The latest LOTTE Himart Q3 earnings report for 2025 has sent a complex but cautiously optimistic signal to the market. While the Korean electronics retailer (KRX: 071840) faced persistent revenue headwinds, a significant turnaround to operating profit has caught the attention of investors. This performance isn’t just a set of numbers; it’s a story of strategic adjustments in a fiercely competitive Korean retail sector and a saturated home appliance market.

Can LOTTE Himart build on this newfound profitability for sustainable growth, or are the underlying market challenges too great? This comprehensive LOTTE Himart analysis will dissect the Q3 results, evaluate the company’s strategic position, and identify the critical watchpoints for the future.

Breaking Down the LOTTE Himart Q3 Earnings Report

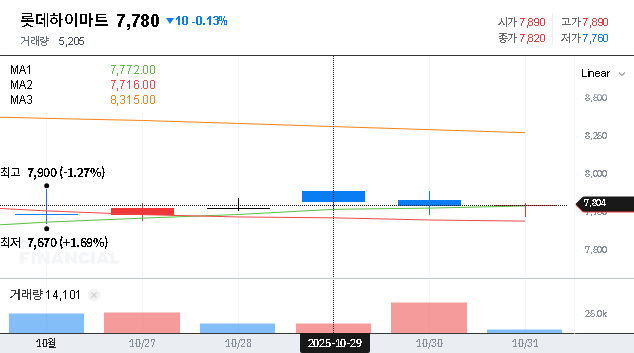

On October 31, 2025, LOTTE Himart released its preliminary Q3 operating results, which presented a mixed bag of outcomes when compared to market consensus. According to the Official Disclosure, the key figures were as follows:

- •Revenue: KRW 652.5 billion, falling 6.0% short of the KRW 695.4 billion estimate.

- •Operating Profit: KRW 19.0 billion, a narrow 4.0% miss compared to the KRW 19.7 billion estimate, but a crucial return to profitability from an H1 loss.

- •Net Income: KRW 14.2 billion, a significant outperformance, beating the KRW 11.8 billion estimate by over 20%.

The primary takeaway is the successful pivot from an operating loss in the first half of the year. This suggests that internal cost-control measures and efficiency improvements are beginning to bear fruit, even as top-line growth remains a significant challenge.

While revenue sluggishness is a concern, the impressive turnaround in operating and net income demonstrates a newfound resilience and a focus on financial discipline that could redefine the company’s trajectory.

Strategic Analysis: Navigating a Turbulent Market

LOTTE Himart’s Q3 performance is the result of a complex interplay between internal strategy and external pressures. A deeper 071840 stock analysis requires understanding these dynamics.

Internal Strengths and Financial Health

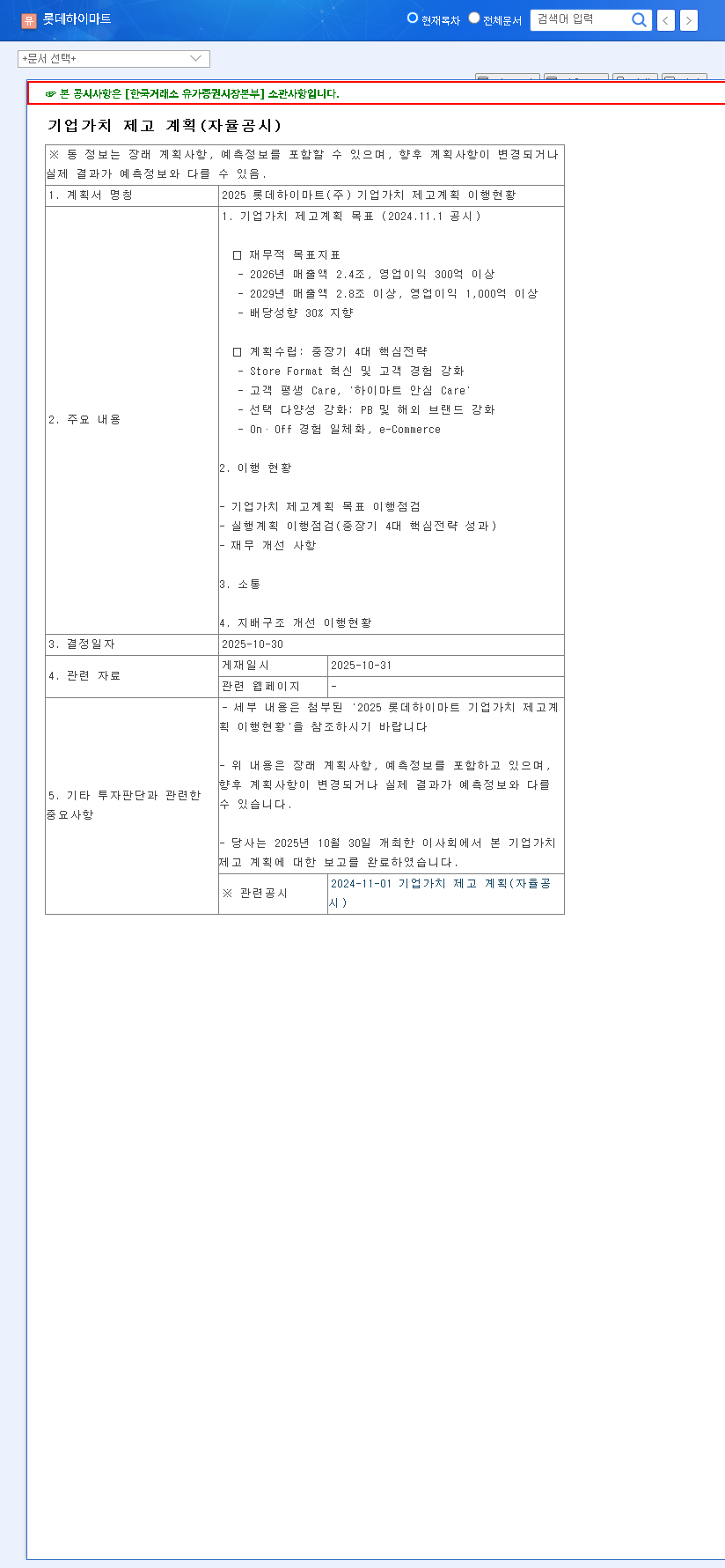

The company’s core strengths remain its extensive nationwide store network and a wide product assortment. Differentiated offerings like the ‘Himart Ansim Care Service’ and an expanding OMNI channel strategy provide a competitive edge over purely online players. Financially, the debt-to-equity ratio of 106.78% is within a manageable range. However, a notable increase in inventory assets to KRW 1.91 trillion signals a potential risk. This could indicate slowing sales or a need for more efficient inventory management, a key factor to watch as it directly impacts cash flow and profitability.

External Pressures and Market Headwinds

The home appliance market in South Korea is mature and highly susceptible to macroeconomic conditions. Persistently high interest rates and inflation have dampened consumer sentiment, directly impacting big-ticket purchases. Furthermore, competition is relentless, not just from traditional rivals but also from dominant e-commerce platforms. Macroeconomic factors, including a high Won/Dollar exchange rate (hovering around KRW 1,300), increase the cost of imported goods and components, squeezing margins. According to global market analysts, these consumer spending headwinds are expected to persist into the next year.

Future Outlook & Key Investor Watchpoints

While the Q3 return to profitability is a positive development, the path forward requires careful navigation. Investors should monitor the following key areas to gauge the sustainability of this recovery:

- •Inventory Turnover Ratio: The current ratio of 3.9% is declining. An improvement here would signal stronger sales and more efficient management, freeing up capital and reducing carrying costs.

- •New Business Contribution: Monitor the revenue and profit contribution from new ventures like franchise operations and private-label PC manufacturing. Successful integration of these businesses is crucial for long-term growth.

- •Gross Profit Margin: As revenue remains under pressure, maintaining or improving gross margins through strategic pricing, product mix, and cost control will be essential for bottom-line health.

- •Macroeconomic Indicators: Keep an eye on South Korea’s consumer sentiment index, interest rate policies, and the KRW/USD exchange rate, as these will directly impact both sales and costs.

In conclusion, the LOTTE Himart Q3 earnings mark a potential turning point. The company has demonstrated its ability to adapt and control costs in a difficult environment. However, the true test lies in reviving top-line growth and effectively managing inventory. The future trajectory of 071840 stock will depend on how successfully management can build upon this quarter’s profitability while navigating the persistent challenges in the broader market.

Leave a Reply