The recent YMT CO., LTD. (251370) stake sale by SP Advanced Materials has sent ripples through the investment community, raising critical questions about the company’s future and its impact on the YMT share price. This substantial shift in ownership demands more than a surface-level glance; it requires a thorough investigation into the company’s core health and market position. Is this a warning sign, or a fleeting market event creating a unique buying opportunity?

This comprehensive YMT investment analysis will dissect the details of the stake sale, evaluate the company’s fundamental strengths and financial weaknesses, and provide a clear, actionable strategy for investors navigating this uncertainty. We’ll explore whether this is a simple portfolio adjustment or a signal of deeper issues within YMT CO., LTD.

The Disclosure Decoded: Unpacking the SP Advanced Materials Stake Sale

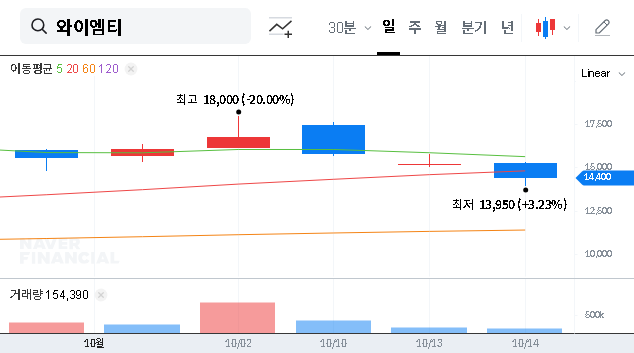

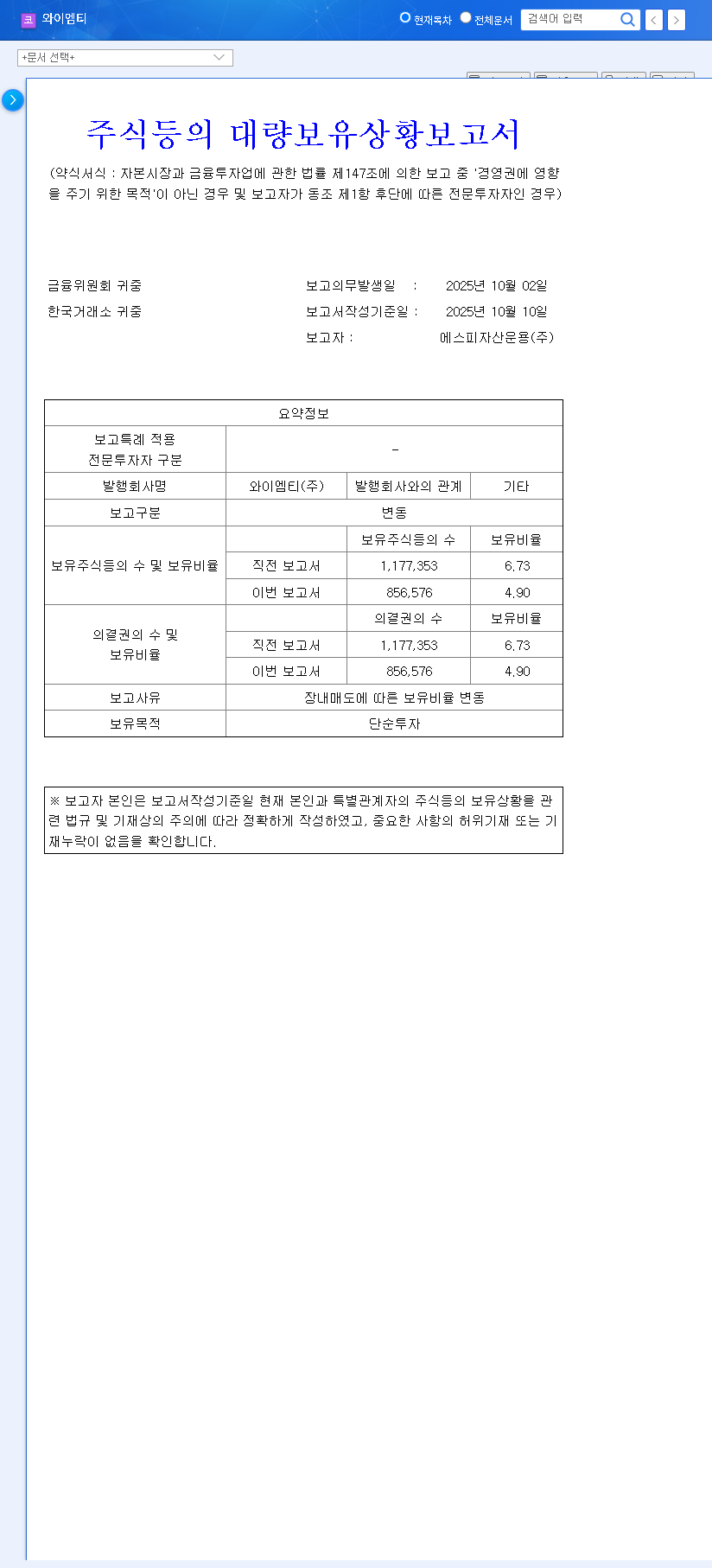

On October 14, 2025, a significant filing caught the market’s attention. According to the Official Disclosure filed with DART, SP Advanced Materials New Technology Investment Partnership reported a notable change in its holdings of YMT CO., LTD. The key details are as follows:

- •Previous Holding: 6.73%

- •Post-Sale Holding: 4.90%

- •Net Change: A sale of approximately 1.83% of total shares.

- •Stated Reason: Market sale for ‘Simple Investment’ purposes.

The crucial takeaway here is the classification as a ‘Simple Investment’. This strongly suggests the sale was motivated by profit realization or portfolio rebalancing rather than a loss of faith in YMT’s fundamental business operations. However, the market release of a significant block of shares can inevitably create short-term volatility.

Beyond the Sale: A Deep Dive into YMT’s Core Business

To truly assess the impact on the YMT share price, we must look at the engine of the company: its technology and market position. YMT CO., LTD. is a powerhouse in the PCB (Printed Circuit Board) chemical materials sector, armed with world-class proprietary technologies.

Technological Edge and Growth Catalysts

YMT’s competitive advantage is built on several pillars:

- •Advanced PCB Technologies: Its unique Soft ENIG and ENEPIG surface finishing technologies give it a strong foothold in both domestic and international markets, catering to high-end electronics.

- •New Business Ventures: The company is aggressively pushing into high-growth areas like semiconductor package substrates. Its Ultra-thin Copper Foil is particularly noteworthy, challenging the long-standing dominance of Japanese firms with superior technology and cost-effectiveness.

- •Global Footprint: With strategic expansion in China and Vietnam and a client roster including giants like Samsung Electro-Mechanics and Foxconn, YMT has a solid foundation for global growth.

While YMT’s technological prowess is clear, recent financial performance reveals underlying challenges. Understanding this financial context is crucial for any YMT investment analysis.

A Sobering Look at the Financials

Despite its business strengths, YMT’s 2024 consolidated performance raised some flags. While revenue grew 8% to KRW 137.2 billion, profitability was a concern. The company posted a razor-thin operating profit margin of just 3% and slipped into a net loss of KRW 2.33 billion, driven by higher financial costs. Furthermore, the debt-to-equity ratio has increased, a common result of funding ambitious new projects but a risk factor nonetheless. Investors should learn how to analyze company financials to better understand these risks.

Investor Outlook: Navigating the YMT Share Price Volatility

The stake sale by SP Advanced Materials is a catalyst that forces investors to weigh short-term pressures against long-term potential. Here’s a balanced perspective:

The Bull Case (Positive/Neutral)

The sale’s classification as ‘Simple Investment’ is the strongest argument against a fundamental problem. This is likely a standard move by an investment fund to lock in profits. Any temporary dip in the YMT share price could be an attractive entry point for long-term believers in the company’s technology, particularly its Ultra-thin Copper Foil venture. For more on investment strategies, you can read expert opinions on sites like Investopedia.

The Bear Case (Negative/Cautionary)

The primary risk is short-term supply pressure. A 1.83% stake hitting the open market creates a supply-demand imbalance that can depress the stock price. This effect is magnified by the existing concerns over YMT’s weak profitability and rising debt. The combination of a large seller and questionable recent financials could scare away risk-averse investors.

Conclusion: A Strategic Action Plan for YMT Investors

The SP Advanced Materials stake sale does not change the core business of YMT CO., LTD. The investment thesis hinges on whether its future growth can outweigh its current financial fragility.

- •Short-Term Strategy: Exercise caution. Monitor the share price for stabilization after the market absorbs the sold shares. A patient, wait-and-see approach is prudent.

- •Long-Term Strategy: Focus on fundamental recovery and growth milestones. Investment decisions should be tied to tangible progress in key areas like new business revenue, improved profit margins, and a strengthened balance sheet.

Ultimately, a disciplined approach that prioritizes fundamental business improvement over reacting to shareholder movements will be the most rewarding path for investing in YMT CO., LTD.

Leave a Reply