Hyupjin Co., Ltd. has made a bold strategic move, announcing a ₩15.3 billion investment to significantly increase its Hyupjin Gwangmu stake. This acquisition of an additional 26.02% of its subsidiary, Gwangmu Co., Ltd., is more than a simple financial transaction; it’s a pivotal decision that signals a new chapter in Hyupjin’s corporate strategy, aiming to fortify its management control and unlock new avenues for growth. But what does this major capital outlay truly mean for the company’s future, its financial stability, and its shareholders? This comprehensive analysis will explore the nuances of the deal, its potential impacts, and the key factors investors should be watching closely.

Deconstructing the ₩15.3 Billion Deal

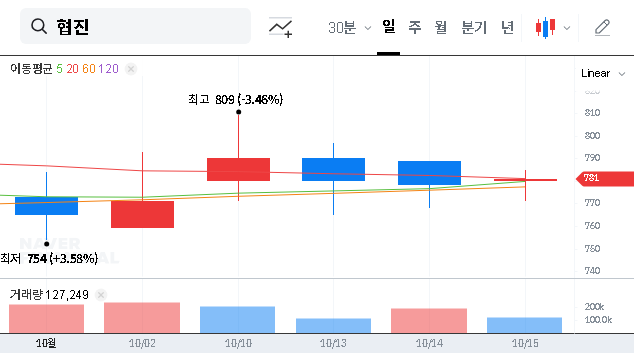

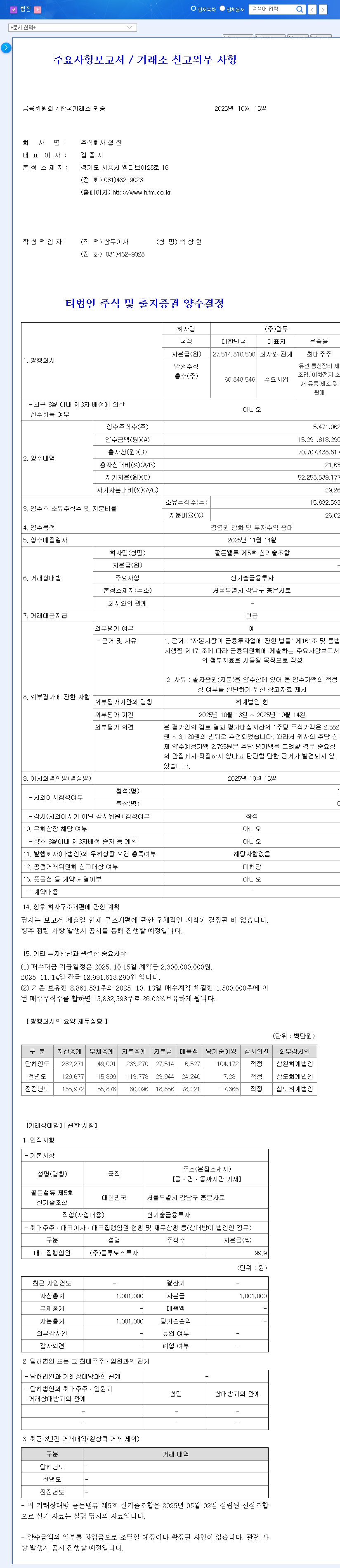

On October 15, 2024, Hyupjin Co., Ltd. formally announced its intent to acquire the additional Gwangmu shares, a transaction representing a significant 29.26% of Hyupjin’s own capital. According to the Official Disclosure (DART), the cash payment is scheduled for completion by November 14, 2025. The company has been clear about its motivations: to strengthen its management rights over Gwangmu and enhance its overall investment returns. This follows a previously successful investment where an 11.88% stake yielded substantial profits, suggesting this move is a calculated doubling-down on a proven asset.

This move is a classic example of a parent company solidifying control to steer a subsidiary’s strategy more directly, betting that deeper integration will yield greater returns than a passive investment.

Financial and Strategic Implications

The Double-Edged Sword of Cash Outflow

The most immediate impact of this Gwangmu acquisition is the significant ₩15.3 billion cash outflow. For any company, an expenditure of this magnitude can introduce short-term liquidity challenges. Investors will need to scrutinize Hyupjin’s balance sheet and cash flow statements in upcoming quarters to assess its ability to manage this financial pressure without compromising operational stability. On the other hand, this transaction converts liquid cash into a substantial investment asset. Gwangmu’s performance will now have a much more pronounced effect on Hyupjin’s consolidated financial statements, making Gwangmu’s profitability a critical factor in Hyupjin’s overall valuation.

Diversification into New Growth Engines

This increased Hyupjin Gwangmu stake is a clear strategic pivot. Hyupjin, having successfully transitioned its core business to food processing machinery, is now branching out. Gwangmu operates in seemingly unrelated sectors: wired communication equipment and secondary battery materials. This lack of direct overlap suggests the acquisition is a deliberate strategy for portfolio diversification. By entering the secondary battery market—a sector with explosive growth potential as detailed by market analysis from sources like BloombergNEF—Hyupjin is seeking to secure new, high-growth revenue streams and reduce its reliance on a single industry. For a deeper understanding of such corporate strategies, you can review our guide on analyzing business acquisitions.

Investor Outlook: A Guide to the Hyupjin Gwangmu Stake

While this investment could be a catalyst for long-term growth, it comes with inherent risks that demand a cautious and informed approach from investors. Here is a breakdown of the key considerations:

Positive Indicators to Watch

- •Proven Track Record: Hyupjin has a history of profitable investment in Gwangmu, increasing the likelihood of future success.

- •Growth Market Exposure: The move provides Hyupjin with a significant foothold in the high-potential secondary battery materials industry.

- •Strong Fundamentals: The investment is made from a position of strength, following Hyupjin’s successful business model transformation.

Potential Risks and Red Flags

- •Liquidity Strain: The ₩15.3 billion cash payment could strain short-term financial health and limit other operational investments.

- •Synergy Uncertainty: The lack of obvious operational synergy between food machinery and battery materials means the execution of a cohesive strategy is critical.

- •Transparency Concerns: Hyupjin’s past issues with disclosure corrections warrant careful monitoring of its corporate governance and information transparency going forward.

Frequently Asked Questions (FAQ)

Why is Hyupjin investing so much in Gwangmu?

Hyupjin’s primary goals are to strengthen its management control over Gwangmu to guide its strategy and to capitalize on Gwangmu’s potential for high investment returns, especially in its secondary battery materials business.

How will this Gwangmu acquisition affect Hyupjin’s finances?

In the short term, it creates a ₩15.3 billion cash outflow, which is a potential liquidity risk. In the long term, it increases Hyupjin’s investment assets, and Gwangmu’s profits and losses will have a greater impact on Hyupjin’s consolidated financial results.

What should investors monitor moving forward?

Key areas to watch are Hyupjin’s ability to maintain financial health post-acquisition, the business performance and profitability of Gwangmu, any concrete plans for synergy between the two companies, and improvements in Hyupjin’s disclosure transparency.

Leave a Reply