In a significant development for the semiconductor sector, leading design solution provider ASICLAND Co.,Ltd has announced a substantial new sales contract. This deal, valued at ₩15.4 billion, is with AI chip innovator Mobilint Co., Ltd., and appears to be a major validation of ASICLAND’s growth trajectory. However, this promising news is set against a backdrop of ongoing financial challenges, particularly concerning ASICLAND profitability.

While the contract signals robust revenue potential, persistent operating losses and unstable cash flow have raised valid concerns among investors. The crucial question is: Can this single large-scale project fundamentally reshape ASICLAND’s financial health and solve its long-standing profitability puzzle? This analysis will delve into the company’s fundamentals, the implications of the Mobilint contract, and provide a strategic outlook for investors.

This in-depth analysis unpacks the paradox of ASICLAND’s revenue growth versus its profitability struggles, offering a clear perspective on whether this new contract is a true turning point for the company.

The ₩15.4 Billion ASICLAND Contract: A Detailed Breakdown

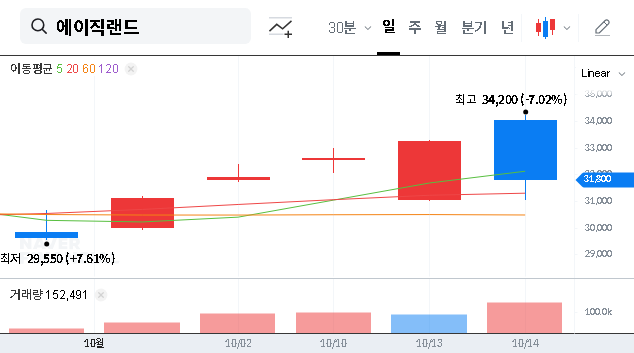

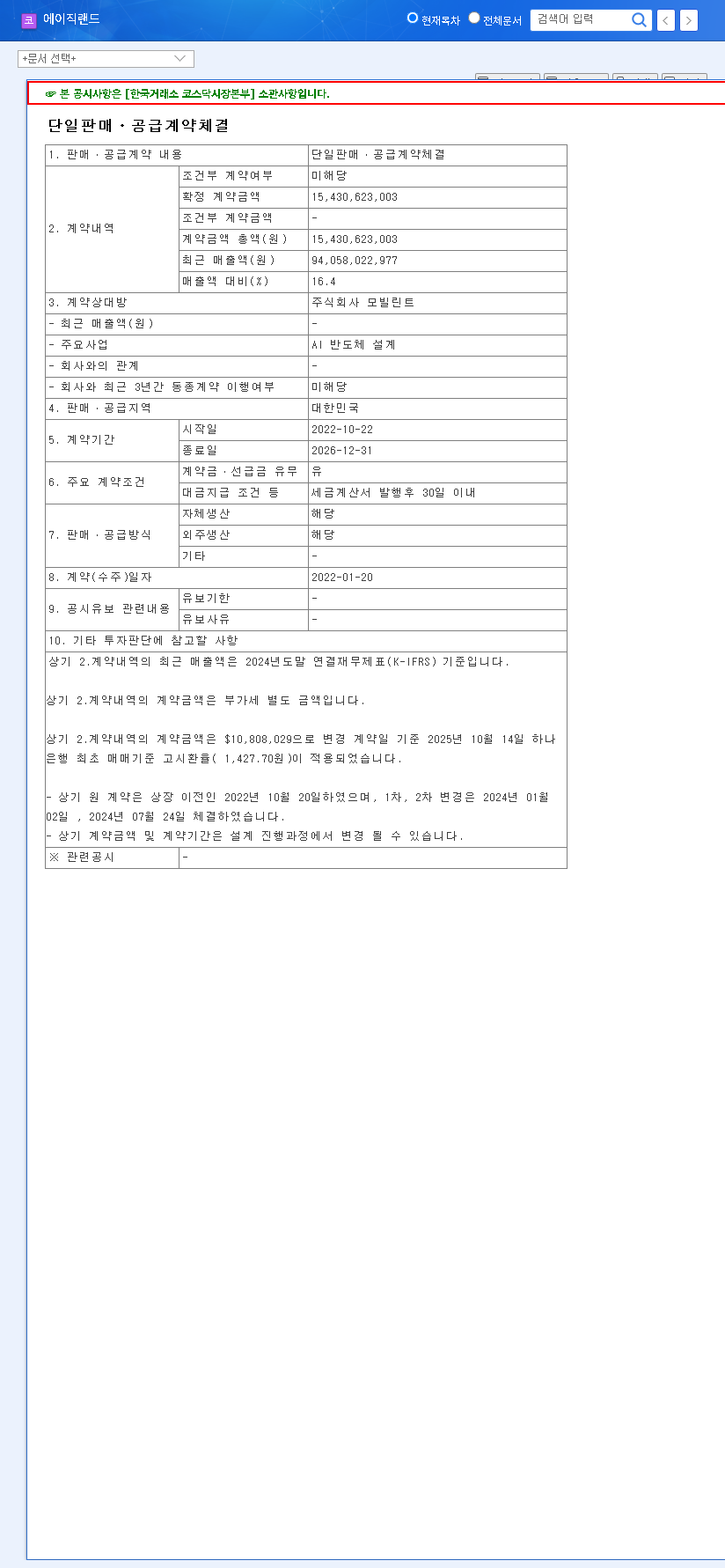

On October 14, 2025, ASICLAND formally announced a single sales and supply agreement with Mobilint Co., Ltd., valued at a significant ₩15.4 billion. According to the Official Disclosure on the DART system, this contract’s value is equivalent to 16.4% of the company’s entire 2023 annual revenue. The contract period, which extends to December 31, 2026, promises a long-term, stable revenue stream that will be crucial for the company’s performance in the coming years. This partnership with Mobilint, a company specializing in advanced AI semiconductors for the automotive industry, strategically positions ASICLAND within a high-growth market vertical.

ASICLAND’s Core Business and Financial Health

The Power of Being TSMC’s Sole Korean VCA

ASICLAND holds a uniquely powerful position in the Korean market as the sole TSMC VCA (Value Chain Alliance) partner. This grants it exclusive access to the process technology of the world’s largest and most advanced semiconductor foundry. As a premier semiconductor design solution provider, ASICLAND acts as a critical bridge for fabless companies, enabling them to bring complex chip designs to life using TSMC’s manufacturing capabilities. This VCA status is a formidable competitive advantage, providing unparalleled credibility and technical access in sectors like AI, automotive, and IoT.

The Financial Paradox: Growing Revenue, Worsening Losses

Despite its strategic strengths, ASICLAND’s financial statements reveal a troubling trend. While revenue grew consistently to ₩94.0 billion in 2024, profitability has sharply declined. The company swung from an operating profit in 2023 to significant operating losses of ₩16.97 billion in 2024 and ₩13.16 billion in the first half of 2025 alone. This deteriorating ASICLAND profitability is the central challenge. Furthermore, consistently negative operating cash flow poses a risk to liquidity and funding for new projects. While the company’s debt-to-equity ratio remains stable, the erosion of equity due to net losses cannot be ignored.

Impact Analysis: What the Mobilint Contract Truly Means

Short-Term Boost vs. Lingering Concerns

In the short term, the ASICLAND contract with Mobilint will undoubtedly bolster revenue figures and enhance market credibility. However, the immediate impact on the bottom line is uncertain. The contract’s profit margin remains undisclosed, and without it, we cannot assume that this revenue will translate into meaningful profit. There’s also a risk that the costs of fulfilling this large-scale project could further strain the company’s already negative cash flow before payments are fully realized.

Long-Term Strategic Value

The long-term implications are more promising. Successfully executing this contract strengthens ASICLAND’s portfolio in the booming automotive semiconductor market, a key pillar for future growth. According to industry reports, the demand for advanced automotive chips is expected to grow exponentially. You can learn more about this trend from authoritative sources like Gartner’s latest market analysis. This project serves as a powerful case study, validating ASICLAND’s technological capabilities and potentially attracting more high-value clients. It helps build a stable foundation, mitigating the revenue volatility seen in recent quarters.

Investment Outlook and Final Recommendations

The Mobilint contract is a significant and positive catalyst for ASICLAND. It provides revenue visibility and strengthens its strategic positioning. However, investors must look beyond the headline number and focus on the fundamental issue: profitability. Revenue growth without a clear path to profit is unsustainable.

- •Cautious Short-Term Approach: The positive news may already be reflected in the stock price. It is prudent to wait for financial reports that demonstrate a tangible improvement in profit margins and cash flow resulting from this contract.

- •Conservative Long-Term Stance: The company’s core strengths, especially its TSMC VCA status, are highly attractive. For more insights, consider reading about the semiconductor value chain. However, a conservative investment stance is recommended until the company demonstrates a consistent trend of profitability and positive cash flow.

In conclusion, this contract is a vital opportunity, but the ultimate success of ASICLAND hinges on its ability to translate top-line growth into bottom-line results. Diligent monitoring of the company’s cost management strategies and profitability metrics is essential for any potential investor.

Leave a Reply