems that could lead to further regulatory scrutiny and fines, as noted by market analysts at sources like Bloomberg.

Strategic Outlook and Investor Action Plan

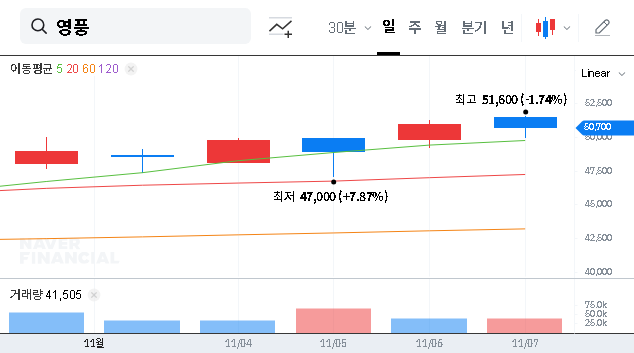

The short-term outlook is undoubtedly negative. The market is likely to price in the revenue loss, leading to downward pressure on YOUNGPOONG’s stock. However, savvy investors should look at the mid-to-long-term picture.

Key Questions for the Future

The company’s recovery hinges on several factors:

- •Speed of Resolution: How quickly can management resolve the underlying cause and resume operations safely and in full compliance?

- •Growth of Other Divisions: Can the high-performing electronics and semiconductor divisions continue their growth trajectory to eventually lessen the reliance on the volatile smelting business? For more on this, see our Analysis of Korea’s Tech Sector.

- •Commitment to ESG: Will this crisis force a genuine, long-term investment in environmental, social, and governance (ESG) standards to prevent future incidents?

Recommendations for Investors

For Current Shareholders: Avoid panic selling. The company’s strong balance sheet provides a safety net. Monitor company communications closely for clarity on the resumption of operations and plans to address the root cause.

For Potential Investors: This situation may present a long-term value opportunity if the stock price overcorrects. However, entry should only be considered after the company provides a transparent and credible plan for stabilizing the Seokpo Smelter and strengthening its environmental compliance. The performance of the non-smelting divisions remains a significant long-term bull case.

In conclusion, the YOUNGPOONG Seokpo Smelter operations halt is a major setback that will dominate the company’s performance in the coming months. The key to its future value lies in management’s ability to turn this crisis into a catalyst for fundamental operational and environmental reform.