This comprehensive SHINSUNG E&G earnings analysis for Q3 2025 unpacks the recent preliminary earnings announcement that sent a shockwave through the investor community. While top-line revenue numbers appeared healthy, a drastic turn to an operating loss has raised serious questions about the company’s fundamental health and future prospects. For investors holding or considering SHINSUNG E&G stock (011930), understanding the underlying issues is more critical than ever. We will explore the performance breakdown, identify core business challenges, analyze external risks, and provide a clear investment thesis.

SHINSUNG E&G’s Q3 2025 Performance: A Deceptive Headline

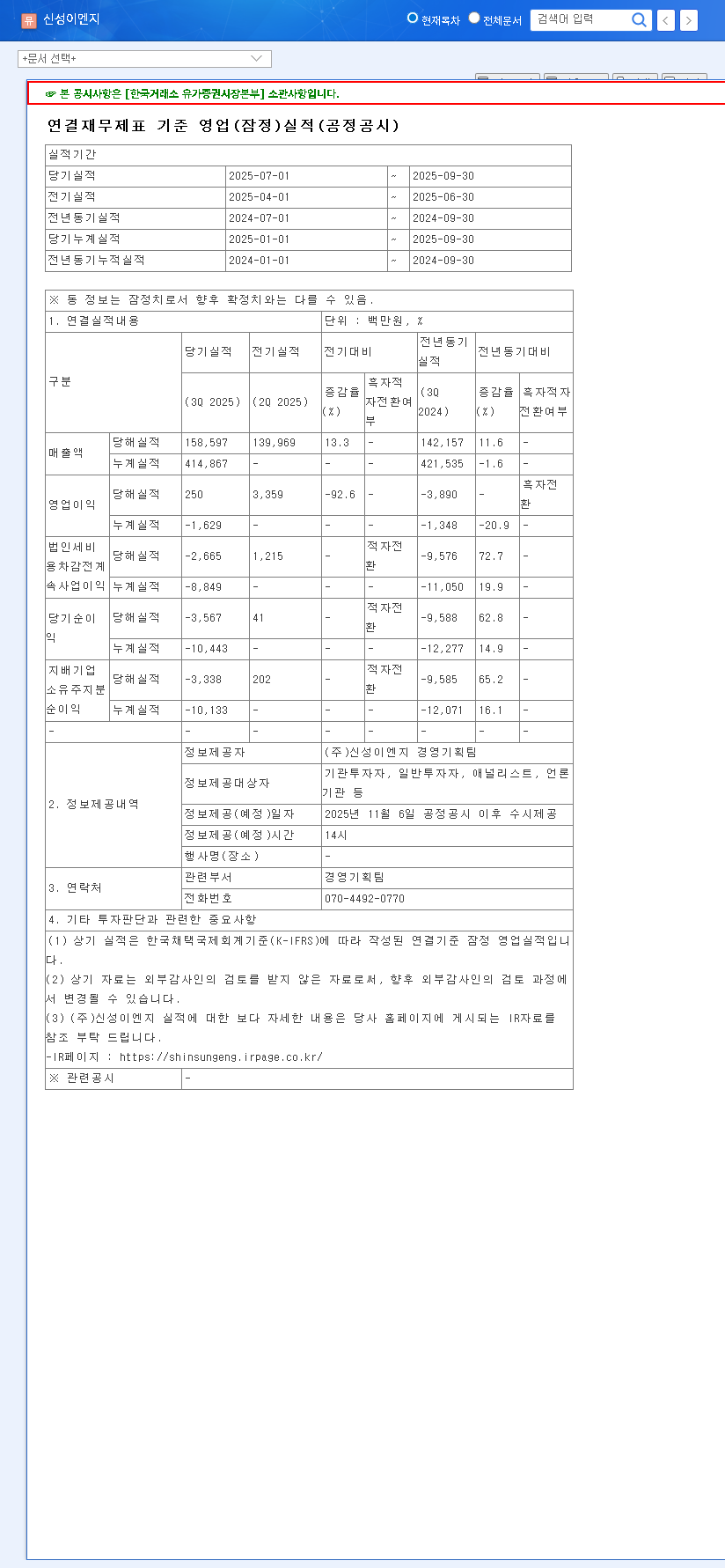

The preliminary Q3 2025 results for SHINSUNG E&G, announced on November 6, 2025, painted a confusing picture. At first glance, the revenue figure seemed promising, but the profitability metrics told a different, more troubling story. The full details can be found in the company’s Official Disclosure on DART.

- •Revenue: KRW 158.6 billion, surpassing the forecast of KRW 140.9 billion.

- •Operating Profit: KRW 0.2 billion, a significant miss on the KRW 4.6 billion forecast, representing a turn to an operating loss.

- •Net Income: A loss of KRW 3.3 billion.

This stark contrast between revenue and profit is a classic red flag. It indicates that while the company is generating sales, it is failing to convert that activity into sustainable profit, signaling deep-seated operational or structural issues.

Unpacking the Fundamental Crisis

A detailed review of the company’s semi-annual report reveals that the Q3 earnings shock is not an isolated incident but rather a symptom of a deepening fundamental crisis. Several key areas are cause for significant concern.

1. Revenue Decline and Profitability Collapse

Consolidated revenue had already decreased by 8.28% year-over-year to KRW 256.27 billion. This was driven by weakness in both the Clean Environment business (tied to volatile semiconductor and display markets) and the Renewable Energy business (plagued by a global solar module oversupply). More alarmingly, consolidated operating profit swung to a loss of KRW 1.88 billion, thanks to rising SG&A expenses and R&D costs on top of falling sales.

2. Precarious Financial Health

The company’s balance sheet is flashing warning signs. The debt-to-equity ratio remains at a high 147.39%, indicating significant leverage. Furthermore, liquidity is a major concern, as highlighted by deteriorating operational cash flow, which fell to a negative KRW 26.31 billion. For more information on evaluating company financials, investors can learn about analyzing key financial ratios.

With a current ratio of just 0.77x and a quick ratio of a mere 0.05x, the company’s ability to meet its short-term obligations without selling inventory is severely constrained. This raises serious concerns about its short-term financial stability.

Segment-Specific Headwinds and Risks

A closer look at the core business units in this SHINSUNG E&G earnings analysis reveals specific challenges that are unlikely to resolve in the short term.

- •Clean Environment Division: While there are long-term opportunities in AI and data centers, the division’s reliance on cyclical display industry investments limits near-term growth potential.

- •Renewable Energy Division: This segment is struggling to secure profitability due to intense global competition, an oversupply in the solar market, and a sluggish domestic recovery. New investments are needed but will be difficult given the weak financial position.

- •Exchange Rate Volatility: With a high volume of foreign currency transactions, the company is highly exposed to currency fluctuations. A 10% appreciation in the USD is estimated to cause a loss of ~KRW 2.2 billion, a significant risk in the current environment.

Investment Outlook: A Strong ‘Conservative’ Stance is Advised

Considering the significant Q3 operating profit miss, deteriorating fundamentals, and challenging macroeconomic conditions discussed by sources like Bloomberg, the investment outlook for SHINSUNG E&G stock is decidedly negative. A short-term price rebound appears highly unlikely.

We strongly recommend investors ‘maintain a conservative view’. A cautious approach is necessary until management presents a clear, actionable strategy to improve profitability and strengthen the balance sheet—and shows tangible results from its implementation.

Key Risk Factors to Monitor:

- •Persistent Weakness: Continued underperformance in the Clean Environment and Renewable Energy divisions.

- •Financial Deterioration: Worsening liquidity and an increasing debt burden could trigger a financial crisis.

- •Macroeconomic Headwinds: Prolonged high interest rates and a global recession could further dampen demand and increase costs.

Investors should meticulously track future earnings reports, strategic announcements, and changes in the macroeconomic landscape before making any decisions regarding SHINSUNG E&G stock (011930).

Leave a Reply