The latest SAMSUNG HEAVY INDUSTRIES Q3 2025 Earnings report, released on October 23, 2025, has sent a mixed but intriguing signal to the market. While the shipbuilding giant showcased a formidable operating profit that significantly outpaced expectations, a concurrent dip in net income has left investors seeking clarity. This comprehensive analysis will break down the numbers, explore the underlying factors driving this performance, and provide a strategic outlook for both short-term traders and long-term stakeholders.

Can Samsung Heavy Industries (SHI) harness the momentum from its operational excellence to navigate the complexities revealed in its bottom line? Let’s delve into the data and uncover the full story.

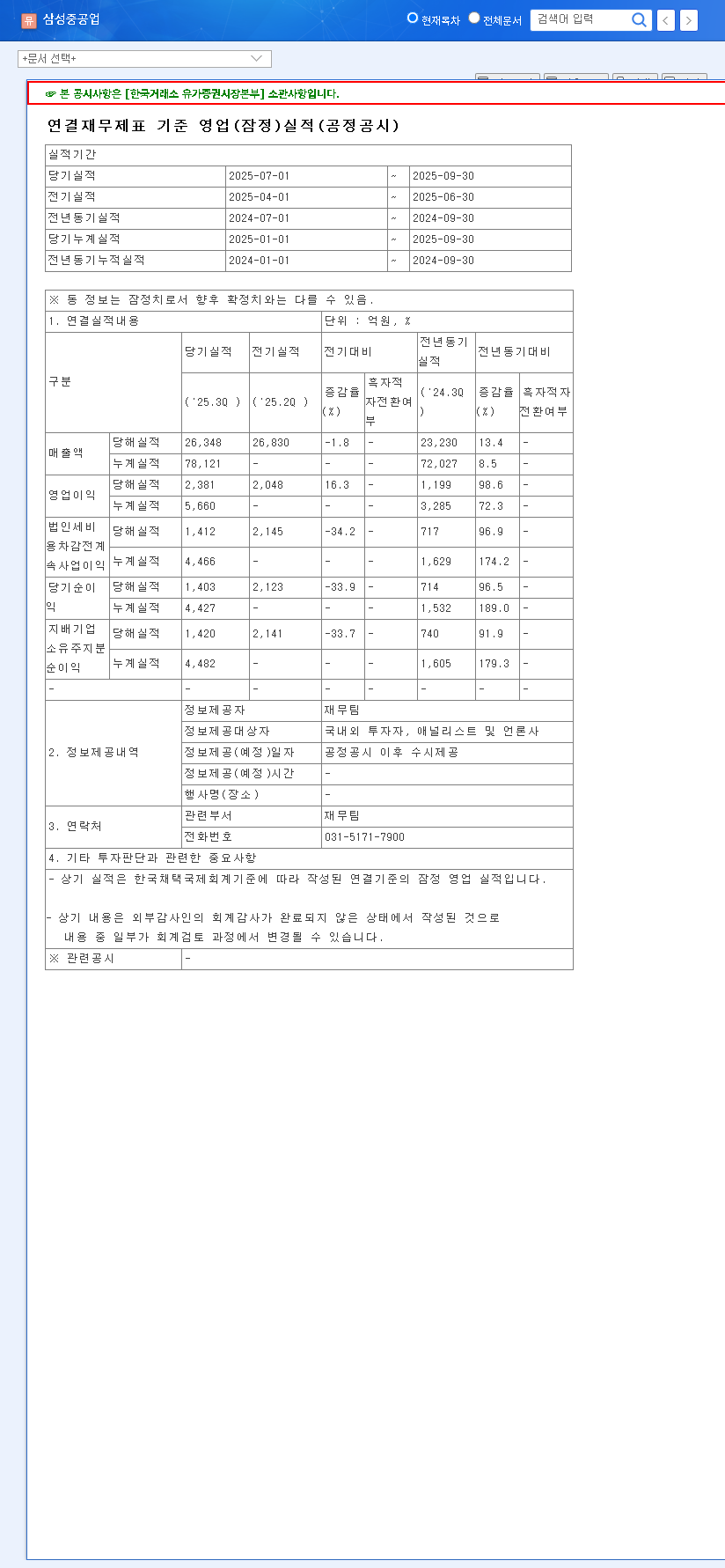

Q3 2025 Financials: The Tale of Two Profits

Samsung Heavy Industries announced its provisional consolidated financial results, revealing a fascinating divergence between operational strength and net profitability. The official figures present a clear picture of this trend. For full transparency, investors can review the Official Disclosure (DART Report).

- •Revenue: KRW 2,634.8 billion, a slight miss of 2.4% against the market estimate of KRW 2,699.0 billion.

- •Operating Profit: KRW 238.1 billion, a robust 8.2% beat over the market estimate of KRW 220.1 billion.

- •Net Income: KRW 142.0 billion, falling 17.1% short of the market estimate of KRW 171.3 billion.

The core story of the SAMSUNG HEAVY INDUSTRIES Q3 2025 Earnings is one of operational mastery. The company’s ability to control costs, improve margins, and enhance production efficiency is evident in its stellar operating profit. This is a powerful indicator of fundamental business health.

Decoding the Discrepancy: Why Did Net Income Falter?

The gap between a surging operating profit and a declining net income requires careful examination. Operating profit reflects the core shipbuilding business’s health, while net income accounts for non-operating factors. The shortfall in the latter could stem from several areas:

Potential Culprits for the Net Income Miss

- •Financial Costs: As a capital-intensive business, SHI’s debt servicing costs can fluctuate with interest rates. A rise in these costs could have eaten into the bottom line.

- •Foreign Exchange Losses: The shipbuilding industry deals heavily in US dollars. Unfavorable movements in the KRW/USD exchange rate can lead to significant non-operating losses on contracts and foreign currency holdings.

- •Tax Expenses & One-Off Charges: An increased corporate tax burden or non-recurring extraordinary losses related to specific projects or write-downs could also be contributing factors.

While the operating profit has been on a clear upward trend since Q1 2025, reaching its highest level in three quarters, the net income’s volatility highlights the external pressures impacting the company. A detailed statement from SHI during its upcoming investor call will be critical to fully understand these dynamics.

Investment Outlook: Navigating the Short and Long Term

Investors are now weighing the positive operational signals against the concerning net income figures. Here’s how the SHI stock analysis is shaping up.

Short-Term Market Reaction

In the immediate term, the market’s direction will hinge on which narrative wins out. The positive sentiment from the operating profit beat could drive the stock up, as it signals strong core fundamentals. However, the net income miss could create uncertainty and selling pressure. The key variable will be the company’s communication and its ability to reassure investors that the net income issues are manageable and non-recurring.

Mid-to-Long-Term Growth Drivers

For long-term shipbuilding industry investment, the focus shifts to the foundational pillars of growth:

- •Order Backlog: The true health of a shipbuilder is its order book. Consistent wins for high-value vessels are paramount for future revenue and profitability.

- •High-Value Vessels: SHI’s competitiveness in building LNG carriers, methanol-fueled ships, and complex offshore plants is crucial. These vessels command higher margins and are in high demand due to global decarbonization efforts, as outlined by bodies like the International Maritime Organization.

- •Technological Edge: Continued investment in eco-friendly technologies and smart ship solutions will define the industry leaders of tomorrow. Investors should monitor SHI’s R&D progress in these areas. For more details, see our analysis on future trends in the shipbuilding market.

Conclusion: A Cautiously Optimistic Outlook

The SAMSUNG HEAVY INDUSTRIES Q3 2025 Earnings report paints a picture of a company with a strong operational core facing external financial headwinds. The impressive Samsung Heavy Industries profit at the operating level demonstrates a successful focus on efficiency and high-margin projects. While the net income figure is a point of concern that requires clarification, the long-term thesis for SHI remains tied to its ability to secure high-value orders and lead in the green shipping transition. Prudent investors will watch for the company’s official explanation and focus on the forward-looking order book as the ultimate indicator of sustained growth.

Leave a Reply