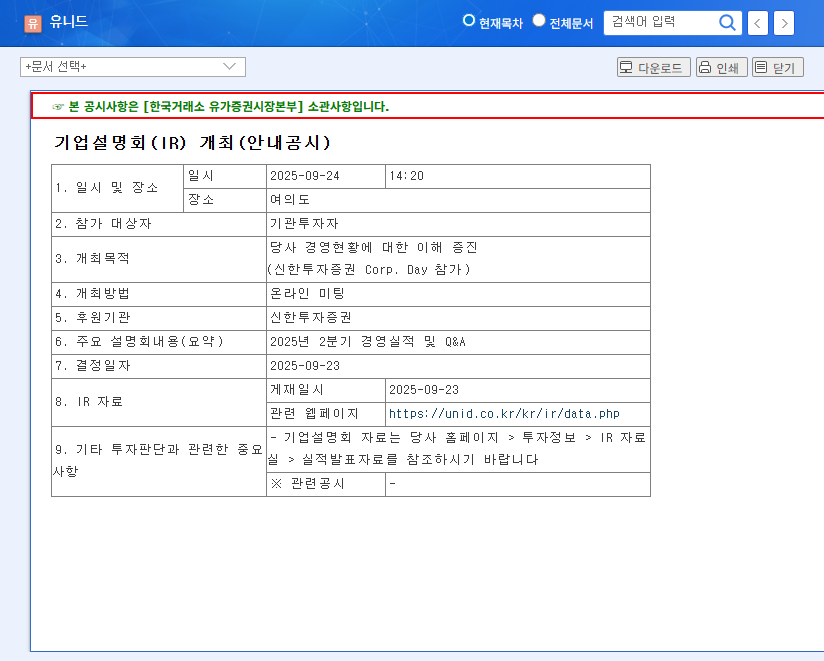

The upcoming UNID IR Briefing for its Q3 2025 performance is a pivotal moment for investors. Scheduled for October 28, 2025, at 9:00 AM, this event for UNID CO.,LTD (014830) is more than a standard earnings call; it’s a critical look into the chemical giant’s future. While top-line growth has been impressive, looming concerns over profitability and market pressures have created a high-stakes environment. This analysis will provide a deep dive into what to expect from the UNID Q3 2025 earnings report, the key risks at play, and how the outcomes could significantly impact the company’s stock valuation.

Investors are keenly watching to see if the momentum from overseas business can be sustained and, more importantly, if management can present a convincing strategy to address margin compression. This report offers a comprehensive UNID stock analysis ahead of this crucial briefing.

A Look Back: UNID’s H1 2025 Performance Review

To understand the context of the Q3 briefing, it’s essential to analyze UNID’s performance in the first half of 2025. The results painted a dual picture of robust growth and emerging challenges.

Strong Revenue Growth Driven by Overseas Operations

UNID reported consolidated revenue of 663.4 billion KRW for H1 2025, marking a significant 21% increase year-over-year. This impressive top-line expansion was primarily fueled by the strong production and sales of caustic potash and related chemical products from its major subsidiaries in China. The successful operation of new facilities has been a key contributor, demonstrating the company’s ability to scale its international footprint.

The Elephant in the Room: Profitability Concerns

Despite the revenue surge, operating profit saw a slight year-over-year decrease to 61.4 billion KRW. This has understandably raised concerns about a profitability slowdown. The primary causes are multifaceted: falling international prices for key products like caustic potash, stubbornly firm prices for raw materials such as potassium chloride (KCl), and intensifying market competition within China. This margin pressure is a central theme that the UNID IR Briefing must address head-on.

A Pillar of Strength: Solid Financial Health

On a positive note, UNID’s financial foundation remains remarkably stable. Key metrics like the debt-to-equity ratio (31.37%) and net debt-to-equity ratio (12.41%) both improved from the previous year. This sound financial health provides a crucial buffer, especially in a global environment of rising interest rates, giving the company flexibility to navigate market turbulence. To learn more, you can read our analysis of the broader chemical sector.

Investors will be listening for more than just numbers; they need a convincing strategy that addresses margin compression and outlines a clear path to sustainable growth through innovation and effective risk management.

Navigating Headwinds: Key Risks to Watch

Several external and internal challenges face UNID, and the company’s strategies to mitigate these risks will be a major focus of the investor Q&A session.

- •Exchange Rate Volatility: With a significant portion of assets and liabilities in foreign currencies, UNID is exposed to fluctuations in exchange rates (particularly KRW/USD and KRW/CNY), which can impact earnings unpredictably.

- •Raw Material Pressures: The firm international price of KCl and potential production cuts in key supplier nations pose a direct threat to production costs. A clear supply chain strategy is vital, especially with global commodity markets remaining tight, as reported by outlets like Bloomberg.

- •Intensified Competition: The emergence of new competitors and the expansion of production capacity in the crucial Chinese market threaten to erode UNID’s cost competitiveness and market share.

- •Low R&D Investment: A relatively low R&D expenditure (0.04% of sales) is a long-term concern. Investors will look for a clearer commitment to innovation to secure new growth engines beyond existing products.

Investment Strategy & Stock Price Scenarios

The upcoming UNID IR Briefing could act as a significant catalyst for the stock price. The direction will depend heavily on the content and tone of the presentation.

Positive Scenario (Bull Case)

If Q3 earnings meet or exceed market expectations and management provides clear, actionable strategies for improving profitability, managing currency risk, and investing in future growth, investor confidence could surge. This enhanced transparency could lead to a positive stock re-rating.

Negative Scenario (Bear Case)

Conversely, if Q3 earnings miss expectations or the company fails to provide convincing answers to the profitability and risk factor questions, investor sentiment could sour. A lack of clarity could amplify existing concerns, potentially leading to downward pressure on the stock price.

Ultimately, investors should maintain a long-term perspective. While short-term volatility is likely post-briefing, the most prudent approach is to base decisions on the company’s fundamental strength and the credibility of its strategic vision. For complete transparency, the company’s official filing is a crucial resource. You can find the Official Disclosure here. This report is based on available information, and investment decisions should be made with careful consideration and individual judgment.

Leave a Reply