Daolink has recently captured headlines by announcing the landmark Daolink LG Uplus contract, a deal worth ₩9.1 billion. On the surface, this agreement to supply advanced Wi-Fi routers appears to be a significant victory, promising a much-needed revenue boost and reinforcing the company’s market position. However, a closer look at Daolink’s financial health reveals a precarious situation marked by soaring debt and capital impairment. This creates a critical dilemma for investors: is this contract a genuine turning point or merely a temporary distraction from deeper systemic issues? This comprehensive Daolink financial analysis will dissect the contract’s true impact, evaluate the underlying Daolink investment risk, and provide a clear action plan for anyone considering Daolink stock.

Unpacking the Daolink LG Uplus Contract

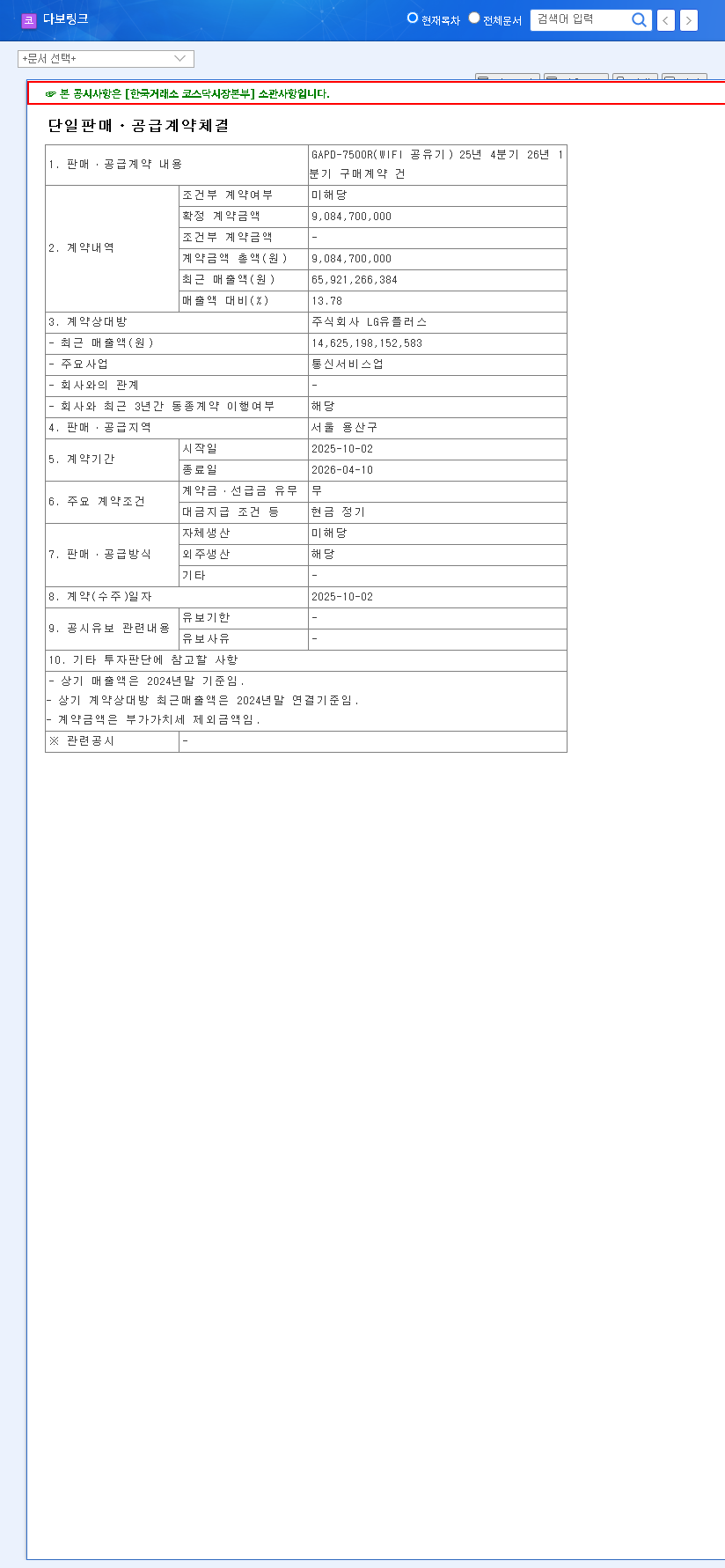

Daolink has officially secured a ₩9.1 billion single-sales and supply contract with telecom giant LG Uplus. The agreement stipulates that Daolink will provide its GAPD-7500R Wi-Fi routers between the fourth quarter of 2025 and the first quarter of 2026. This deal is substantial, representing 13.78% of the company’s recent annual sales. For investors, this news confirms Daolink’s core competency and competitiveness in the high-stakes telecommunications hardware market. The GAPD-7500R model is a key product, and securing a large order from a major carrier like LG Uplus validates its technology and market relevance.

The Alarming Contrast: A Deep Dive into Daolink’s Financial Health

Despite the positive contract news, recent financial disclosures paint a grim picture of Daolink’s stability. These documents, including the company’s Official Disclosure (DART), reveal several critical warning signs that cannot be ignored.

Key Financial Red Flags

- •Surging Debt Levels: The issuance of convertible bonds has caused total debt to balloon, placing immense pressure on the company’s balance sheet.

- •Deepened Capital Impairment: Persistent net losses and a growing accumulated deficit have severely eroded the company’s capital base, a serious concern for shareholder equity.

- •Soaring Debt-to-Equity Ratio: This critical metric, which you can learn more about from authoritative sources like Investopedia, has reached alarming levels, indicating a high degree of financial leverage and risk.

- •Rising Derivatives Liabilities: The company’s exposure to financial derivatives introduces volatility, as market fluctuations can lead to significant, unpredictable losses.

- •Expanding Non-Operating Losses: Profitability is being undermined by factors outside of its core business, such as interest expenses, further straining its financial position.

Collectively, these indicators raise serious questions about the company’s ability to continue as a going concern, making the Daolink investment risk exceptionally high at this moment.

The core issue is whether a ₩9.1 billion contract, while significant, is enough to resolve the systemic financial distress plaguing Daolink. The evidence suggests it is a step in the right direction but falls short of a comprehensive solution.

Strategic Pivots: Seeking Growth Amidst Crisis

In response to these challenges, Daolink’s management is not standing still. While working to strengthen its core Wi-Fi solutions business, the company is actively pursuing diversification to create new revenue streams. It has expanded its business objectives to include generator rentals, new and renewable energy projects, and semiconductor materials. This strategy is a double-edged sword: it offers the potential for future growth in high-demand sectors but also requires significant capital investment, further straining an already fragile balance sheet. Investors should look for more information on how these ventures align with broader trends in the tech industry to gauge their viability.

Smart Investor’s Action Plan: A ‘Hold’ Stance

Given the conflicting signals, a prudent investment approach is necessary. The Daolink LG Uplus contract is a clear positive, providing short-term revenue stability and reaffirming the company’s technical capabilities. However, the severe financial deterioration represents a critical, overriding risk.

Therefore, the current investment opinion for Daolink stock is a ‘Hold.’ Recommending a new investment is difficult until the company demonstrates a clear and credible path toward financial stabilization. A cautious, observant approach is required.

Key Monitoring Points for Investors:

- •Financial Restructuring Efforts: Watch for specific, actionable plans from management regarding debt reduction, capital enhancement, and improving cash flow. Press releases and quarterly reports are crucial sources.

- •New Business Performance: Demand tangible results from the new ventures. Monitor for actual revenue generation and profitability from the energy and semiconductor segments, not just announcements.

- •Macroeconomic Headwinds: Keep an eye on interest rates and currency exchange fluctuations. A challenging macroeconomic environment could further increase Daolink’s financial burden and operational costs.

In conclusion, while the LG Uplus contract provides a welcome glimmer of hope, Daolink’s long-term survival hinges on its ability to navigate severe financial turbulence. The uncertainty remains very high, warranting extreme caution from the investment community.

Leave a Reply