This comprehensive COWAY earnings analysis provides a detailed look into the company’s preliminary financial results for the third quarter of 2025. For investors tracking COWAY Co., Ltd. (021240), the latest report presents a mixed but fascinating picture. While the home appliance rental giant showcased resilient top-line growth, underlying cost pressures impacted its net profitability. This deep dive will dissect the numbers, explore the key drivers behind the performance, and provide a clear outlook on what this means for the COWAY stock analysis and your investment strategy.

COWAY Q3 2025 Earnings: The Official Numbers

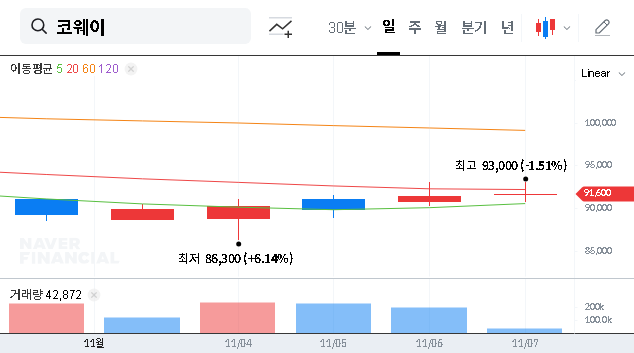

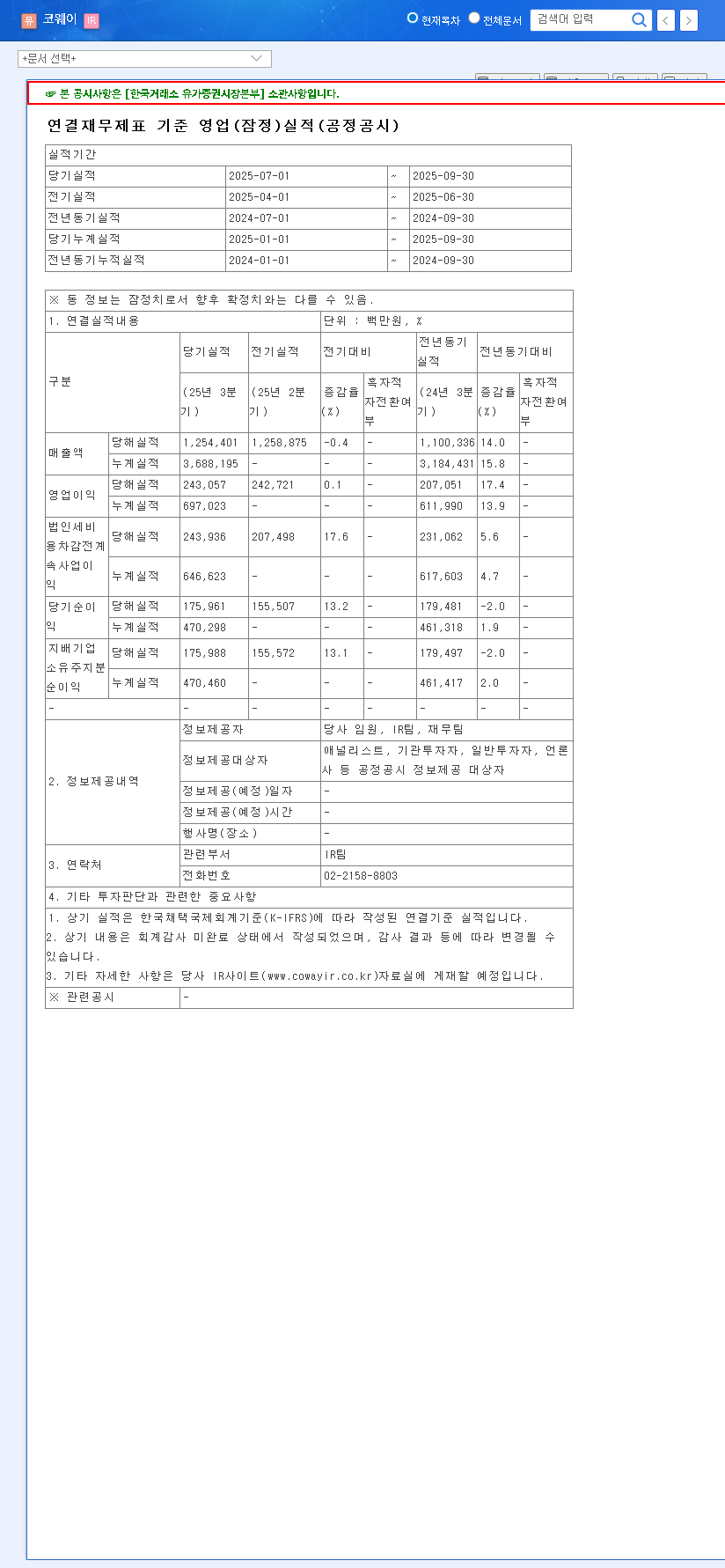

On November 7, 2025, COWAY released its preliminary Q3 earnings, which immediately captured the market’s attention. The company managed to outperform expectations on revenue and operating profit, but a miss on net profit has raised important questions about operational efficiency. The official figures can be reviewed in the Official Disclosure on DART.

Here is a summary of the key performance indicators from the 021240 earnings report:

- •Revenue: KRW 1,254.4 billion, a 1.0% beat against the market consensus of KRW 1,244.1 billion.

- •Operating Profit: KRW 243.1 billion, a 2.2% beat against the market consensus of KRW 237.9 billion.

- •Net Profit: KRW 176.0 billion, a significant 4.9% miss compared to the market expectation of KRW 185.2 billion.

While revenue and operating profit grew slightly year-over-year, the decline in net profit signals that rising costs are beginning to weigh on the bottom line. This dynamic—strong sales but weakening profitability—is the central theme of the COWAY Q3 2025 earnings report.

Deep Dive: Analyzing COWAY’s Financial Health

To truly understand these results, we must look beyond the headline numbers and examine the fundamental drivers and pressures shaping COWAY’s performance.

The Unwavering Strength of the Rental Business

COWAY’s core strength remains its dominant rental business model. Accounting for over 90% of total sales, the recurring revenue from its massive installed base of environmental home appliances provides a highly stable and predictable income stream. This foundation allows the company to weather economic uncertainties better than competitors who rely on one-off sales. The continued expansion of its domestic and international rental accounts is a testament to the brand’s power and the sustained demand for its products.

Despite macroeconomic headwinds, COWAY’s rental segment continues to be a fortress of stability, fueling its top-line growth and cementing its market leadership. However, the key challenge moving forward will be translating this revenue strength into proportional profit growth.

Decoding the Profitability Squeeze

The primary culprit behind the net profit miss is a noticeable increase in selling, general, and administrative (SG&A) expenses. This includes higher commission fees and sales-related costs. This spending surge could be a strategic investment in growth—such as entering new overseas markets or aggressive marketing campaigns to fend off rising competition—but it directly impacts profitability. For a detailed overview of market dynamics, investors often consult resources like Bloomberg’s market analysis. The market will be watching closely to see if this increased spending translates into sustainable, long-term market share gains.

Financial Stability and Cash Flow Concerns

From a balance sheet perspective, COWAY remains on solid ground. Its debt-to-equity and current ratios are within healthy ranges, indicating strong financial soundness. However, a significant point of concern is the sharp year-over-year decrease in operating cash flow, which turned negative this quarter. Management attributes this to temporary factors related to investment and financing activities. While potentially a one-off event, investors should monitor cash flow trends in subsequent quarters to ensure it’s not a sign of underlying operational issues. Understanding financial ratios is key, and our guide to investor metrics can help.

Stock Outlook: What’s Next for COWAY (021240)?

The mixed results from the COWAY Q3 2025 earnings report create a nuanced outlook for its stock price.

- •Short-Term Momentum: The positive surprise in revenue and operating profit may provide a short-term lift. However, the net profit miss could act as a ceiling, limiting significant upward movement until the company demonstrates better cost control.

- •Mid-to-Long-Term Potential: The long-term investment thesis remains intact. COWAY’s robust business model, international expansion strategy, and commitment to ESG and R&D are powerful drivers for future value creation. The key variables will be its ability to manage SG&A expenses and navigate currency fluctuations effectively.

Investor FAQs: COWAY Q3 2025 Earnings

Q1: Did COWAY’s Q3 2025 earnings meet expectations?

A1: It was a mixed result. Revenue (KRW 1,254.4B) and operating profit (KRW 243.1B) beat market expectations, demonstrating solid growth. However, net profit (KRW 176.0B) fell short of estimates, indicating cost pressures.

Q2: What was the main reason for COWAY’s net profit decline?

A2: The decline is primarily attributed to an increase in selling and administrative (SG&A) expenses, including higher commission fees and sales commissions, which squeezed profit margins.

Q3: What is the mid-to-long-term investment outlook for COWAY?

A3: The outlook remains positive, supported by its stable rental business and overseas growth. However, successful management of rising operational costs and currency risks will be critical for future stock performance. Investors should monitor profitability trends closely.

Leave a Reply