The recent announcement of the WITHTECH SK Hynix contract, a substantial KRW 3.9 billion deal, has sent ripples through the semiconductor industry and caught the attention of keen investors. As the demand for advanced semiconductors skyrockets, the technology that underpins their flawless production—specifically, manufacturing environment monitoring—becomes mission-critical. This deal not only represents a significant revenue injection for WITHTECH, Inc. but also serves as a powerful endorsement of its technological leadership.

This comprehensive analysis unpacks the details of this pivotal agreement, examines WITHTECH’s current financial health, and provides a forward-looking perspective for potential investors. We will explore whether this contract is the catalyst for a new era of growth or if underlying financial concerns warrant a more cautious approach to WITHTECH stock.

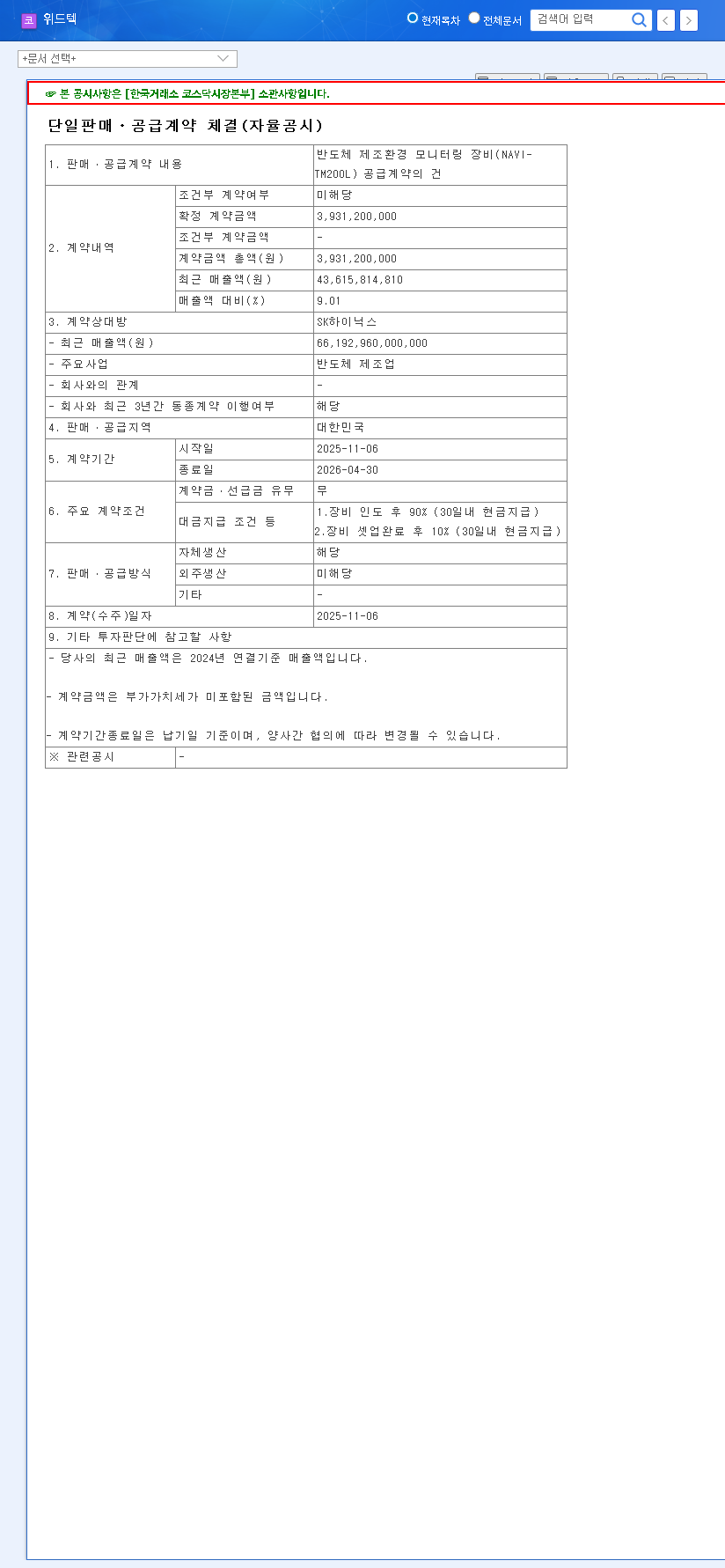

Deconstructing the WITHTECH SK Hynix Contract

On November 7, 2025, WITHTECH, Inc. formally disclosed a major agreement with SK Hynix, a global leader in memory semiconductors. The deal involves the supply of its advanced semiconductor monitoring equipment, specifically the NAVI-TM200L model. Here are the core details:

- •Contract Value: KRW 3.9 billion.

- •Financial Impact: This figure represents a significant 20.3% of WITHTECH’s revenue from its 23rd semi-annual period.

- •Contract Period: November 6, 2025, to April 30, 2026.

- •Source: The details of this agreement are publicly available in the Official Disclosure on DART.

This isn’t just a simple equipment sale. The NAVI-TM200L system is crucial for monitoring and controlling molecular-level contaminants in real-time within fabrication plants (fabs). As chip architecture shrinks to the nanometer scale, even the slightest impurity can render an entire wafer useless, making this technology indispensable for maximizing yield and profitability.

Why This Deal is a Game-Changer for WITHTECH

1. Validating Technological Supremacy

Securing a contract of this magnitude from a tier-one manufacturer like SK Hynix is the ultimate validation. It proves that WITHTECH’s technology meets the incredibly stringent standards required for cutting-edge memory production, such as HBM for AI applications. This credibility can be leveraged to attract new clients and solidify its market position against competitors.

2. Immediate and Future Revenue Growth

The immediate KRW 3.9 billion boost is set to significantly impact WITHTECH’s top-line growth. More importantly, it deepens the company’s integration into the SK Hynix supply chain. As SK Hynix continues to expand its production capacity to meet AI-driven demand, WITHTECH is now perfectly positioned to win subsequent, potentially larger, orders. This is a critical step in building a long-term, predictable revenue stream. For a deeper understanding of industry trends, explore insights from authoritative sources like Gartner’s semiconductor forecast.

This contract is more than a financial transaction; it’s a strategic partnership that anchors WITHTECH’s technology at the heart of the global AI revolution, driven by industry leaders like SK Hynix.

WITHTECH Investment Analysis: A Look at the Fundamentals

While the SK Hynix deal is unequivocally positive, a prudent WITHTECH investment decision requires a balanced view of the company’s underlying financial health.

Strengths to Consider

- •Premier Client Roster: Long-standing relationships with titans like Samsung Electronics and SK Hynix provide a stable business foundation.

- •Favorable Market Tailwinds: The entire semiconductor industry is moving towards more complex processes, increasing the need for sophisticated contamination monitoring.

- •Financial Stability: The company maintains a low debt-to-equity ratio, indicating a healthy balance sheet and reduced financial risk.

Concerns Requiring Monitoring

Despite growing revenue, profitability has become a challenge. The 23rd semi-annual report revealed a consolidated operating loss of KRW 0.59 billion and a net loss of KRW 2.1 billion. This was driven by rising costs in sales, administration, and crucial R&D. Furthermore, operating cash flow was negative at KRW -5.017 billion, signaling that the company spent more cash than it generated from its core operations during the period. Investors must watch to see if the profitability of the WITHTECH SK Hynix contract can help reverse this trend. To learn more, you can read our guide on understanding cash flow statements.

Future Outlook and Investor Action Plan

The SK Hynix contract is a powerful catalyst for WITHTECH. It provides a clear pathway to revenue growth and enhances its industry standing. However, the long-term success of WITHTECH stock hinges on the company’s ability to translate this top-line momentum into bottom-line profitability.

Investors should keep a close watch on the following key metrics in upcoming quarterly reports:

- •Profit Margins: Will the new contract carry a high enough margin to improve overall profitability?

- •Operating Cash Flow: Can the company convert its new sales into positive cash flow?

- •Cost Management: Are there clear strategies in place to control rising SG&A and other operational expenses?

In conclusion, the WITHTECH SK Hynix contract is a significant and promising development that reaffirms the company’s growth potential. For investors, it signals a major opportunity, but one that must be balanced with diligent monitoring of the company’s progress toward sustainable profitability.

Leave a Reply