The latest SG CORPORATION (004060) Q3 2025 preliminary earnings report presents a complex picture for investors. While a notable rebound in sales suggests a potential recovery, the persistence of operating losses raises critical questions about the company’s fundamental health and long-term strategy. This comprehensive analysis will unpack the results, explore the underlying causes, and provide a clear outlook for anyone evaluating an investment in SG CORPORATION stock.

SG CORPORATION Q3 2025 Earnings at a Glance

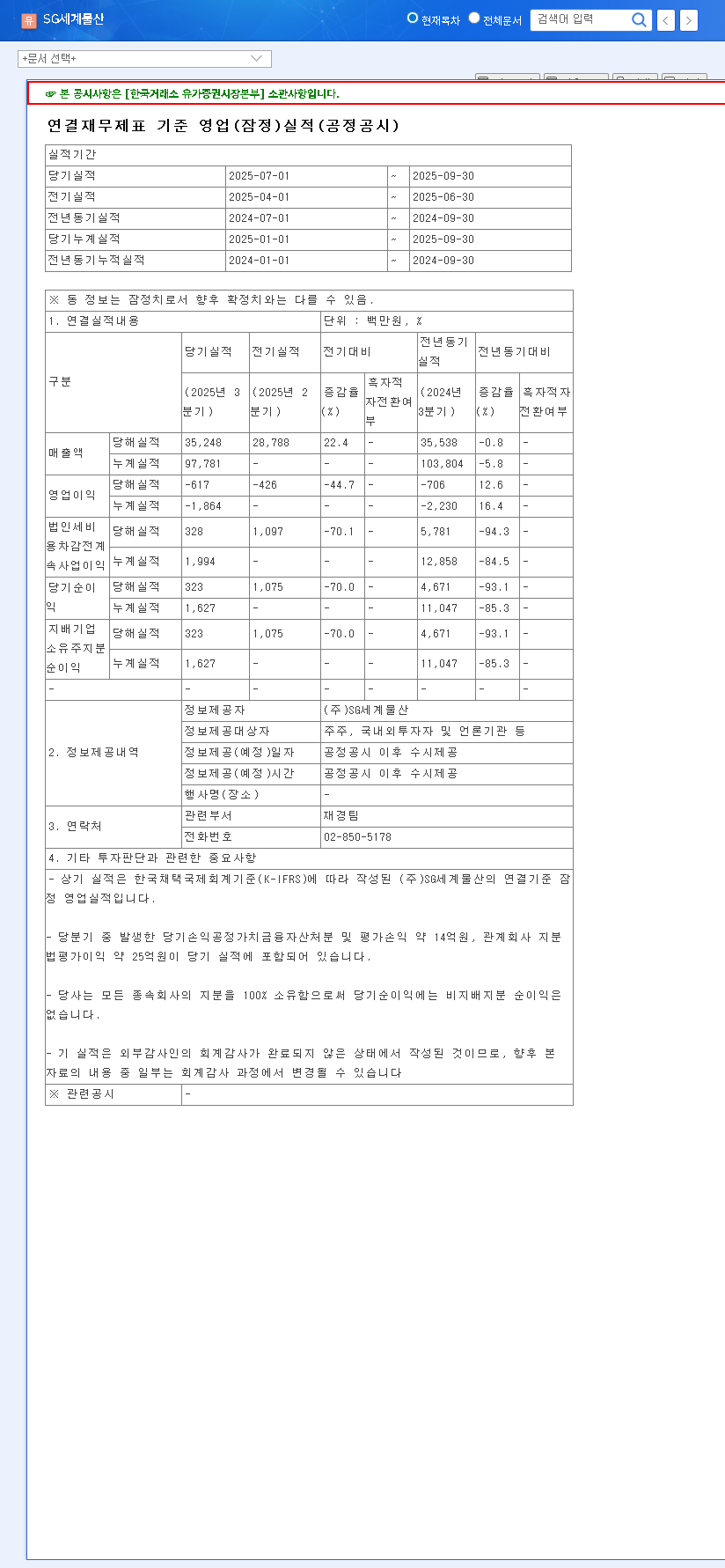

On November 7, 2025, SG CORPORATION released its preliminary operating results for the third quarter. The headline figures, detailed in the Official Disclosure on DART, show a mix of progress and continued challenges:

- •Revenue: KRW 35.2 billion, marking a significant 22.2% increase from the previous quarter, though still down a marginal 0.8% from the prior year period.

- •Operating Profit: A loss of KRW 0.6 billion. This represents a wider loss compared to the previous quarter’s -KRW 0.4 billion, although it is a slight improvement from the same period last year.

- •Net Income: KRW 0.3 billion. This figure is a sharp decrease from both the previous quarter and, more alarmingly, from the KRW 4.7 billion recorded in the same period last year.

The quarter-over-quarter revenue growth is a positive signal, largely driven by the company’s stable export business. However, the inability to translate this into operating profit and the steep decline in net income are major red flags that demand a closer look at the company’s core operations.

The Tale of Two Segments: Analyzing SG CORPORATION’s Core Business

The performance of SG CORPORATION can be understood as a battle between its two primary divisions. The latest results highlight a growing divergence that is central to the company’s current financial state.

Apparel Export: The Steady Engine

The apparel export segment continues to be the bedrock of the company’s revenue. Through stable Original Equipment Manufacturer (OEM) supply contracts, this division has maintained steady growth. This reliability is the primary reason for the overall quarterly revenue increase, demonstrating resilience even amidst global economic uncertainties.

Fashion Segment: The Persistent Drag

In stark contrast, the domestic fashion segment remains a significant drain on profitability. Intense competition, shifting consumer preferences towards fast fashion, and a general decline in consumer sentiment have led to a continued slump in this division. This underperformance is the main driver behind the company’s operating losses, effectively negating the positive contributions from the export business.

The core issue for SG CORPORATION is clear: while the export business provides a stable foundation, the unprofitable fashion segment is eroding the company’s bottom line. A strategic turnaround in this area is not just desirable—it’s imperative for survival and growth.

External Factors: Macroeconomic Headwinds and Tailwinds

Beyond internal operations, global macroeconomic trends are exerting both positive and negative pressures on the company. Investors should be aware of these external variables, which are often tracked by major outlets like Bloomberg.

Positive Catalysts

- •Favorable Exchange Rates (KRW/EUR): A stable, high KRW/EUR exchange rate positively impacts the profitability of exports to Europe.

- •Monetary Easing: A potential easing of monetary policy in the U.S. and South Korea could reduce borrowing costs and financial pressure.

- •Lower Input Costs: Falling crude oil prices may lead to reduced raw material costs, while a decline in freight indices signals easing logistics burdens.

Negative Risks

- •Unfavorable Exchange Rates (KRW/USD): A general downward trend in the KRW/USD rate can negatively affect export competitiveness to the US market.

- •Rising Logistics Costs: Despite some easing, certain indices like the Baltic Dirty Tanker Index show rising trends, indicating persistent upward pressure on shipping costs.

Outlook and Investor Takeaways for SG CORPORATION

Given the mixed signals, a prudent and patient approach is required. The short-term impact of these results is likely neutral, as they confirm existing market concerns. The long-term trajectory of SG CORPORATION stock, however, depends entirely on the management’s ability to execute a successful turnaround. Investors should keep a close watch on the following key areas:

- •Fashion Segment Strategy: What concrete steps will be taken to innovate, rebrand, and regain market share? Are there plans for new brand launches or significant restructuring?

- •Cost Management: Are the increases in SG&A expenses, particularly R&D, strategic investments for future growth or signs of inefficiency? Look for evidence of disciplined cost controls.

- •Export Growth Sustainability: Can the stable apparel export segment continue its growth trajectory and expand its client base? This is critical for maintaining the company’s revenue floor. For more on this, see our analysis of the Korean apparel export market.

Conclusion: A Time for Caution

The SG CORPORATION Q3 2025 earnings report highlights a company at a crossroads. While the revenue recovery is a welcome sign, the persistent operating losses driven by a struggling fashion division limit the stock’s immediate appeal. A hasty investment based on these preliminary results would be unwise. Instead, investors should adopt a ‘watch and wait’ strategy, meticulously monitoring for tangible proof of a strategic turnaround in the fashion segment and improved cost discipline before committing capital.

Leave a Reply